Sari-sari stores: Maximizing distribution opportunities

In this age of supermarkets and hypermarkets, why are sari-sari stores still relevant to categories such as snack foods? The sari-sari stores in the Philippines continue to serve as the pantry extension of about 20 households each. Hence, the outlet type remains an important retail channel contributing 36% of fast-moving consumer goods (FMCG) peso sales. As of June 2014, an average sari-sari store can sell FMCG products amounting to Php26,000 a month, about Php5,000 more than the average two years ago.

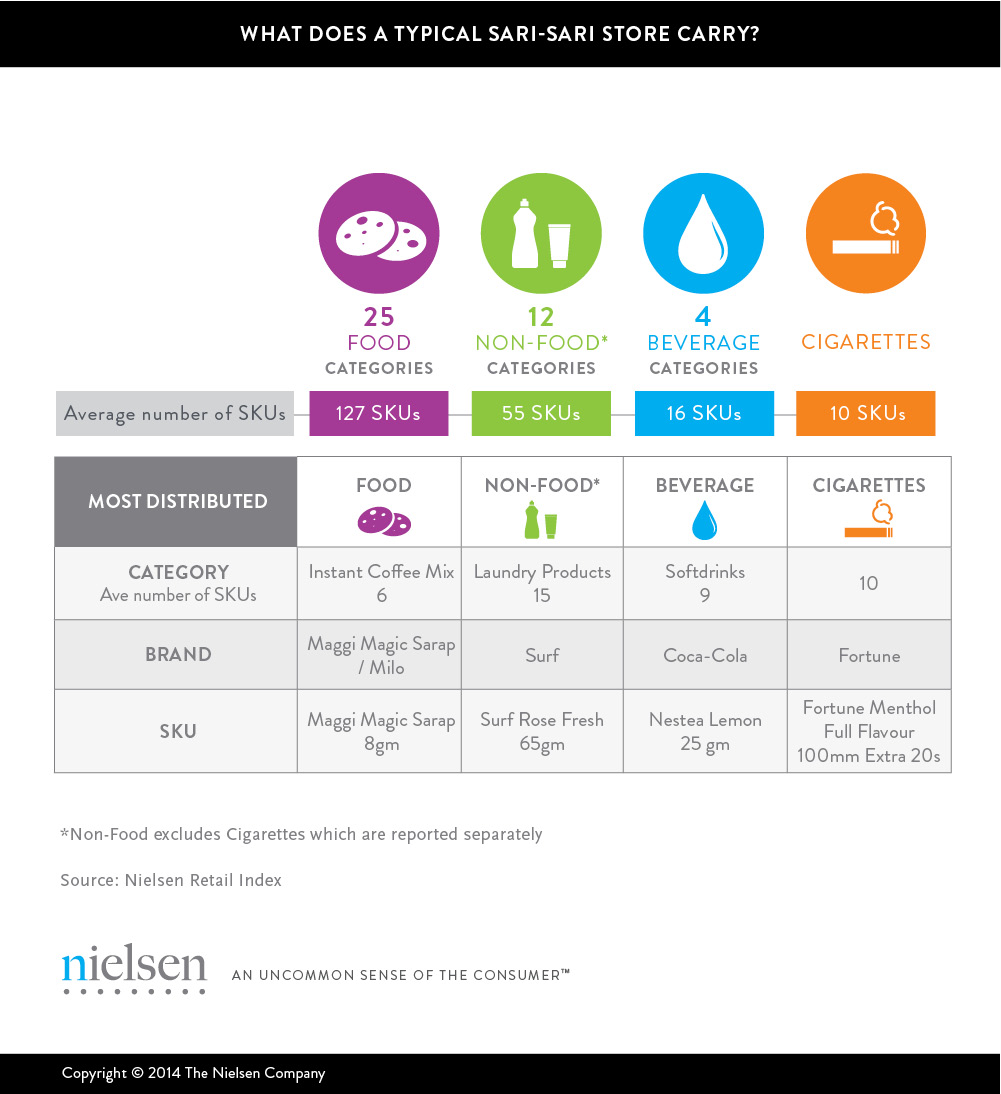

Despite having limited floor area, the typical store can carry up to 200 products, or stock-keeping units (SKUs), more than half of which are food items. Instant coffee mixes, laundry products, soft drinks, and cigarettes are the food, non-food, and beverage categories that are widely carried in sari-sari stores. Meanwhile, Maggi Magic Sarap and Milo tie for the food brand with the most presence in stores, despite coffee being the top-distributed category. For non-food and beverage, Surf and Coca-Cola lead the brands respectively.

With over a million outlets in the country, presence in the sari-sari store helps products easily reach consumers. In order to maximize distribution opportunities, companies must first understand what drives a typical sari-sari store to carry a product. Consumer demand, advertising, and trade deals are some considerations that store owners look into. Companies should employ the right mix of these to ensure their products are available.

Understanding consumer behavior

Knowing the buying behavior of consumers in the sari-sari store will also help companies plan which SKU to drive. For instance, knowing how much people spend per sari-sari store visit and how often they buy a specific category can aid manufacturers in determining a product’s price and packaging.

Setting the target

Other than comparing against the best-performing SKU for the competition, companies can also benchmark against an adjacent category to determine if there is an opportunity to carry more variants. It could also reveal more distribution opportunities should there, for instance, be more stores carrying instant coffee than coffee creamer.

Profiling the stores to tap

Understanding and evaluating a product’s distribution would also help form execution strategies. Is a particular product always sold alongside competition, or do stores prefer to carry only limited brands of a category? Can a specific SKU contend with a competing one head-on when they are sold in the same stores? Answers to these questions should shape how and where companies sell their products.

Knowing where stores source their product

But where do sari-sari stores source their products? Do they purchase primarily from the manufacturer’s distributor, a third-party wholesaler, or the neighborhood supermarket? Do they prefer these sources over others? In the Greater Manila Area (GMA), sari-sari stores generally source almost a third of their products from market stalls. Urbanity of the store’s location also plays a part in affecting a sari-sari store’s purchase preference. Based on NielsenIQ’s 2013 GMA Census,

But where do sari-sari stores source their products? Do they purchase primarily from the manufacturer’s distributor, a third-party wholesaler, or the neighborhood supermarket? Do they prefer these sources over others? In the Greater Manila Area (GMA), sari-sari stores generally source almost a third of their products from market stalls. Urbanity of the store’s location also plays a part in affecting a sari-sari store’s purchase preference. Based on NielsenIQ’s 2013 GMA Census,* sari-sari stores located in more-urban areas tend to rely more on supermarkets and company salespersons than their more-rural counterparts, who source more products from wholesalers and market stalls. Manufacturers would generate cost savings by using the most efficient route to market for their products.

sari-sari stores located in more-urban areas tend to rely more on supermarkets and company salespersons than their more-rural counterparts, who source more products from wholesalers and market stalls. Manufacturers would generate cost savings by using the most efficient route to market for their products.

Going beyond product quality and stimulating demand in the market, FMCG companies must ensure that the gap between the company and its consumers is bridged by having products that are easily accessible in trade through efficient distribution strategies applicable to their product and category.

*The GMA Census is a syndicated retail study done in 2013 which compiles a list of defined retail outlets and store characteristics within the Greater Manila Area.