Risk and rise: State of FMCG in Eastern Europe

State of FMCG in Eastern Europe

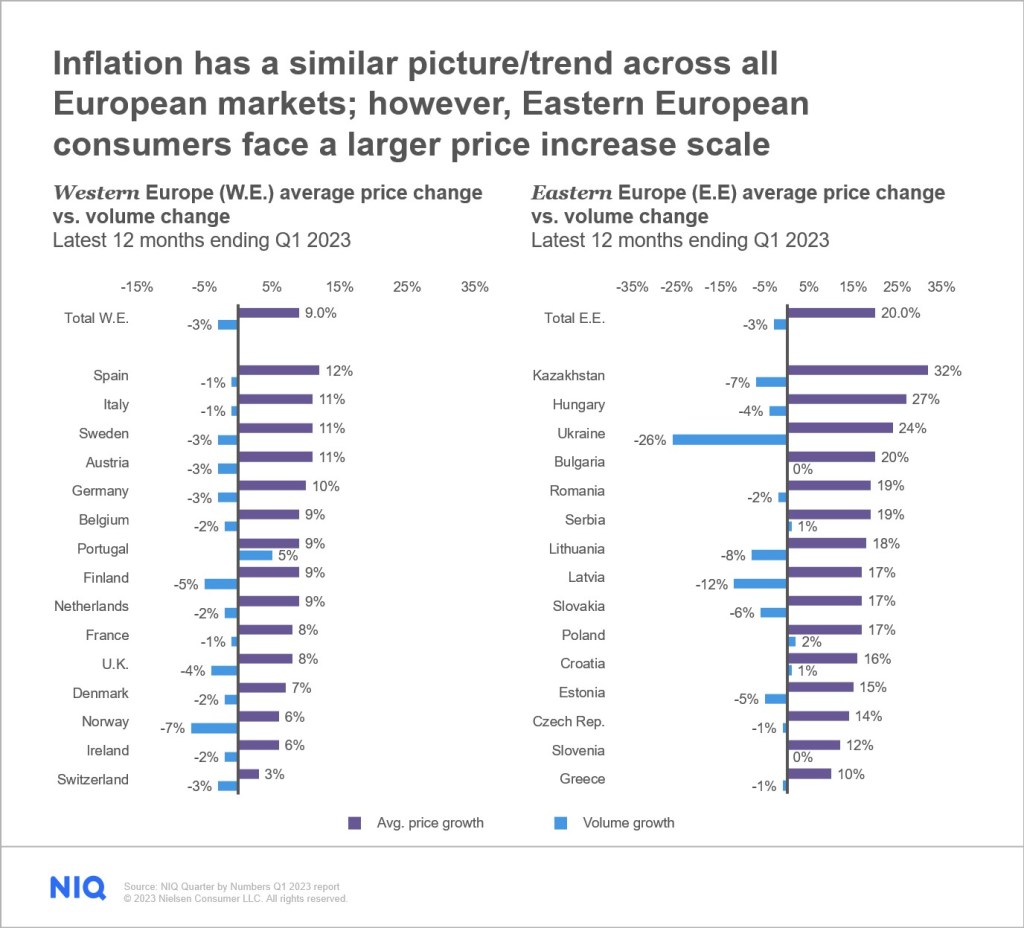

To fully capture the events of Q2 2023 in Eastern Europe (E.E.), it is necessary to approach the topic contextually. Comparing the current era to the same period last year is essentially contrasting a time when Covid had finally ceased to be the primary global threat, yielding space for a new upheaval — the escalation of the geopolitical situation in Ukraine. During this period, double-digit inflation rates had become regular, and the beginning of a decline in consumer consumption became evident.

Currently, excessive inflation is causing widespread anxiety throughout the Eastern European region. Therefore, interpreting its reduction and alleviation requires a cautious approach, using a lens to study the patterns of the previous year’s similar time. Across most Eastern European markets, consumers face more significant price hikes in Q2 versus Q1 when measured against 2021.

The same goes for reading flat volume growth versus last year since the dynamics across the warzone have had a significant influence. The distinct pattern appears in the rest of Eastern Europe, where consumption is declining. Although exceptions exist, such as Croatia and Greece, the overall consumption drop is 3.2%.

Discounters: Consumers’ top choice to fight rising costs

European consumers are becoming more cautious in their shopping selections due to the economic setbacks caused by the global energy crisis, extreme weather, and rising prices. Many people are already in safeguard mode because they are worried about the future.

With inflation being a major worry for both consumers and business leaders, modest price increases were critical in promoting FMCG sales in Eastern Europe. Consumer confidence has been greatly impacted by the cost-of-living problem, with rising food costs being the top concern for 44% of European consumers. As a result, shoppers are shifting their preferences from premium to more affordable options, favoring discount stores that offer a better value for money.

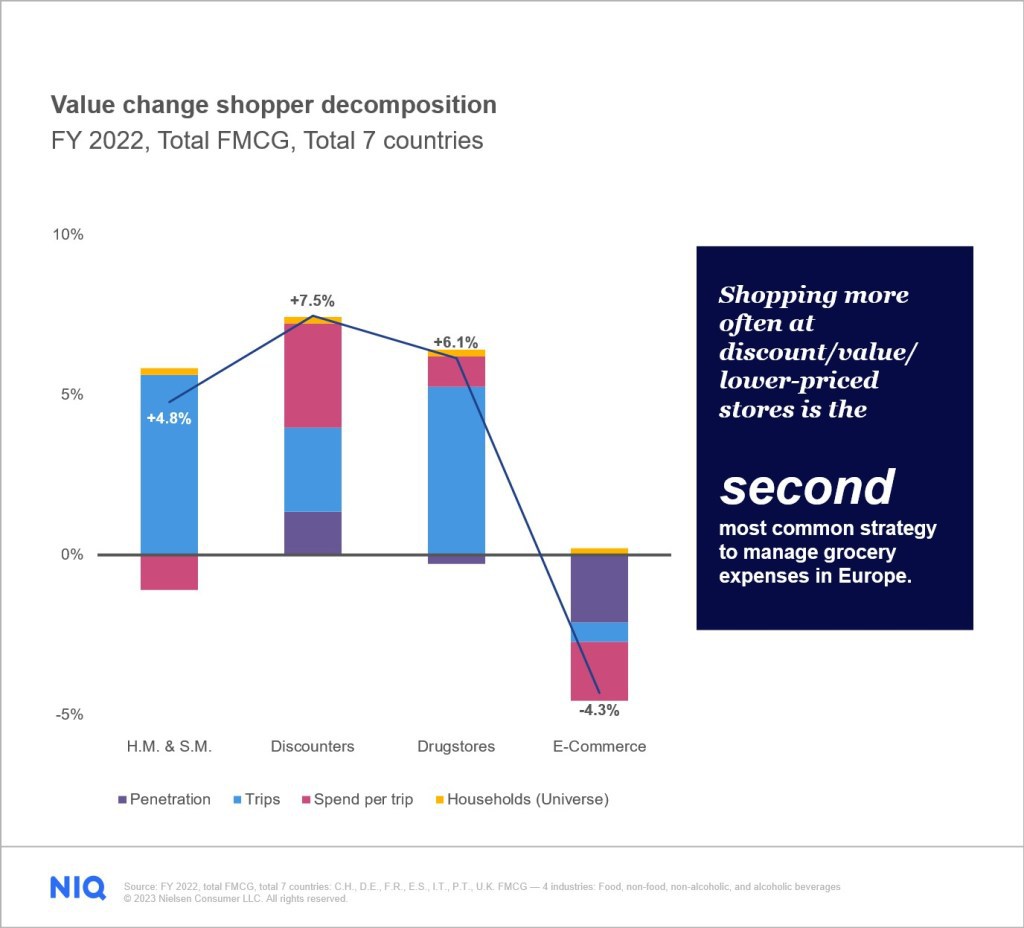

To cope with the rising cost of living, consumers turned to discounters, which provided more affordable options and attracted cost-conscious shoppers seeking budget-friendly purchases. The overperformance of discounters was primarily driven by increased spend per trip, making them a more important shopping destination in the current environment.

Discounters have become market leaders in Poland, with nearly 1 in 4 Polish złoty spent on FMCG products at these stores. This has resulted in more than a 25% increase in channel value.

In addition, discounters were the only channel with a positive volume trend in the food and medication categories. This tendency has also fueled the expansion of private brands, which have surpassed other manufacturing groups and increased their market share by 1%.

Despite a price increase trend, private labels gain traction

By detaining a relevant price gap compared to branded, private labels (P.L.) have an advantage when it comes to transferring increasing costs. According to data from NIQ Retail Measurement Services (RMS) and Consumer Panel Services (CPS) for Great Britain (G.B.), it is visible that private labels are increasing prices ahead of branded in 66% of analyzed locations for European consumers. In other words, there is an overall shortening of the price gap between private labels and branded products, making branded products relatively more competitive than private labels.

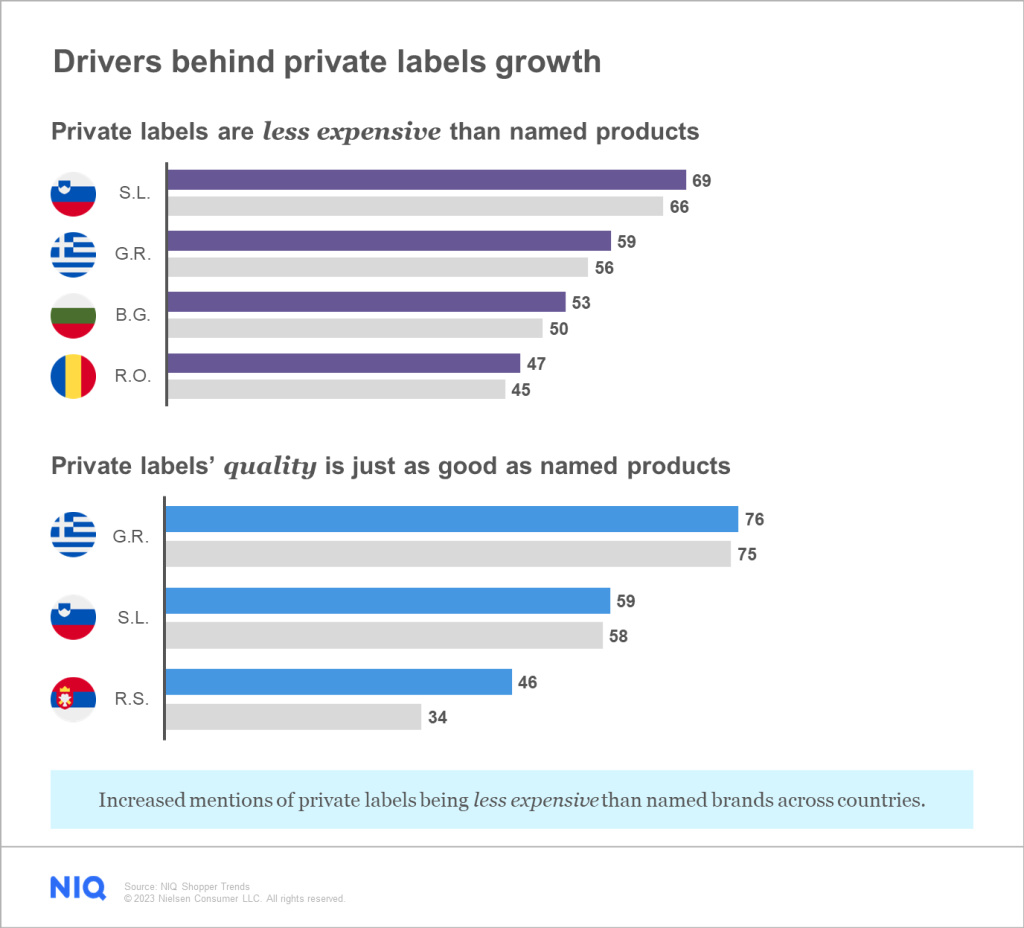

Private labels have grown significantly in Eastern Europe, as customers perceive them as less expensive alternatives to name brands while also establishing a reputation for higher quality. Private labels continue to accelerate in accordance with customers’ focus on value for money, growing at twice the rate of the overall market.

93% of shoppers reported having purchased private-label brands. 33% of those questioned said they would increase their private label purchases due to better value for money and improved quality.

The tendency of consumers to attempt to maximize their purchasing power is nearly uniform. Private labels are gaining market shares across the board while discounters continue to dominate. All evidence points to the continuation of this trend, driven by consumer pessimism due to rising living costs.

The pivot towards private labels and more affordable products becomes a true loyalty test for top brands. Only through committed collaboration between retailers and manufacturers can promotions be sustained without reverting to the unprofitable levels witnessed before the pandemic. Effective promotion management and innovations supported by marketing efforts become crucial to preserving consumer excitement and market position.

The cliché is usually true: a crisis can provide the best opportunity for success.

Signs of stabilization in e-commerce

The Polish shopper entered 2023 uncertain about the future and worried about their financial situation in the coming months. According to NIQ’s Quarter by Numbers Report, nearly two-thirds of them said they are investing time and effort to ensure they buy their groceries at the lowest price. Eastern European consumers are shifting their shopping behavior, showing a preference for discount stores and private-label products. Furthermore, they are visiting grocery stores more frequently but are lowering the size of their baskets, focusing on purchasing only needed things.

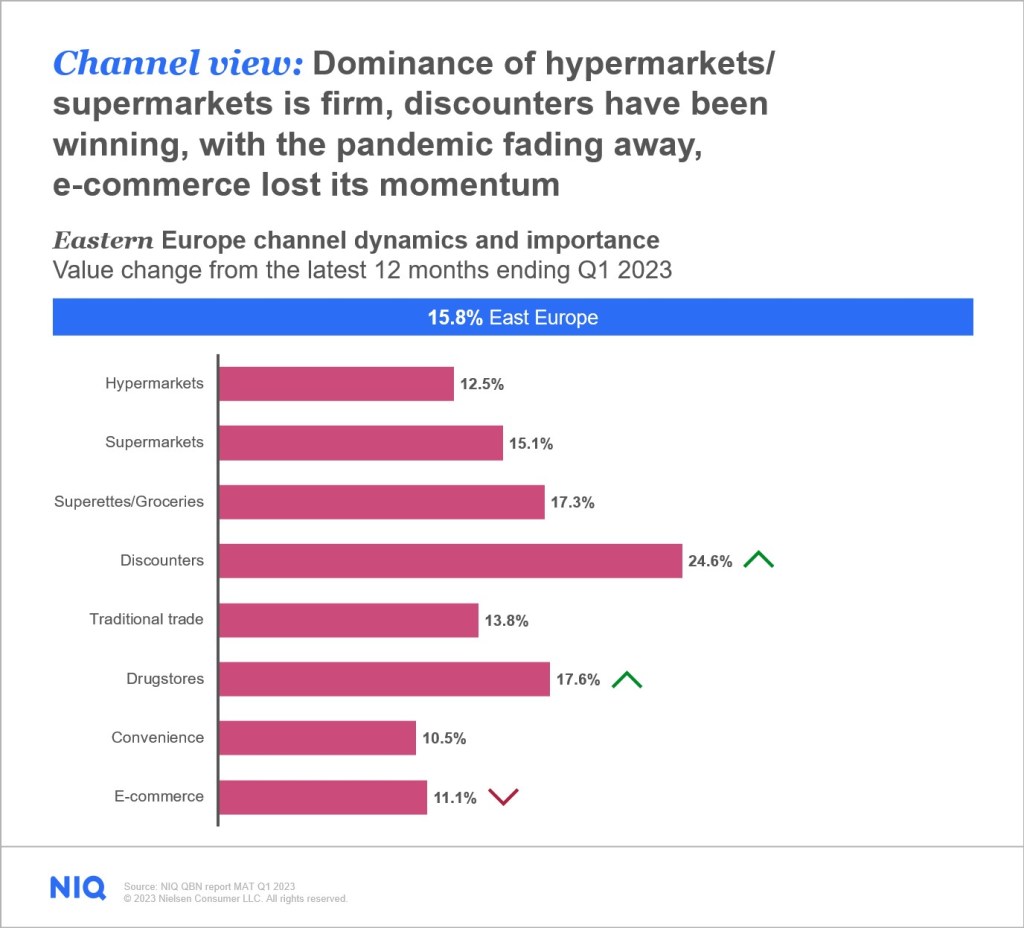

This article shows that while hypermarkets (H.M.) and supermarkets (S.M.) remain dominant, e-commerce growth has slowed as the pandemic recedes. It’s no secret that the pandemic brought with it an e-commerce boom unlike anything we could have predicted. But now, the growth is slowing, and signs of e-commerce stabilization across the world is visible.

E-commerce is still critically important. Because of this, the road ahead relies more heavily on the symbiotic balance of online and offline sales.

Consumers are fluidly fulfilling their needs across channels, and this heightened omni familiarity is what makes the full omni view of retail an absolute necessity for measurement today.

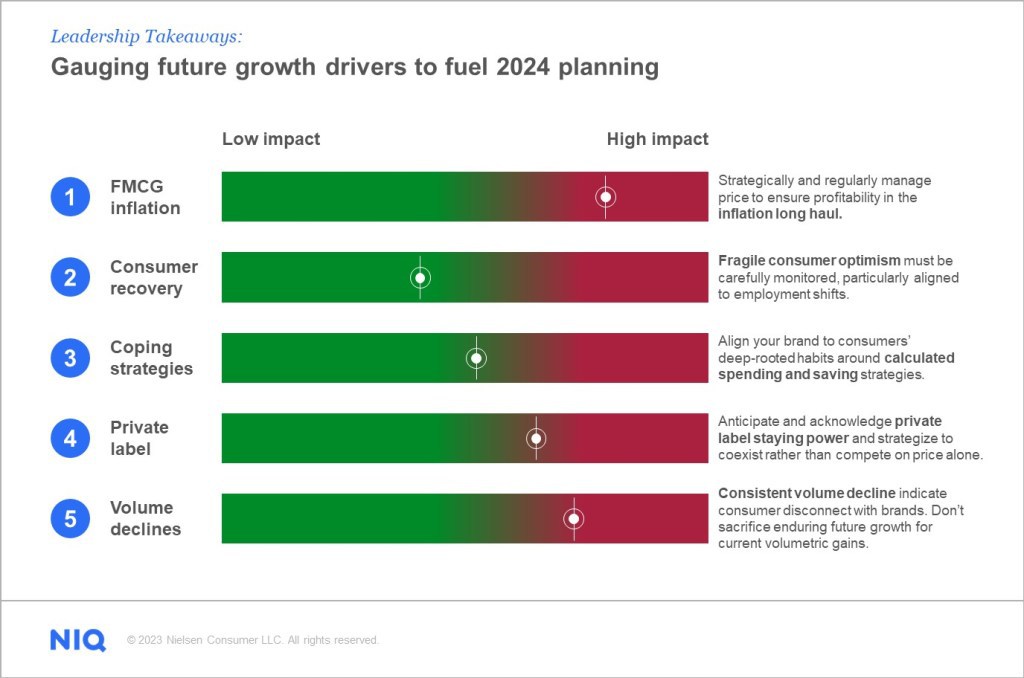

Gauging future growth drivers to fuel 2024 planning

It’s important to monitor future growth drivers and develop strategies to succeed in an evolving marketplace. When considering these, businesses should keep the following bullet points in mind:

- With inflation sticking, it’s important to develop pricing strategies that ensure profitability.

- Consumers are beginning to pull back and remain vulnerable to negative shifts in employment.

- It’s important to align to newly developed spending and saving habits that will continue to define growth opportunities.

- Private labels remain stable and will continue to win over consumer wallets; it’s critical to develop strategies to co-exist rather than compete on price.

- Finally, volume declines will continue, fueled by rising prices. Don’t sacrifice your future growth over short-term volume gains. Promote with a purpose to grow your business profitability while maintaining margins.

Power your business decisions

Navigate the shifts in the retail landscape with the most accurate and trusted data in the industry to grow your business.