A rising SVOD tide may not raise subscription prices

With the number of subscription video on demand (SVOD) services growing, and existing ones getting frequent enhancements, media stakeholders have to wonder when “enough” will become “too much”. How many of these services will consumers subscribe to, and how much will they pay? Is there a road to profitability for market leaders who are investing millions in original content and exclusive licensing?

Movement in the marketplace

In the past year, signs of the SVOD market’s vitality have been easy to spot. There are new offerings – some smaller (Britbox) and some larger (Sling TV). A recent entrant, CBS All Access, is finally readying for its likely reason for being – the launch this fall of the streaming-only Star Trek: Discovery series.

Among the Big 3 SVOD services, we’ve seen enhancements by Hulu, which added ad-free and live-TV subscription options. Amazon expanded its originals and will offer streaming of NFL games in the coming season. Market-leader Netflix seems to have scaled back its ambitions, opting for more curation and showing a willingness to cut ties with expensive but less-successful originals (The Get Down and Sense8).

And the big recent news hanging over this entire market is Disney’s announcement that it will launch its own SVOD service and pull back its licensed content from other SVOD players – a double whammy for established players in the space.

How much are subscribers willing to pay?

We can gain some insight into the SVOD marketplace – at least for the Big 3 SVOD services – by looking at the eighth annual Over-the-Top TV report from GfK’s The Home Technology Monitor™.

First, we see that the proportion of Netflix subscribers who also subscribe to either Amazon Prime Video or to Hulu – those that are multiple subscribers – has doubled in the past three years, from 10 percent in 2014 to 21 percent in 2017. The good news: We have proof that consumers are open to having more than one paid streaming service. But, on the downside, this may squeeze the amount they are willing to pay for each.

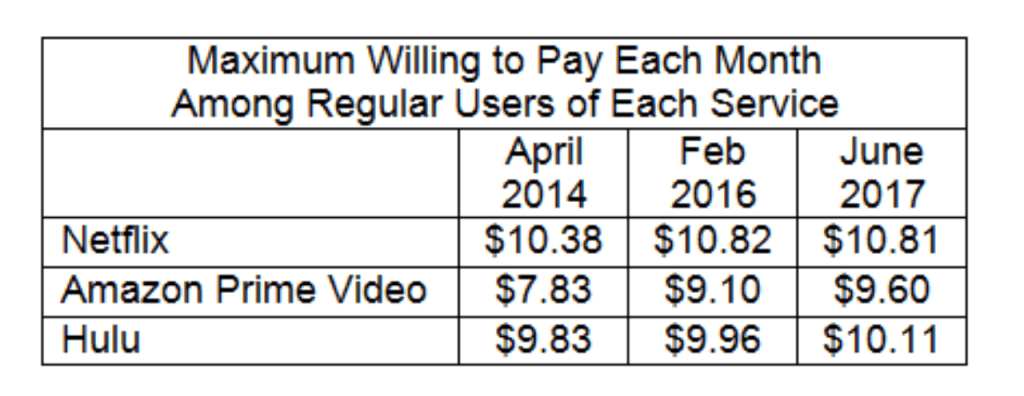

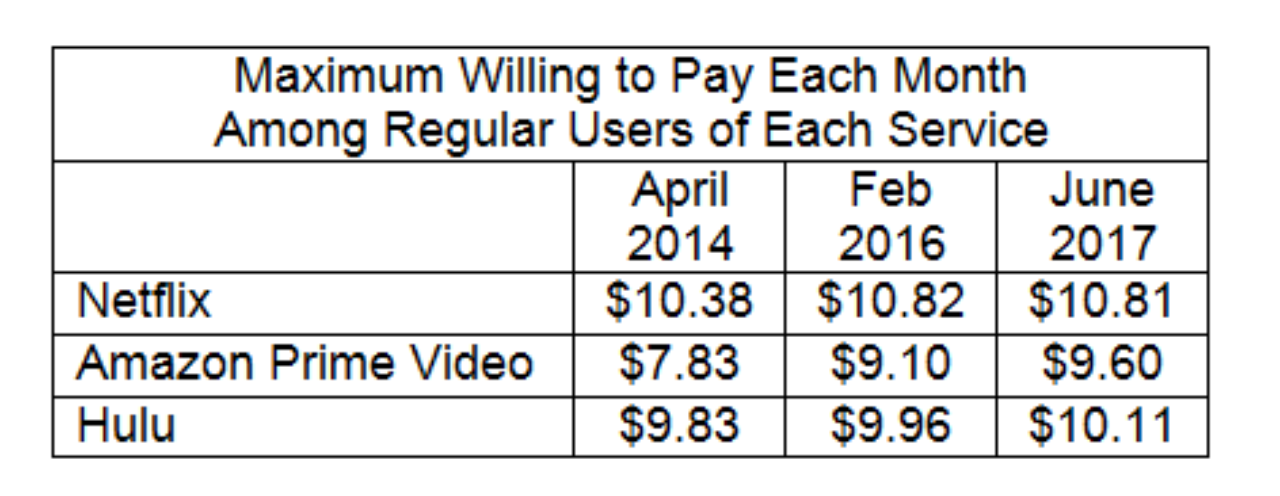

The most interesting insight comes from our tracking since 2014 of perceived value for each of the Big 3 services. Measured in 2014, 2016, and 2017, we asked regular users of each service what was the maximum they would pay per month for that service.

As we noted in 2016, and now see again in this year’s data, there is very strong indication for a “natural limit” of about $11 per month for any SVOD service. With standard service currently costing $9.99 a month for Netflix, $7.99 ($11.99 ad-free) for Hulu, and $8.25 for Amazon, we can again see there is good news (all are valued higher than their actual costs) mixed with bad (there is little room for additional subscription price increases).

In particular, Netflix appears most vulnerable. Their standard service is already priced at 92 percent of the maximum price (compared with Amazon at 86% and Hulu at 79%). Also, Netflix’s perceived value showed no change in the past 16 months, while Amazon and Hulu scored positive (albeit small) momentum. Add in the consumer budget squeeze from the increase in multiple SVOD subscriptions, and the days of being able to easily run up revenues through subscription increases may be over.

Altering the business model?

While Hulu has advertising as a second revenue stream, Amazon has both very deep pockets and a raft of additional benefits from being a Prime member (shipping, music, e-books, etc.) – perks that Netflix lacks. Netflix’s ability to offset an increasing mountain of debt[1] may be limited by its current business model; it may, at some point, need to consider advertising, program sponsorships, or other streams of revenue in order to make Wall Street happy.

Pricing aside, many other aspects of SVOD services need to be explored in the future as these services proliferate. What is the total budget for streaming and/or pay TV? How does the wide choice of services fit together? How can services avoid monthly, seasonal, or program-related churn? And, perhaps most importantly, how can consumers easily find their way to the content they want to watch across these multiple platforms? We look forward to partnering with our clients to further explore this space and help drive successful business outcomes.

Get similar insights – and many more – as soon as they get published by subscribing to The Home Technology Monitor™ in 2017. Aside from the Over-the-Top TV 2017 report, our reports this year include our annual Ownership and Trend Report, Commanding Media (voice commands), TV Everywhere, and SVOD Digital Journey.

[1] “Netflix is on the hook for $20 billion. Can it keep spending its way to success?”, Los Angeles Times, July 29 2017. http://www.latimes.com/business/hollywood/la-fi-ct-netflix-debt-spending-20170729-story.html