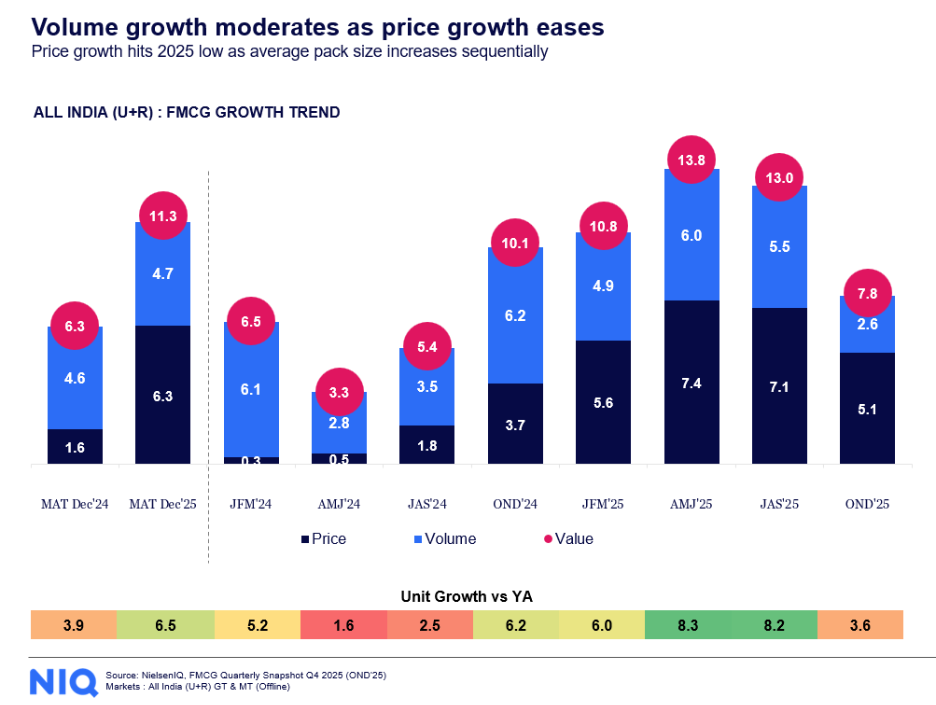

- FMCG growth moderates to 7.8% in OND 2025 amidst GST transition and high festive base

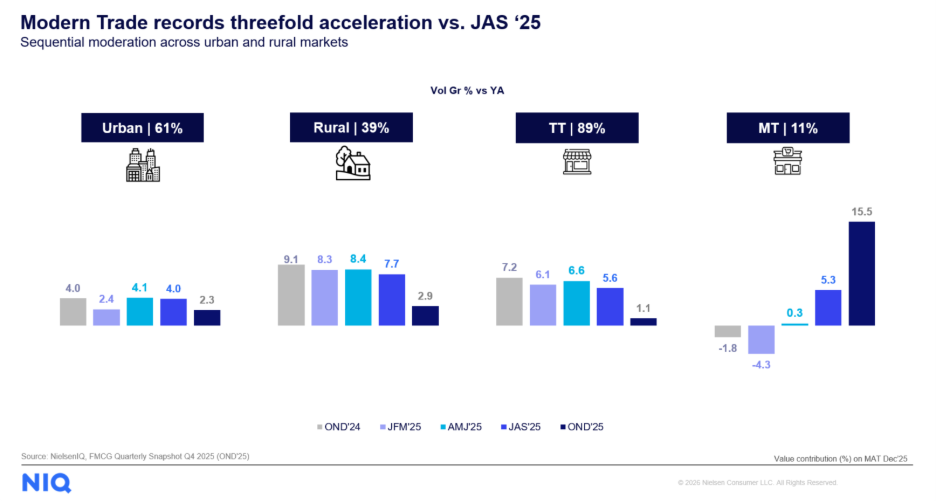

- Modern Trade records threefold acceleration versus previous quarter; E-commerce reaches 18% share in top 8 metros

- Small manufacturers continue to outpace larger players in volume growth

Mumbai — March 5, 2026 — NielsenIQ (NIQ) (NYSE: NIQ), a leader in consumer intelligence, in its Quarterly Snapshot for Q4 2025 (October–November–December, OND 2025), reports that India’s FMCG sector recorded value growth of 7.8% year-on-year, moderating compared to the July–August–September (JAS 2025) quarter (Refer to Chart 1).

“The FMCG industry witnessed heightened activity following GST 2.0 implementation, with expectations of demand stimulus across categories,” said Sharang Pant, Head of Customer Success – FMCG and Tech & Durables, NielsenIQ in India. “While initial supply and pricing adjustments led to moderated consumption in the OND quarter, organized channels responded faster to structural changes. We expect the positive impact of GST 2.0 on consumption to become more visible from the January–February–March (JFM 2026) quarter onwards.”

The moderation reflects a combination of a higher festive base in the previous year and transitional adjustments linked to GST 2.0 rate revisions. Both price and volume growth softened sequentially, particularly within Traditional Trade, which experienced temporary supply and pricing recalibrations during the initial phase of implementation.

Recent data indicates improving availability of GST-related launches and pricing alignment across the retail network, suggesting stabilization following the transition.

Source: NielsenIQ, FMCG Quarterly Snapshot Q4’25 (OND’25)

GST 2.0 Drives Structural Shift Across Channels

Nearly 60% of the FMCG portfolio underwent GST rate revisions, requiring coordinated pricing adjustments across manufacturers, distributors, and retailers. While these changes temporarily impacted Traditional Trade performance, organized channels adapted more quickly.

Modern Trade recorded a threefold acceleration in OND 2025 compared to Q3 2025, supported by faster pricing execution and stronger operational systems (Refer to Chart 2).

Chart 2: Modern Trade leads growth amidst GST transition in OND’25. Source: NielsenIQ, FMCG Quarterly Snapshot Q4’25 (OND’25)

Urban–Rural Gap Narrows as Metro Recovery Emerges

Rural markets continued to outpace urban consumption for the eighth consecutive quarter; however, the growth gap narrowed in OND 2025.

Rural regions recorded 2.9% volume growth, moderating against a higher base, while urban markets grew 2.3%, supported by recovery in Metro consumption and normalization in E-commerce demand (Refer to Chart 2).

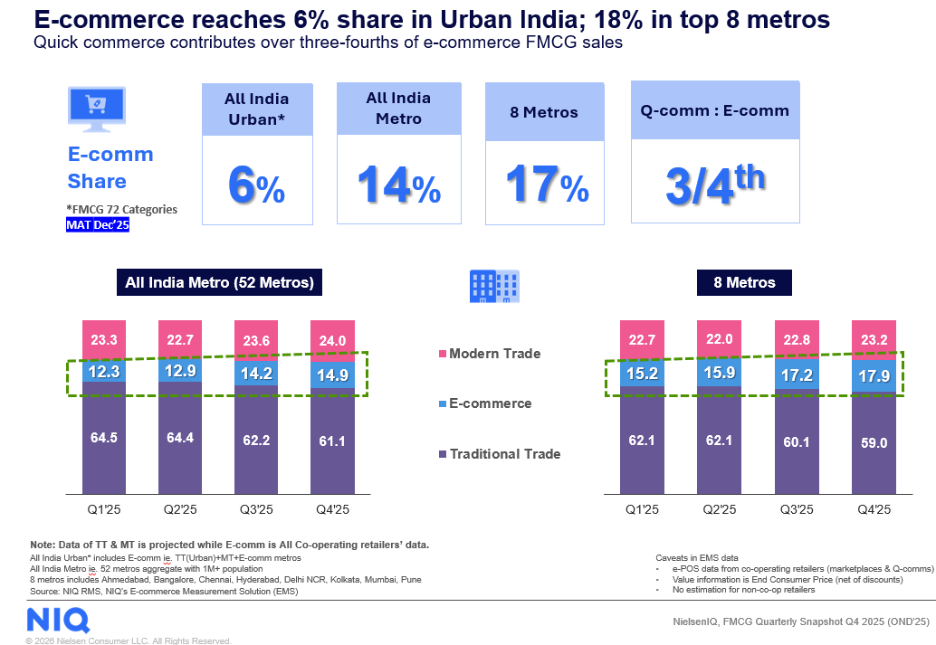

E-commerce continued its upward trajectory

E-commerce strengthened further in OND ‘25 and now accounts for:

- 6% of Urban India FMCG sales

- 14% across all metros

- 18% in the top 8 metros

Quick commerce — contributing over three-fourths of E-commerce FMCG sales — remains the key growth engine (Refer to Chart 3).

Regionally, southern metros have surpassed 21% E-commerce share, while northern and eastern metros are narrowing the gap with Modern Trade. Western markets continue to see Modern Trade leadership, though E-commerce is steadily gaining share from Traditional Trade.

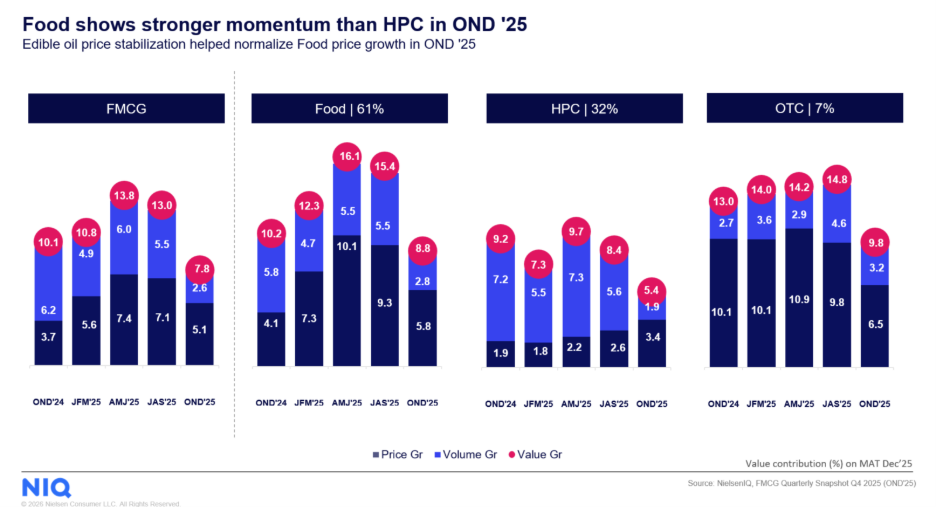

Basket Trends: Diverging Growth Across Food and Home & Personal Care

Across baskets, both Food and Home & Personal Care (HPC) saw moderation in volume growth during OND 2025.

Food consumption benefited from GST-driven price corrections and stabilization in edible oil prices, helping it outperform HPC in consumption growth. HPC recorded 1.9% volume growth, reflecting sharper moderation due to higher exposure to GST revisions.

Over-the-counter (OTC) categories posted relatively stronger consumption growth at 3.2%, outperforming both Food and HPC (Refer to Chart 4).

Small Manufacturers Continue to Gain Momentum

Small manufacturers sustained growth momentum in OND 2025, continuing to outpace the broader FMCG market in volume growth.

While overall volumes moderated across segments, large FMCG players implemented comparatively steeper price reductions to align with GST adjustments and competitive pressures. Smaller manufacturers demonstrated greater agility in pricing and portfolio adaptation, reinforcing their competitive positioning (Refer to Chart 5).

About NIQ

NielsenIQ (NIQ) is a leading consumer intelligence company, delivering the most complete understanding of consumer buying behavior and revealing new pathways to growth. Our global reach spans over 90 countries covering approximately 85% of the world’s population and more than $7.2 trillion in global consumer spend. With a holistic retail read and the most comprehensive consumer insights—delivered with advanced analytics through state-of-the-art platforms—NIQ delivers the Full View™.

For more information, please visit www.niq.com.

Forward-Looking Statements Disclaimer

This press release on India quarterly FMCG snapshot may contain forward-looking statements regarding anticipated consumer behaviors, market trends, and industry developments. These statements reflect current expectations and projections based on available data, historical patterns, and various assumptions. Words such as “expects,” “anticipates,” “projects,” “believes,” “forecasts,” and similar expressions are intended to identify such forward-looking statements.

These statements are not guarantees of future outcomes and are subject to inherent uncertainties, including changes in consumer preferences, economic conditions, technological advancements, and competitive dynamics. Actual results may differ materially from those expressed or implied in these statements.

While we strive to base our insights on reliable data and sound methodologies, we undertake no obligation to update any forward-looking statements to reflect future events or circumstances, except to the extent required by applicable law.

© 2026 Nielsen Consumer LLC. All Rights Reserved.

Media Contact:

Liza Martija – liza.martija@nielseniq.com