The Innovation Barometer, powered by BASES Innovation Measurement and Consumer Panel Services (CPS), quickly identifies, categorizes, and measures innovations, to bring you a quarterly update on the most active players in CPG innovation, what’s up, what’s down, who’s winning, who’s losing and more. By using NielsenIQ sales data and consumer panel data, we give you an overview of innovation activity and performance across six key super-categories: food, confectionary and snacks, beverages, alcoholic beverages, home care and personal care.

July 2026 Edition

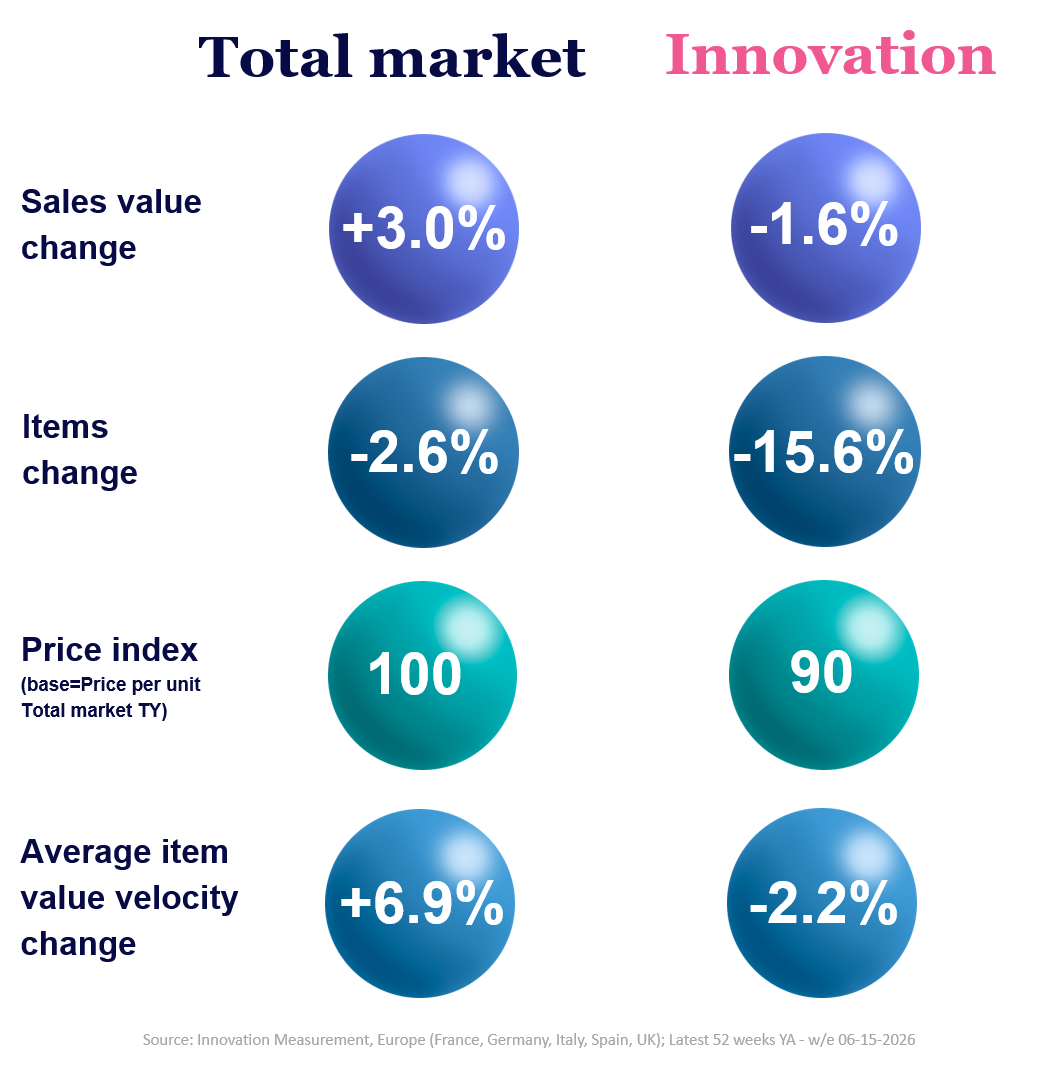

What is the current state of innovation in the CPG industry in Western Europe?

Compared to a year ago, total sales increased by 3.0%, while sales coming from innovations declined by 1.6%.

The overall number of products available in the market across all categories decreased by 2.6%, with a decline in new products of almost 16%.

This year, innovations were, on average, 10% lower priced than the average FMCG product price.

While average item value velocity increased, innovation velocity decreased.

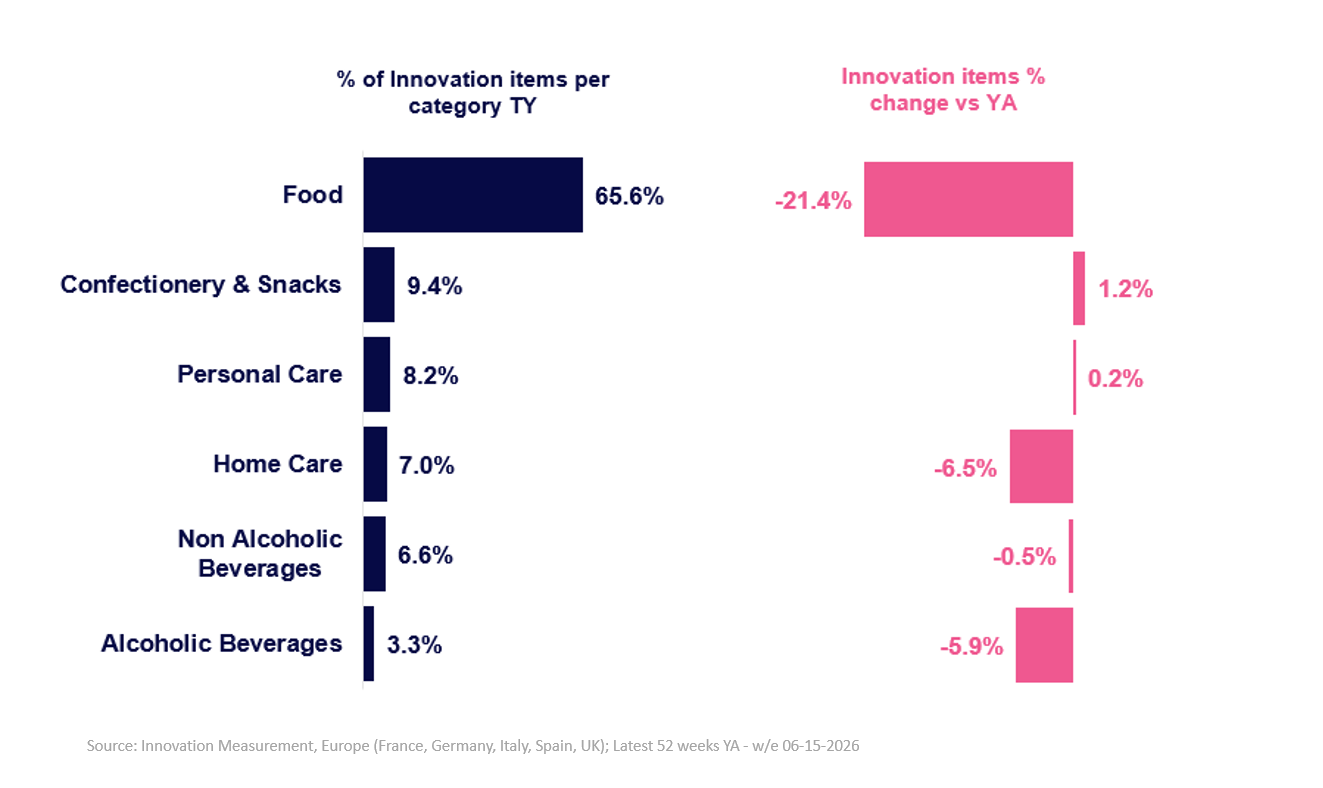

Together with holding the largest share, Food, once again experienced the steepest decline in the number of innovation items

183k

innovation items were launched in last 52 weeks (-15.6% vs a year ago)

Innovation Contribution

Home Care

24.9%

+1.7 pts vs YA

Total Market

9.5%

–0.4 pts vs YA

Non–Alcoholic beverages

4.7%

-0.4 pts vs YA

Average Item Velocity

Food

11.565

-3.3% vs YA

Total Market

7.294

-2.2% vs YA

Personal Care

3.526

+7.5% vs YA

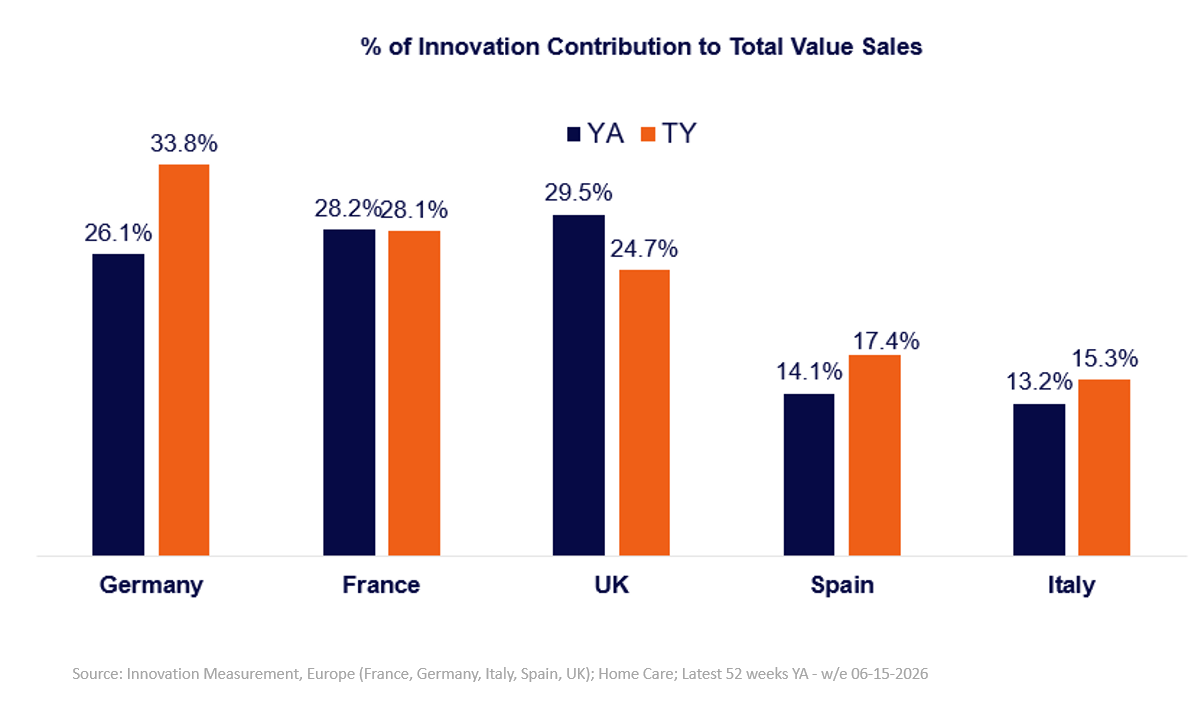

Category Spotlight

Home Care

Germany, Spain and Italy have increased innovation contribution within the Home Care category

Innovation sales holds

24.9%

of total Home Care value sales in Western Europe

5 most innovation active brand owners in Home Care

1

P&G

748

2

Henkel

272

3

Unilever

235

4

Reckitt

204

5

SC Johnson

184

Source: BASES Innovation Measurement, Europe (France, Germany, Italy, Spain) home Care: Latest 52 weeks until June 15th 2026; Total number of innovations by brand owner (product x country counts)

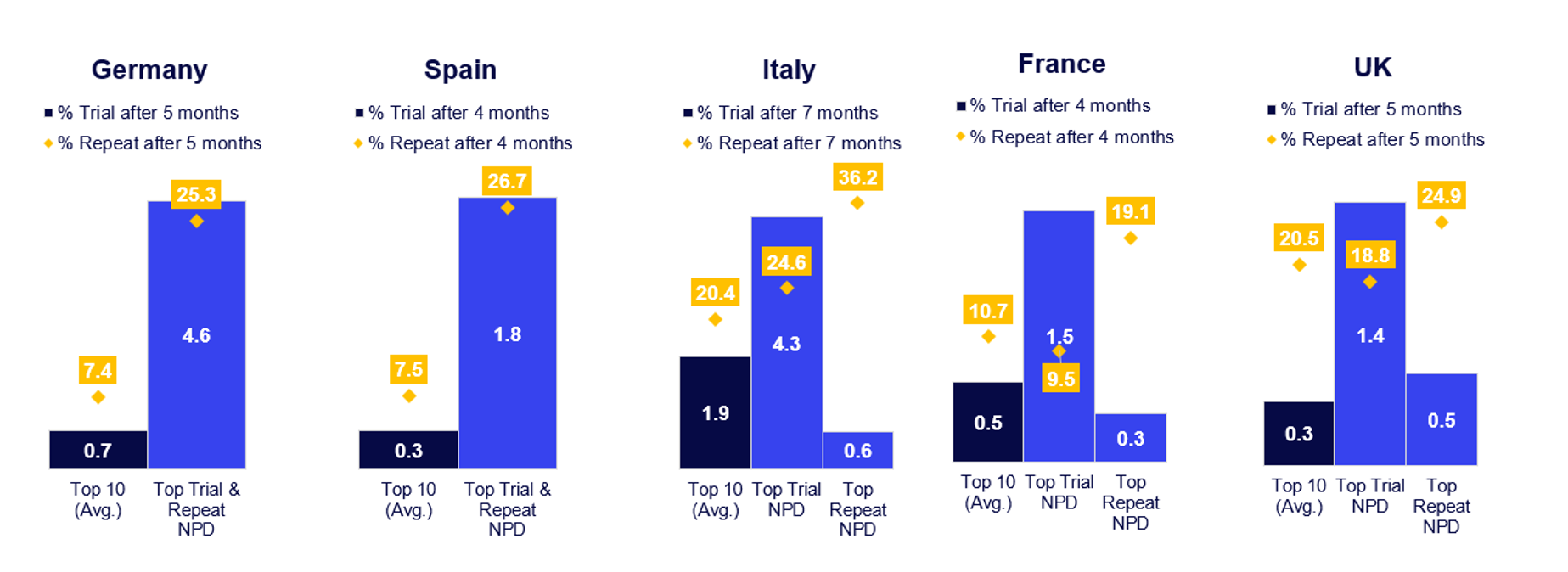

Home care launches struggle to stand out, due to their nature and long purchase cycle

Across countries, top 10 selling new products struggle to reach 1pt of penetration. Italy is the only exception.

Source: NIQ Homescan data. Top innovations cover New Brands/brand extensions and New Sub-brands, that launched in the past 52 weeks and have at least 12w of presence. Ranking is based on past year value sales within each country. Top Trial / Repeat NPD identified within Top 10 selling launches per country (based on value sales) that reached at least 0.5% penetration and scored the highest Trial and / or Repeat until May’26

Want to know which innovations made the cut?

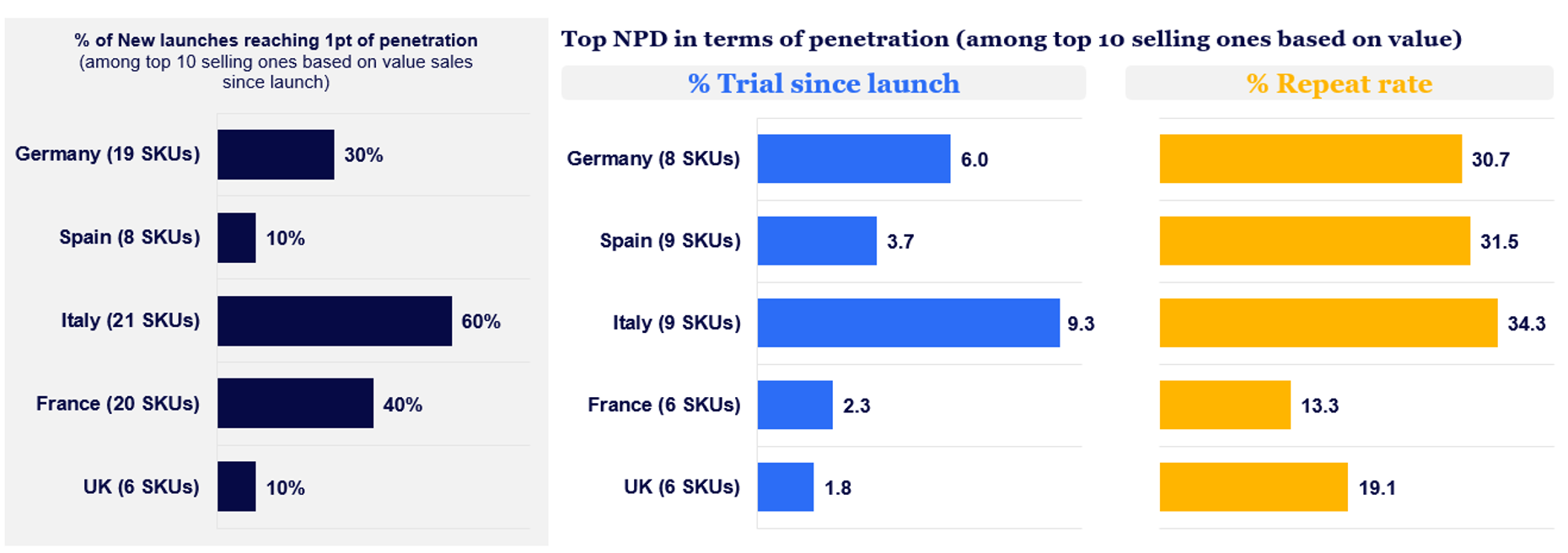

Besides more launches reaching more consumers, top performer in Italy is reaching highest trial and repeat compared to rest countries’ top performer

Source: NIQ Homescan data ending 22nd February 2026. Top innovations cover New Brands/brand extensions and New Sub-brands, that launched in the past 52 weeks. Ranking is based on past year value sales within each country

Want to get a more in-depth view of our Innovation Barometer data?