Predictions for the golden quarter – spotlight on Black Friday 2023

After a year where many consumers were more cautious with their spending, there will be a lot of brands with high hopes for 2023’s ‘golden quarter’. But capitalizing on this period is likely to be a challenge for many brands and retailers. With consumer spending trends in 2023 pointing to weaker discretionary spending expected in the build up to the holiday season, many brands and retailers will be looking to outcompete their peers from discounting and sales promotion. Accordingly, making the most of promotional events like Prime Day, Black Friday and Cyber Monday 2023 is a top strategic priority.

Just like retailer and brand strategies this year, the big promotional events are dynamic and evolving. This may lead to further changes in the way brands look to boost sales in the final quarter of the year. Let’s look at how this might impact brands both this year and beyond – starting with Prime Day 2023 performance.

What did we learn from the Second Prime Day 2023

In 2022, Amazon introduced a second Prime Day, held in 19 countries on October 10. In 2023, the company expanded this idea by holding its second Prime Day event across two days in October, following on from its usual event in the summer. Called the Prime Early Access Sale, this event was available in 15 countries across Europe, North America, Asia and South America.

So how did this relatively new promotional strategy play out this year?

Demand for the second Prime Day was 0.8% lower than its counterpart in 2022. It was also 5% lower than the traditional summer Prime Day event. However, this only translated to a 0.3% drop in revenue from 2022. This continues to be much higher than 2019. There is also clear evidence that this event does work – the second Prime Day event saw 25% more online sales than an average week.

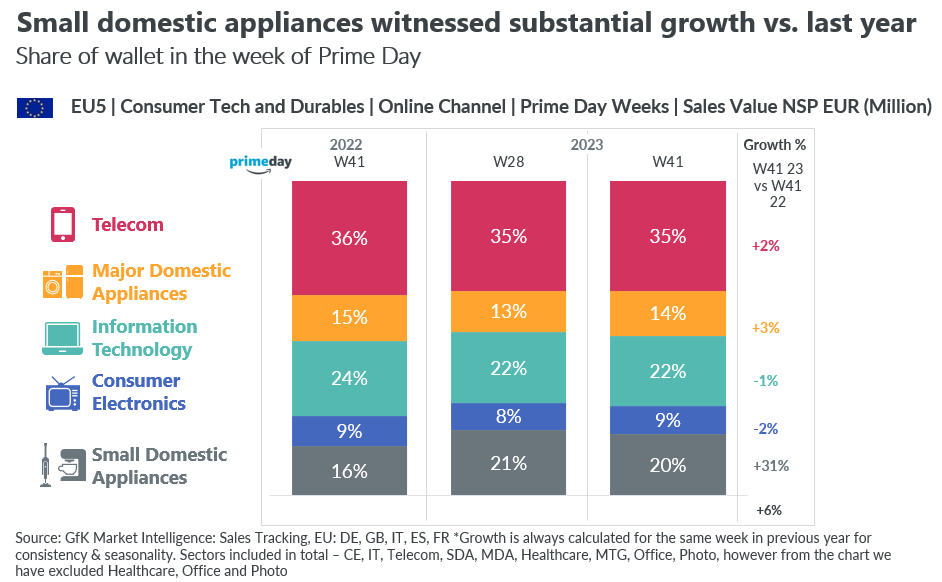

In terms of what products consumers were buying, small domestic appliances (SDA) have been the clear winners this year. The category saw substantial growth compared to last year with a rise from a 16% share of the 2022 second Prime Day wallet to 20%. This contrasts with most other tech and durable categories, which remained relatively stable.

And what is the Black Friday 2023 outlook

The introduction as well as the success of the second Prime Day 2023, in particular for certain categories, is an interesting development in the intense competition of the golden quarter and seasonal promotional events. One potential impact could be a negative effect on Black Friday performance due to consumers already having access to some deals. Whether this materializes is yet to be seen but if it does, the impact is likely to be relatively small.

This year’s Black Friday event is expected to be stable in terms of demand with a slight rise in volume share from 7.6% to 7.9%. But actual growth in volume terms is down by around 10% . So what is actually happening? The market already has low demand and price sensitive consumers are planning purchases and buying products they want during promotions. This is leading to more and more retailers and brands participating in this event. As the contribution increases so does the importance of this year’s event. But in absolute volume terms, it is unlikely to be as successful as last year.

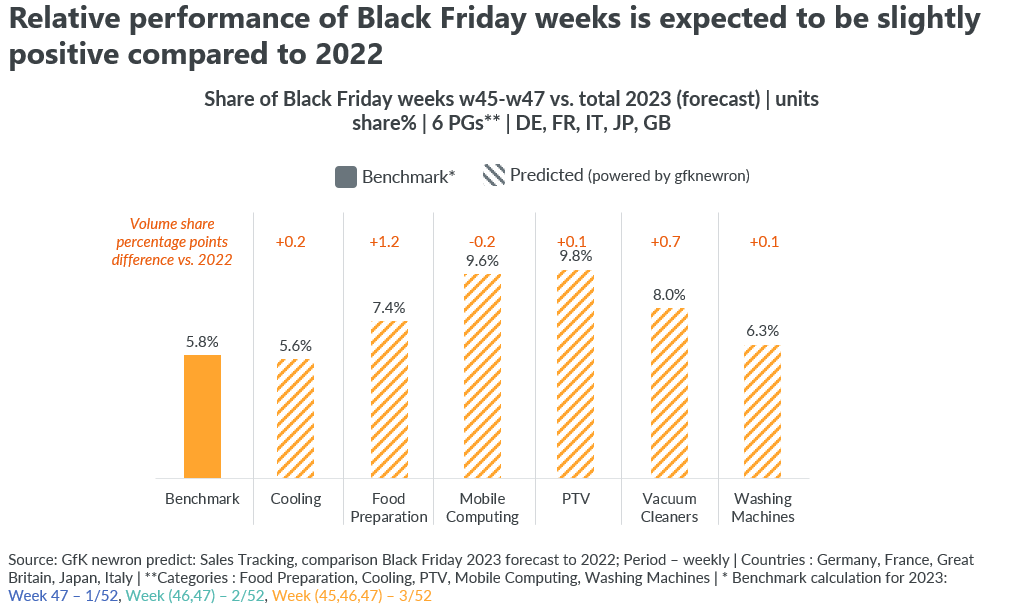

Predictions for this year’s Black Friday across the technical consumer goods (TCG) categories are broadly in line with what we saw during the second Prime Day. All categories are expected to perform higher in terms of contributions than the benchmark – except the cooling category, which looks set to see a slight drop. Once again though, small appliances such as vacuum cleaners and food preparation appear likely to see the biggest opportunities.

What are the key takeaways for brands and retailers?

This year’s golden quarter is going to be challenging for many businesses. With cautious shoppers and the likelihood of lots of brands opting for big discounts, brands need to tread carefully. January is traditionally a time when consumers reign in their spending after the holidays. If this reduced level of discretionary spending continues into the New Year, 2024 is going to be a pivotal year for many businesses.

Here are some ways that brands can build better promotional strategies for the months ahead:

It’s all about value

It is likely that consumers will continue to balance ‘money spent’ against ‘value gained’ when it comes to purchases throughout this quarter. Many will be approaching promotional events with the aim of picking up some great or premium products on deals – but they will have a set budget in mind. Value in this situation doesn’t just equate to price, although that is a crucial factor. Consumers may also be looking for premium features, durability or energy efficiency. For retailers, value may also mean things like fast delivery, bundling and loyalty schemes. Brands and retailers need to make sure they are promoting the benefits of their products rather than just the price in order to differentiate themselves from the competition.

The run up to Black Friday is critical

The countdown to Black Friday has already begun. The last two years have seen the importance of pre-Black Friday events grow steadily and this year is likely to continue that trend. A 0.4 percentage points rise in sales is predicted across the two weeks prior as well as the Black Friday week itself. Many retailers have begun to offer discounts and offers before the official Black Friday 2023 weekend arrives. This can be an effective strategy. Brands may wish to offer discounts early to stand out, or cement loyalty by offering exclusive deals to existing customers first.

Performance will vary across categories

While overall performance is expected to be slightly positive and will be able to uplift the demand within this year’s volume dynamics, some categories are likely to have more relative gains than others. Categories such as food preparation and vacuum cleaners are predicted to see a boost in sales. This fits with the common theme of consumers looking to make each purchase count and taking this opportunity to pick up some essential household items at a lower cost. There is also going to be some divergence when it comes to people’s willingness to go premium. In the first Prime day, we saw premiumization in online channels. Conversely, the second Prime day saw premium in one sector and affordable premium pricing in others – with a fall in major domestic appliances (MDA) premium sales not mirrored in sales of premium SDA products. This poses an interesting question for both brands and retailers about the role of private labels that offer affordable premium pricing.

Solid strategies require solid data. gfknewron can help you keep up to date with changes in your market.