Promotions are everywhere, but their power is fading. Across Western Europe, FMCG markets are experiencing rising promotional pressure at the same time as unit growth slows. In other words, more products are on deal, yet fewer incremental units are being sold. The 2025 State of Price and Promotion report reveals a clear tension: shoppers are more price‑sensitive than ever, but promotions are no longer the growth lever they once were.

Western Europe: more deals, slower momentum

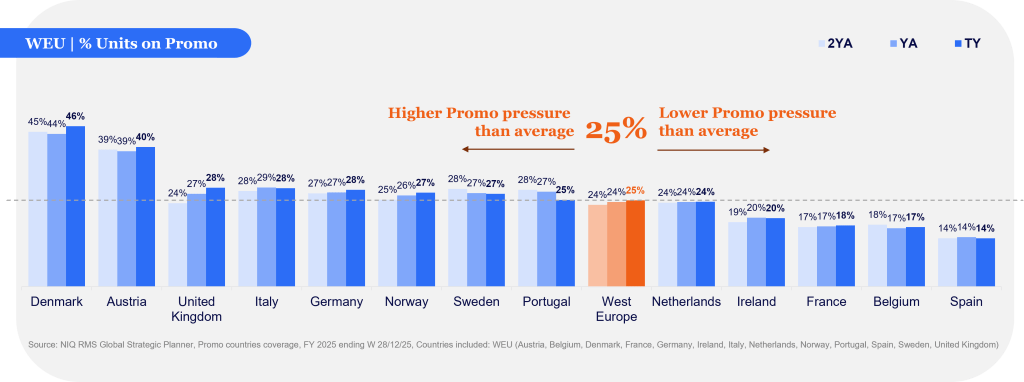

Today, one in four FMCG units in Western Europe is sold on promotion. Compared with last year, promo intensity has slightly increased, but total unit growth has slowed sharply. Inflation remains elevated, and demand has become more price‑sensitive, yet promotions are no longer delivering the incremental volume they once did.

This tension reveals a critical insight: promotions are now supporting demand rather than stimulating it. Where base (non‑promo) sales are weakening, promotions struggle to compensate. Categories and markets with declining non‑promo sales tend to decline overall, even when promotional activity increases.

Deal‑heavy markets are under the most pressure

Promotional reliance varies widely across Western Europe, and the gap between markets is widening.

Nordics, Germany and the United Kingdom stand out as highly promotion‑driven markets with more than a quarter of FMCG units are sold on deal, and promo pressure increasing year on year. Yet growth in these markets is largely price‑led, with limited unit uplift from promotions. In Germany, high promo elasticity means that small pricing missteps can trigger large volume swings, raising the stakes for precision rather than intensity.

By contrast, France, Spain, and Belgium operate with lower promotional pressure and lower inflation than the Western European average. These markets show more predictable demand dynamics. In France, for example, promo pressure remains stable, and growth is volume‑led; suggesting that better targeting, not more deals, is what matters. Spain similarly relies more on non‑promo demand, with promotions playing a supporting rather than leading role.

Italy sits between these extremes. While highly sensitive to both regular and promotional pricing, growth is primarily driven by non‑promoted food categories, with stable promo pressure overall. Here, everyday price discipline appears more important than increasing deal frequency.

Categories reveal where promotions work— and where they don’t

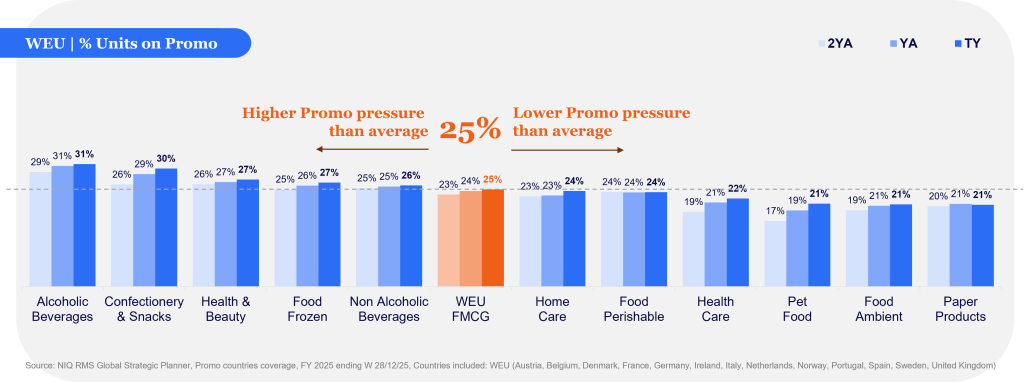

Category dynamics further reinforce the message. Promotional reliance is rising across most FMCG categories, but not evenly.

Alcoholic Beverages remain among the most promotion‑heavy categories in Western Europe. Meanwhile, Confectionery & Snacks and Pet Food show some of the steepest increases in promo pressure. Confectionery & Snacks also faces strong price inflation, making demand more volatile and more exposed to ineffective promotions.

In contrast, categories where non‑promo sales remain resilient, such as Perishable Food in several markets, are better able to sustain growth without escalating promotional intensity. The data consistently shows that promotions cannot rescue categories where base demand is already eroding.

Private Label: strong without escalating promotions

Perhaps the clearest signal comes from private label. While branded manufacturers continue to increase their reliance on promotions, private label has maintained a stable promo mix. Despite this restraint, private labels are outpacing branded products in promotional unit growth, indicating stronger promo efficiency rather than heavier discounting.

This divergence suggests that success in 2025 was less about how often brands promoted, and more about how effectively promotions were designed and deployed.

What this means for 2026

The conclusion is clear across countries and categories: more promotions are no longer a reliable path to growth.

In deal‑heavy markets, the focus will need to shift from more promotions to better ones—sharper pricing, tighter targeting, and a clearer line of sight to incrementality. In more stable markets, protecting base demand and everyday price discipline will become an even stronger source of advantage.

As consumers become more price‑aware but less promotion‑responsive, success in 2026 will depend on precision. This means protecting base demand, targeting promotions for true incrementality, and resisting the temptation to discount for volume alone. Growth will come from discipline, not pressure.