Premium has a new price in Western Europe FMCG: Proof, not positioning

Across Western Europe, consumers are beginning to feel slightly less pessimistic than they did a year ago. Yet the pressure of everyday spending remains front of mind, with cost of living still the dominant concern for many.

This creates a new kind of shopper: not one who simply trades down, but one who constantly evaluates whether something is worth trading up for.

The result is a market that looks contradictory on the surface. Consumers are scrutinizing every purchase more carefully, yet they continue to spend on premium. Not out of habit, and not out of aspiration alone, but because certain products still earn their place.

Premium has not disappeared. It has become selective. Premium+ now accounts for 28.2% of FMCG value in Western Europe and continues to grow (+4.1% year-on-year).

This is the new paradox: consumers are trading down and trading up at the same time.

Premium is becoming everyday

Premium is no longer confined to indulgence or occasional treats. It is increasingly embedded in everyday consumption.

The categories driving this shift tell the story clearly. Ambient food, fresh food, and personal care alone account for 61% of total premium growth. These are not special occasions, they are routine purchases.

Premium is no longer a moment. It is becoming a habit.

What was once reserved for “treating oneself” is now about upgrading the everyday: better ingredients, better performance, better outcomes, even in the most functional categories.

Proof over positioning: The new rules of premium

What has fundamentally changed is not the existence of premium, but the rules that govern it.

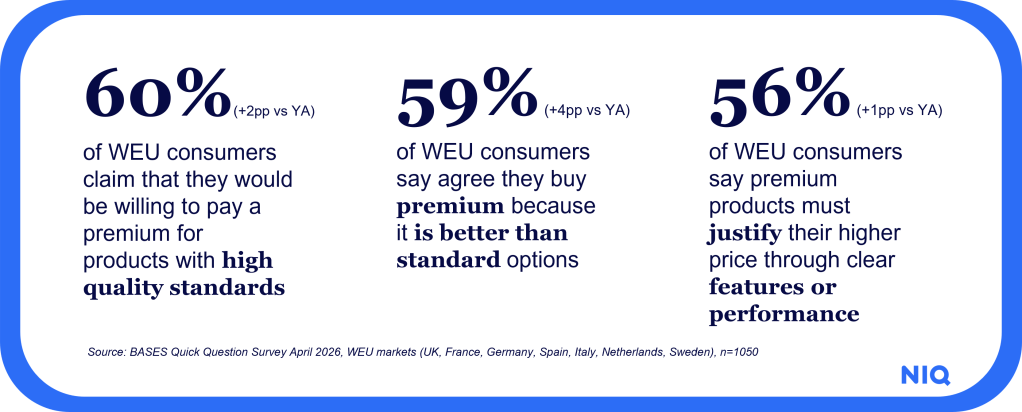

Today, 56% of consumers say premium products must justify their price through clear features or performance, while 60% are willing to pay more for high-quality products, and 59% believe premium is worth it only when it delivers better outcomes than standard alternatives.

Premium is no longer defined by what brands say. It is defined by what products do.

At the shelf, this shift becomes even more visible. 63% of consumers link premium to high-quality ingredients, while functional performance and unique features significantly outweigh simple price positioning as drivers of willingness to pay.

Premium is being judged in real time, in the context of competing alternatives. Price alone is no longer a signal of value, proof is.

Value only wins when it’s visible

This is where many brands are falling short. Differentiation still exists, but too often it isn’t obvious. And in a more selective market, anything that requires explanation risks being overlooked.

Consumers assess value in the moment, combining functional performance, emotional resonance, and contextual comparison into a single, rapid judgment.

That is why premium growth is uneven across the market. It accelerates in categories where improvements are easy to see and experience, such as small domestic appliances, and slows where differentiation is harder to communicate, even if innovation is still happening.

The implication is clear: value does not convert unless it is immediately visible.

Fragmentation and new competition

At the same time, loyalty is fragmenting.

49% of consumers say they are buying a wider variety of brands than before, reflecting a clear shift away from automatic brand loyalty. Switching is easier than ever. Discovery happens digitally, validation happens socially, and the final decision happens in the moment.

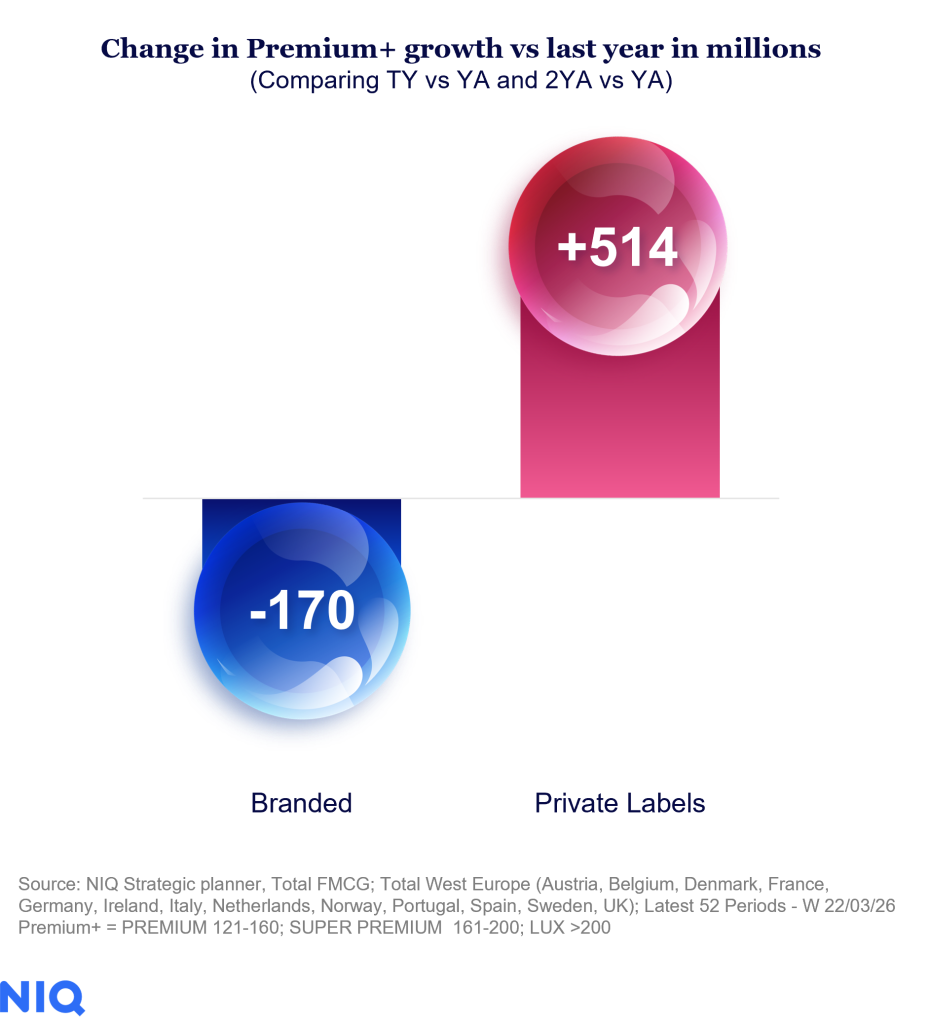

In parallel, the competitive set is expanding. Private label is no longer just an entry-level alternative, it is moving into premium space at pace. In fact, private label is contributing significantly more to recent premium growth (+514 vs. -170 for branded players).

Retailers are not just competing on price anymore. They are building credible premium propositions of their own.

In this environment, premium is not retained through legacy. It is re-earned with every purchase.

Premium is won in the moment of choice

All of these forces point to a deeper shift: premium is no longer a fixed position in a price ladder. It is fluid.

Consumers assess value holistically. Functional benefits, emotional signals, design cues, price context, and personal relevance all come together in the moment of decision.

This is not theoretical, it is behavioral. 1 in 3 consumers are actively trading up within categories, while 38% continue to buy premium even under budget pressure when the value holds.

Premium exists only when these cues align.

For brands, this requires a reset. Premium growth is no longer about stretching upward. It is about building clear, compelling reasons to trade up and stay.

That means creating accessible entry points, delivering meaningful differentiation, using design to signal value instantly, and building trust through consistent delivery.

The question is no longer whether consumers can afford premium.

It is whether brands are giving them a reason to believe in it.