Smartphone unit sales rose 6% in North America in 4Q17 – highest growth in two years

GfK global smartphone research study covers over 75 markets in eight regions

The North America smartphone market saw demand jump six percent year-on-year in 4Q17, its strongest growth in over two years. Sales value increased by four percent to US $28.5 billion. As a result, sales in 2017 rose two percent compared to 2016, totaling 201.3 million units. This recent upturn is not expected to last, though; GfK forecasts demand in North America to be flat in 2018 compared to 2017.

GfK forecasts end-demand consumer smartphone purchases – rather than manufacturer shipments – on a global basis each quarter. Market sizes are built up by point-of-sale (POS) tracking* in 75+ markets, with updates on a weekly and monthly basis. GfK’s North American data covers the United States, Canada, and Mexico.

* For the US, GfK employs proprietary market modeling and consumer research rather than POS to produce its market forecasts.

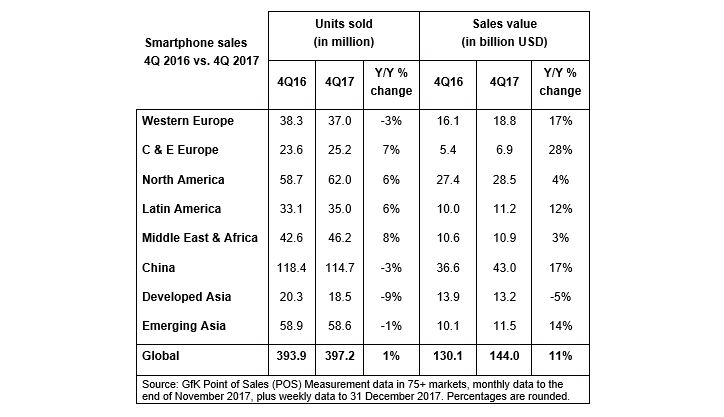

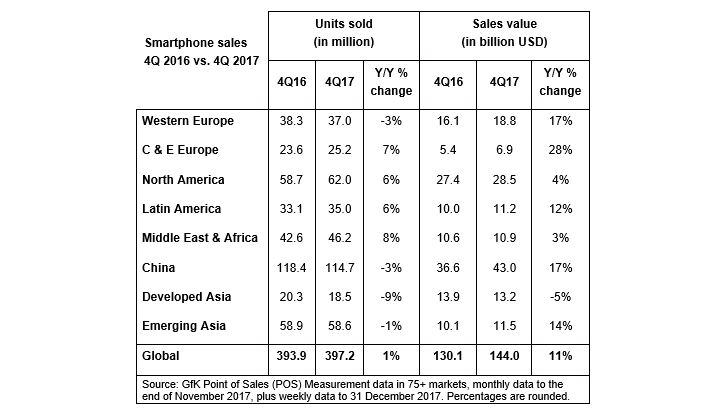

Globally, smartphone sales reached 397 million units in the fourth quarter of 2017 (4Q17), a one percent increase year-on-year. Demand was primarily driven by Middle East and Africa, which experienced eight percent growth, and Central & Eastern Europe, where demand grew seven percent. Global smartphone average sales price (ASP) increased by 10 percent year-on-year to US $363, its fastest quarterly growth rate to date.

Note: Scroll down for full data tables.

Arndt Polifke, Global Director of PoS telecom research at GfK, comments, “Smartphone year-on-year demand growth moderated for the fourth consecutive quarter, rising only one percent to 397 million units in 4Q17. However, sales value increased by 11 percent year-on-year in the quarter, which is exceptional growth for such a mature technology category. This came as the proliferation of smartphones with larger and bezel-less displays incentivized consumers to purchase more expensive devices.”

Western Europe: Strong revenue development combined with a positive demand outlook

Smartphone demand in Western Europe totaled 37.0 million units in 4Q17, down three percent year-on-year. Despite this unit decline, sales value increased by 17 percent, driven particularly by 24 percent value growth in Great Britain and 19 percent value growth in France. In 2017, smartphone sales value in Western Europe totaled USD 56 billion, up five percent compared to 2016. However, in unit terms the market declined by four percent to 125.6 million. The outlook for the region in 2018 is positive, with demand expected to rise by one percent to total 126.4 million units.

Central and Eastern Europe: Strong recovery and highest value increase among all regions

Demand continued to recover in Central and Eastern Europe, with smartphone sales totaling 25.2 million units in 4Q17, a rise of seven percent year-on-year. Further, similar to trends in Western Europe, sales value increased by a massive 28 percent year-on-year. For 2017, the region saw sales of 85.2 million smartphones, a rise of nine percent compared to 2016. And it is expected to grow in 2018, with GfK forecasting a six percent increase in demand driven by Russia and Ukraine.

Latin America: Strong recovery but outlook remains moderate

Fueled by a strong recovery in Brazil, smartphone demand in Latin America continued to grow in 4Q17, with sales rising six percent year-on-year to 35.0 million units. This caused 2017 sales to rise nine percent compared to 2016. However, GfK forecasts growth in the region to moderate to two percent in 2018 compared to 2017, dragged by a slowdown in Brazil.

Middle East and Africa: Egypt and Saudi Arabia drive strong growth in smartphone demand

In Middle East and Africa, smartphone sales totaled 46.2 million units in 4Q17, a rise of eight percent year-on-year, with growth driven primarily by Egypt and Saudi Arabia. In Egypt, demand grew by an impressive 28 percent in the quarter, while in Saudi Arabia it rose 24 percent. In 2017, smartphone sales in the region totaled 176.5 million units, a rise of four percent compared to 2016. GfK forecasts demand to rise by five percent in 2018, as relatively low levels of smartphone penetration in this region leaves plenty of room for first-time buyers to enter the market.

China: Despite demand decline, value growth was stellar

Quarterly smartphone demand in China was sluggish, with 4Q17 sales declining three percent year-on-year to 114.7 million units. This was the first year-on-year decline for the country in two and half years. However, sales value increased by 17 percent year-on-year, as consumers continue to shift towards mid-range and high-end devices. In 2017, demand rose one percent to 454.4 million units, though in value terms, again growth was much higher, up 14 percent compared to 2016.

Developed Asia: Demand weighed on by South Korea

Sales in Developed Asia totaled 18.5 million units in 4Q17, a fall of nine percent year-on-year, dragged by a 21 percent decline in South Korea. Smartphone sales in the region totaled 68.5 million units in 2017, a fall of six percent compared to 2016. However, GfK forecasts a return to growth of two percent in 2018, driven primarily by improving fortunes in Japan.

Emerging Asia: Suffers its first ever year-on-year decline in 4Q17

Emerging Asia saw smartphone sales of 58.6 million units in 4Q17, down one percent year-on-year. This was dragged by a three percent decline in India, where a proliferation of low-priced 4G feature phones likely cannibalized smartphone sales. In 2017, 232.7 million smartphones were sold in the region, an increase of eight percent compared to 2016. GfK forecasts regional demand growth to improve to nine percent in 2018.

Yotaro Noguchi, product lead in GfK’s Trends and Forecasting division, concludes, “The outlook for 2018 is positive as GfK forecasts global smartphone demand to rise by three percent compared to 2017, driven by Emerging Asia and Central and Eastern Europe. With saturation in developed markets, consumer retention will be a key focus for smartphone makers, which, alongside increased commoditization, will encourage greater innovation and differentiation in order to spur sales.”

Note to editors

This release is based on final GfK Point of Sales data for October and November, and December estimates based on weekly data to 31 December 2017. Values are based on unsubsidized retail pricing. Data is available quarterly and the next data set is due in April 2018.

North America data: GfK has recalibrated its US smartphone forecast model, particularly for non-captured segments of the market (including smaller mobile phone carriers, MVNO’s and proprietary channels such as manufacturer-owned stores). GfK previously assumed that the mix of non-captured smartphone sales would decline as the major mobile phone carriers gained share. However, analyzing wholesale connections reported by all carriers, GfK concluded that the non-captured segment mix, in fact, continued to increase. Going forward, GfK will size the US market by analyzing carrier reported metrics such as net additions, churn rates and device upgrades.

Countries included in Developed/Emerging Asia in this release

Developed Asia: Australia, Hong Kong, Japan, New Zealand, Singapore, South Korea, Taiwan

Emerging Asia: Bangladesh, India, Indonesia, Cambodia, Malaysia, Myanmar, Philippines, Thailand, Vietnam