Key Takeaways

- Filipino consumers are cautious but still spending – intentionally

Economic volatility, slower GDP growth (4.4% in FY2025), and corruption-driven uncertainty are pushing households to prioritize essentials, grow savings, and demand value, convenience, and security from banks.

- Digital adoption is near-universal, but usage is shallow

99% of Filipinos shopped online in the past six months, yet only 52% actively use mobile banking apps, 29% use Internet Banking. Consumers want digital services that are fast, easy, secure, and human-supported.

- Value now means “worth it,” not just cheap

Low prices still matter, but value-for-money, convenience, and personalized experiences increasingly drive choice—especially in banking and payments.

What is shaping the new Filipino financial mindset?

Filipino consumer confidence is fragile because macro uncertainty feels personal

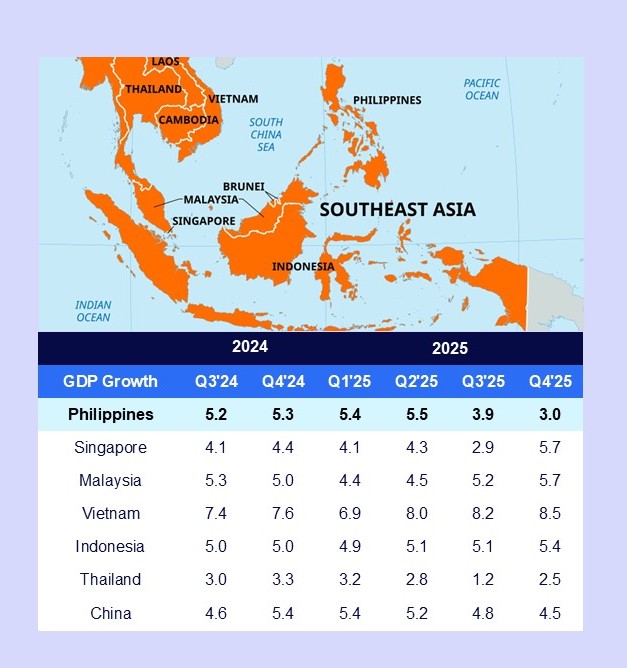

GDP growth slowed to 4.4% in FY2025, driven mainly by a sharp pullback in government capital formation and weaker government consumption.

Let’s break it down. Corruption scandals in 2025 stalled infrastructure projects. This reduced jobs, delayed income flows, and weakened business confidence.

As a result, consumer confidence indices turned negative in Q4’25, with concerns centered on corruption, inflation, and lower household income.

Why does inflation still feel painful—even when it’s slowing?

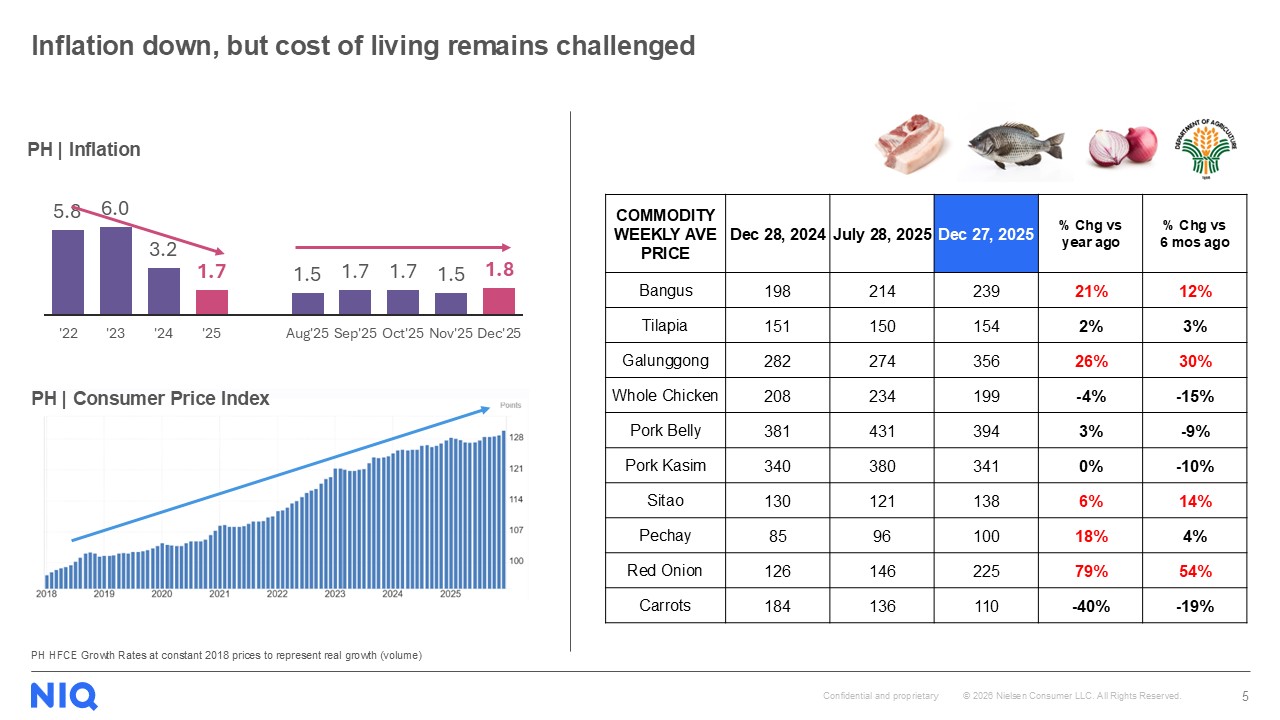

Inflation is lower, but prices are still high.

Philippine inflation eased to 1.7% in 2025, the lowest since 2022, but the Consumer Price Index continues to rise.

Here’s the short version. Inflation measures speed, not relief.

Prices for essentials like red onions (+79% YoY) remain elevated.

How are consumers adjusting their spending behavior?

Spending in 2026 is intentional—every purchase must earn its place

Consumers are adapting, not retreating. Spending caution is now built into household economics.

Common consumer behaviors you’ll recognize:

· Buying smaller packs or buying in bulk on payday

· Switching brands or channels for better value

· Waiting for promotions

· Prioritizing essentials over big-ticket items

At the same time, consumers will still spend on experiences—if the value feels justified.

What does “value” mean to Filipino consumers today?

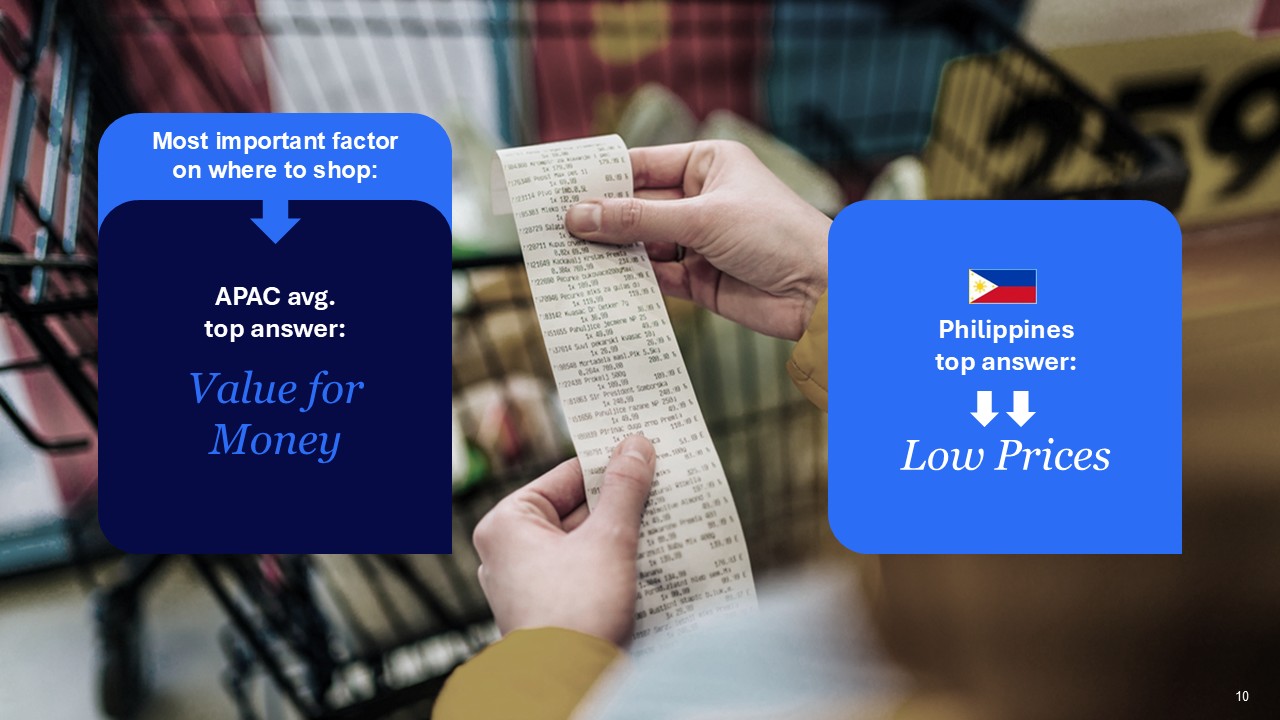

Value means usefulness, control, and peace of mind—not just low prices.

In the Philippines, “low price” remains the top shopping driver, versus “value for money” in APAC overall.

But value is evolving. Consumers now seek:

· Convenience and time savings

· Relevant offers and personalization

· Trust and transparency

This shift explains why brand switching is common and loyalty must be continually earned.

How digital is the Filipino consumer—really?

Digital access is universal; digital depth is not.

The numbers are clear:

· 99% shopped online in the past six months

· 71% use e-wallets

· Only 52% use mobile banking apps

· 29% use internet banking

Usage today is functional, not strategic. Top digital banking activities remain basic:

· Paying bills

· Transferring money

· Checking balances

What defines “good” digital banking today?

Digital convenience means fast, easy, flexible—and secure.

Consumers define good digital experiences as:

· FAST: transactions done in seconds, 24/7

· EASY: intuitive, low-effort, error-free

· FLEXIBLE: seamless online–offline integration

But one factor overrides all others.

Security is the #1 driver of bank choice.

A “good mobile app” matters—but only after trust is established.

What should banks do differently now?

Banks win by combining digital speed with human reassurance.

Winning banks:

· Deliver consistent experiences across all touchpoints

· Use data to personalize meaningfully, not aggressively

· Integrate with daily-life apps and routines

· Make security visible, not assumed

Understanding how Filipino consumers are recalibrating spending, saving, and digital expectations is now critical to staying relevant in financial services.

Learn how NIQ can help you to turn caution into growth

Request a private briefing with our experts and turn insights into action.

Contact Us