COVID-19: The unexpected catalyst for tech adoption

For many consumers, new technology habits are here to stay

Challenges arising from the spread of the new coronavirus (COVID-19) are likely to accelerate the use of existing and new technologies and tools as consumers go into lockdowns, millions are forced to work from home, and digital connectivity takes even more of a hold on everyday habits.

NielsenIQ expects consumers may have greater motivations and fewer perceived barriers to more actively seek technology-enabled solutions to assist in everyday tasks like shopping. For some consumers this may be totally new behavior (such as shopping for groceries online for the first time), while for others this may mean increased online usage or the addition of new technology, tools, and software.

“There is little doubt that consumers’ uptake of technologies to stay informed and safeguard their health can instill confidence in a stressful period, and this may be the unforeseen catalyst to assert broader, longer-term adoption of technology platforms and solutions,” said Nicole Corbett, NielsenIQ Director of Intelligence.

NielsenIQ has examined recent data sets collected from consumers around the world who provided insights on their intentions as it relates to technology and reviewed it alongside developments in recent weeks tied to the COVID-19 outbreak. Through this research, NielsenIQ has identified three “catalyst moments” that may change technology adoption horizons and drive changes in shopping habits.

Curbed store visits propel shoppers online

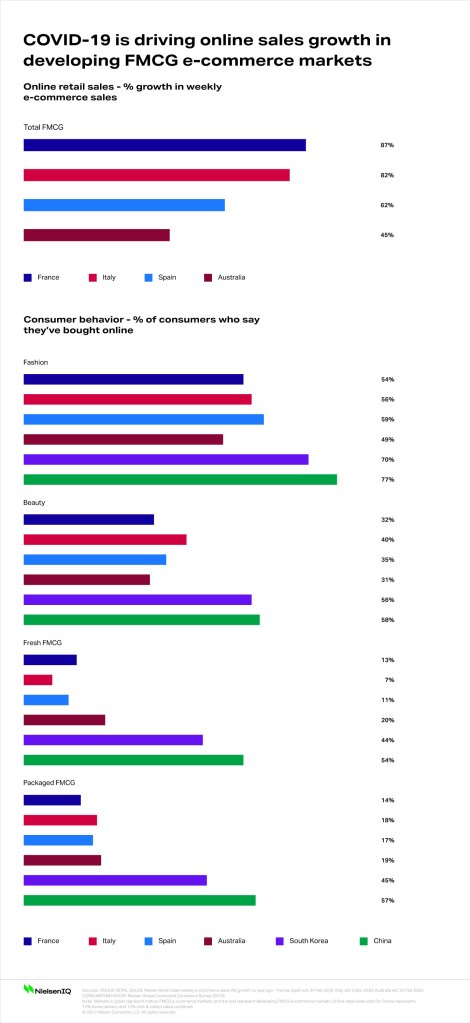

Globally, online shopping adoption has gained traction thanks to improvements in infrastructure (speed and cost), participation, transparency, and trust. The pathway for adoption is a familiar story around the world. In many markets, the fashion, travel, and entertainment categories have been the frontrunners for consumers to enter the online retail sphere, followed by the beauty and personal care categories, as consumers became more comfortable and confident shopping online. But other grocery categories, particularly packaged and fresh goods, have been slower to gain traction in some markets. Today, however, COVID-19 may be a part of driving faster change.

A NielsenIQ investigation uncovered six key consumer thresholds that tie directly to concerns around the COVID-19 outbreak. The thresholds offer early signals of spending patterns, particularly for emergency pantry items and health supplies. As many consumers around the world reach the third threshold, “pantry preparation,” they are increasingly opting for safer, non-physical stores. In examining a number of European markets that had been relatively slower to embrace online FMCG shopping before the pandemic, there are now notable spikes in e-commerce sales in recent weeks.

NielsenIQ’s retailer leader for Italy, Romolo de Camillis, has observed that from late February, as the first lockdown of some Italian areas was imposed, there has been a significant acceleration in e-commerce growth.

“In the coming weeks, however, additional growth will only be achieved if online retailers are able to meet the exponential growth in consumer demand,” De Camillis clarified. “In the future, e-commerce in Italy is likely to be a consolidated reality, with e-tailers providing a more structured and established platform, and consumers keener to buy FMCG baskets online.“

France, Spain, and Australia, where penetration of online shopping for grocery goods has previously been lower, also now show sizable increases in online retail sales, a clear sign that online retail shopping is starting to yield life-changing benefits to consumers.

In leading e-commerce markets South Korea and China, online FMCG shopping has had a strong presence for a while and is already ingrained as a regular, if not preferred, shopping habit for a large proportion of consumers. As the recent outbreak spread, older and less-adventurous consumers began also venturing online, welcoming the security and convenience that technology can provide amidst restrictions of movement and heightened caution. According to Alibaba, the number of grocery orders placed by users born in the 1960s was four times higher than normal during Spring Festival. Miss Fresh, another online retailer in China, claims its number of users age 40 and older have risen by 237% during the COVID-19 period.

For markets with both developed and developing e-commerce, the scenarios created by the spread of COVID-19 are important indicators of what retailers and manufacturers could expect as more trips to the store are curtailed around the world. In these environments, retailers will need to quickly address the main barriers or hesitations that nonusers had expressed in the past—be that freshness guarantees or free delivery. This will be key to keeping consumers online once stores reopen their doors. Although retailers themselves are likely to be faced with significant supply chain challenges in some markets, it will be critical for retailers to make the migration from offline to online as seamless as possible by communicating potential stock outages, advising of delayed delivery timelines, and providing additional online navigation tools and support to first-time users on their platforms.

2. Interrupted supply directs consumers to manufacturers

With retail supply chains progressively challenged due to COVID-19 precautions, many consumers may have initially been faced with empty shelves when searching for high-demand products both in-store and online. And this could compel some consumers to look for alternative online sources to find the products they need. Direct-to-consumer (DTC) businesses have evolved at a rapid pace in the last few years, predominantly driven by smaller, often local players, who have identified niche segments or consumer needs, and recognize the advantages of direct consumer reach, powered by technology.

In addition to the benefits of distinctive engagement opportunities, a significant feature of the DTC model is using online shopping subscriptions to entrench brand loyalty. Automated subscription services provide ease, convenience, customized rewards, preferential pricing and remove the hassle of remembering to top up. In times of unease, consumers may be clamoring for certainty and guaranteed supply, directly from the makers of their preferred brands. Many DTC manufacturers are also mastering their service via quick personalized responses to questions and providing empathy for consumers’ needs and concerns.

In a recent NielsenIQ survey on tech-transformed consumption, four in 10 global online consumers said they were already using online shopping subscriptions, and a further 36% said they were willing to do so in the next two years—an indicator that changes to existing consumer shopping habits are emerging. Corbett points out, “As shopping behavior stabilizes post COVID-19, many consumers are likely to continue to embrace manufacturer-direct technology solutions. This represents an ongoing opportunity for big and small manufacturers to assess not only their engagement platforms, but also their sales channels.”

3. Absent tangible touchpoints lead consumers to replicate reality

Despite the trends outlined above, consumers are not abandoning stores. In fact, many consumers love the store experience, from the ability to touch and feel the products to the security of knowing that what you see is what you get. NielsenIQ survey data shows that globally, consumers still have a strong affinity for in-store shopping, with 59% saying they agree or strongly agree with the statement “I really enjoy doing the grocery household shopping.” But as COVID-19 cases rise daily around the world, many consumers are waking up to self-imposed isolation and quarantine situations where a trip to the store is no longer possible or fraught with challenges. But artificial and virtual reality (A/VR) technology has the potential to bring the in-store experience into their homes.

Imagine the ability to remotely shop from the comfort of your own home. A virtual shelf fills with a curated selection based on your past purchase history. You pick up and inspect products, ask the virtual assistant questions about product ingredients, and check product reviews. You may not be in-store, but it feels like you are. And in some markets, this is already the reality, with smartphone apps leveraging augmented reality to show how a product will look in a consumer’s home or how a new shade of lipstick will suit the outfit she’s wearing or if that new pair of shoes really complements that handbag.

“We are seeing more and more examples of how virtual and augmented reality can be used in retail. The beauty sector is very big in Korea, and brands and retailers are leveraging this technology to enhance the user experience, enabling them to test and try out products virtually,” observed Ji Hyuk Park, NielsenIQ Commercial leader in South Korea. “In the challenging times of COVID-19, where hygiene is a big concern, consumers will be less prepared to physically try on products, and this is where augmented reality can replicate experiences without the health implications.”

So why does this matter? NielsenIQ data shows that more than half (51%) of global consumers are willing to try A/VR to assess products and services. With consumers not able to physically visit stores, they will be looking for alternative entertainment and shopping experiences. Companies that can leverage A/VR may hold the answer to immersive augmented reality experiences that will transform engagement and shopping.

Preparing for a technology-enabled future

As the implications for consumers multiply, new learnings for retailers and manufacturers become evident. China has showcased how companies that harness powerful technology to enable consumers during adversity can become integrated into all aspects of peoples’ lives:

QR codes from WeChat and Alipay, leveraging location data from the telecommunications industry, are highlighting where individuals have traveled and provide real-time exposure to health risks. Wiebo is keeping consumers continuously updated and informed of events. E-commerce options are promoting a growing reliance on their services among existing online shoppers and those who were previously hesitant. Tech health screening for food delivery drivers is providing vital consumer reassurances.

Previously perceived technology obstacles and barriers to adoption may no longer be as indicative or insurmountable, as technology becomes some of the only accessible or viable alternatives to consumers. While not all markets may be as technologically advanced in the retailing areas as China and South Korea, many retail and manufacturing businesses around the world can benefit from a more proactive e-commerce strategy, as technology-enabled solutions become even more sought after and preferred.

Progression in technology usage may start with the basic functionality offered by smartphones, such as product discovery and mobile payments. As consumers become more comfortable with these tools, further advancements such as auto-subscriptions and personalized location alerts will change the way consumers buy, and speed up the adoption trajectory of more-sophisticated tools like A/VR. And these will start to become more widespread as consumers recognize the advantages they can bring both in convenience and experience. Technology will be one of the most significant game-changers for FMCG retailers and manufacturers in the immediate and longer terms.

As this global health crisis continues to evolve, NielsenIQ will provide ongoing updates on the impact COVID-19 is having on consumer behavior. Visit our content hub for the latest global consumer insights into the coronavirus outbreak.