- Total Till sales growth grew to +4.1% in the last four weeks, up from +3.7% in the previous month, as shoppers start to plan spend for the rest of the year.

- In-store visits rose (+4.8%) as shoppers took advantage of retailers’ focus on promotions and loyalty card price cuts.

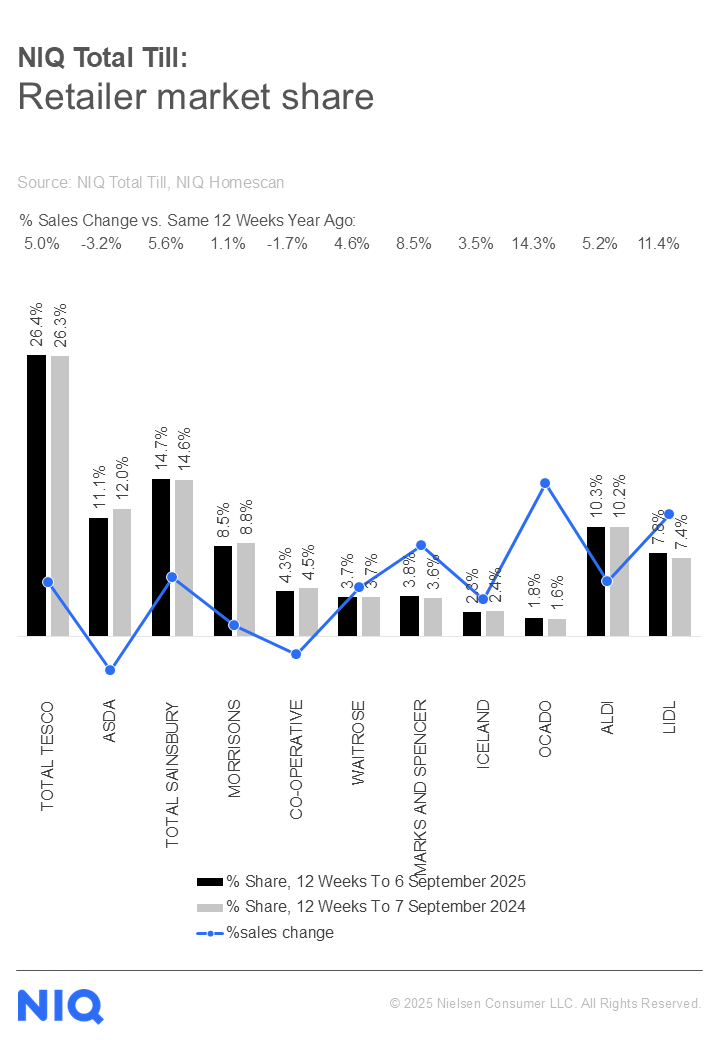

- Lidl (+11.4%) and Ocado (+14.3%) remain the fastest growing retailers with sales at Marks & Spencer also growing (+8.5%).

London, 18 September 2025: Total Till sales at UK supermarkets grew (+4.1%) in the last four weeks ending 6th September 2025. This growth up from +3.7% recorded in August signalled the end of Summer holidays as shoppers shifted focus to back to school items and preparations for Christmas celebrations. The growth was also likely supported in part by rising inflation (+4.1%)1, which increased the overall basket value. Across the Grocery Multiples unit sales fell -0.2%.2

Cautious of rising household bills, retailers were reluctant to pass on the full cost of business or supply chain pressures, as consumer demand remained transient and relatively weak. As a result, sales of items purchased under promotions increased slightly to 23.5% of sales, with shoppers leaning on loyalty card discounts to secure the best deals. Visits to stores continued to increase (+4.8%), while online shopping occasions also grew (+1.9%), reflecting the ongoing ‘little and more often’ shopping behaviour across both in-store and online grocery channels. 3

Looking at category trends, meat, fish, and poultry saw a strong increase, with total sales up (+9.2%) and units rising (+1.6%). Soft drinks also performed well, with sales up (+10.6%) and units purchased up (+4.4%), supported by the sunny weather at the end of August. In addition, health, beauty and toiletries saw sales rise (+6.2%) with the number of items also up (+1.5%).4

In terms of retailer performance, Lidl (+11.4%) and Ocado (+14.3%) continue to lead growth with Marks & Spencer also growing (+8.5%). In the last 4 weeks, one in four shoppers visited Marks & Spencer, a +11.9% growth in shoppers on last year, enticed by the new seasonal food ranges, new store openings and social media engagement. Sainsbury’s (+5.6%) and Tesco (+5.0%) also both gained market share with Waitrose (+4.6%) maintaining momentum throughout the summer.

Mike Watkins, Head of Retailer and Business Insight at NielsenIQ, said: “Following the hottest summer on record, which encouraged spending and sustained food and drink sales, the industry now faces the challenge of navigating higher inflation. One in three households currently identify the cost of living as their top concern, up from 22% in March, while nearly two-thirds of shoppers report being moderately or severely affected by rising costs, compared with 56% a few months ago. As households switch their heating back on and prepare for additional spending ahead of Christmas, most consumers anticipate that financial pressures are set to increase further.”

With 75% of households saying it’s important or very important to actively save money on their grocery bills, the build towards Christmas could be slower than previous years. 5

Watkins adds: “Looking ahead, with many shoppers unable, unwilling, or reluctant to spend freely, if food inflation reaches 5% or more by the end of the year, this could limit some of the volume increases typically seen during the Golden Quarter. So for retailers, three key challenges lie ahead: securing sales growth in the face of rising inflation to drive volume, encouraging ‘trading up’ across different shopping missions, and ensuring that media messages and forthcoming advertising campaigns resonate with increasingly price-sensitive consumers.”

Table: 12-weekly % share of grocery market spend by retailer and value sales % change

Notes

Unless otherwise stated all data is NIQ Homescan Total Till:

1 NIQ BRC SPM Food Inflation, August 2025

2 NIQ Scantrack Grocery Multiples inc Tobacco and General Merchandise

3 NIQ Homescan FMCG

4 NIQ Scantrack GB (Total Coverage)

5 NIQ Homescan Survey September 2025

About NIQ Homescan Total Till

NIQ’s continuous panel of 30,000 GB households and our widest read of retailer performance is designed to measure household purchasing through major supermarkets intended for in-home consumption and brought back into the home. It includes all food and drink, household, and personal care and an estimate of non-food spend (e.g. clothing, electrical, cards and stationery, newspapers & magazines, toys, music, general merchandise, etc.).

About NIQ

NielsenIQ (NIQ) is a leading consumer intelligence company, delivering the most complete understanding of consumer buying behavior and revealing new pathways to growth. NIQ combined with GfK in 2023, bringing together two industry leaders with unparalleled global reach. Our global reach spans over 90 countries covering approximately 85% of the world’s population and more than $ 7.2 trillion in global consumer spend. With a holistic retail read and the most comprehensive consumer insights—delivered with advanced analytics through state-of-the-art platforms—NIQ delivers the Full View™.

For more information, please visit www.niq.com