Report

The Commerce Revolution: Where East Meets West

How Eastern platform innovations and Western retail media are converging to reshape the global commerce landscape—and defining commerce intelligence along the way

Key takeaways

- Commerce is evolving beyond channels but is benefiting from the infrastructure built to support channel-driven growth. It’s transitioning into an integrated system where consumer discovery, transaction, and fulfillment move as a unit.

- The East’s and West’s paths are now running in parallel, forming complementary halves where the strength of each will fuel the next wave of growth for brands and retailers.

- The fastest-growing “channels” (live commerce, social commerce, and quick commerce) no longer operate in silos. Consumers will increasingly expect these experiences to feel integrated and to guide them through a cohesive shopping journey.

- A competitive edge will belong to brands that can leverage best-in-class data to operate within this unified system—transforming that data into commerce intelligence that shapes how demand is generated, captured, and measured.

A welcome from Marta Cyhan-Bowles

Commerce is no longer evolving in channels—it’s being rebuilt as a connected global system.

While the West has traditionally embraced data-rich retail ecosystems, the East has focused on rapid platform innovations, leading the way for emerging channels. As these two distinct models converge, we’re quickly moving toward a new global commerce framework—one powered by artificial intelligence (AI) and increasingly shaped by agent-driven decisioning, fundamentally shifting how consumers discover and purchase products, and how brands and retailers reach them.

While this shift creates a significant opportunity for manufacturers and retailers to deliver more personalized, relevant products and experiences to consumers, it also introduces new challenges across targeting, optimization, and measurement.

That’s what makes this moment—and this report—so critical. The Commerce Revolution: Where East Meets West not only provides retail and brand leaders with an in-depth analysis of the convergence between Eastern and Western commerce models—and the AI-driven technologies born of it; it also outlines the data, solutions, and insights they need to build commerce intelligence and capture share during this period of rapid transformation.

Our teams are ready to help your business thrive as consumer behaviors evolve, expectations rise, and the need for a unified view of the consumer becomes even more critical. If you have questions about our data, research, or how to navigate this increasingly global commerce landscape, we welcome the conversation.

Discover how Eastern platform innovations and Western retail media are converging to reshape the global commerce landscape—and defining commerce intelligence along the way. Watch our preview and then read The Commerce Revolution: Where East Meets West.

Retail’s center of gravity is shifting

Global retail markets have developed at different speeds—largely driven by evolving consumer behavior trends and technology investments in each region. Format-led behaviors emerging from the East—including payment architecture, logistics capabilities, and digital channel expansion—are becoming increasingly linked with the monetization and commerce media systems of the West. This convergence has been further accelerated by AI and its ability to track, automate, and personalize the shopper journey—unlocking deeper consumer insights across channels and platforms.

Notably, AI is beginning to function as a decision engine for consumers through agentic commerce models—learning behaviors over time, interpreting intent, refining recommendations, and increasingly influencing or executing purchase decisions on the shopper’s behalf.

What’s emerging is a new model of consumer influence and value creation driven by more precise and continuously evolving demand signals. This blending of models is poised to reshape how manufacturers and retailers achieve lasting growth over the next five years.

The channel landscape

To ground this shift, we must first understand today’s “channel” landscape—and how consumers engage across it, even as the boundaries between channels begin to erode.

In Western markets, we see widescale adoption and usage of retail media platforms. Indeed, in the US today, more than 22% of total media budgets are now allocated to retail media campaigns, with brands, on average, distributing that budget across six retail platforms—a figure projected to grow to eight by the end of 2026.1 Yet both execution and measurement remain fragmented, largely by campaign and retailer—with 77% of organizations reporting they’re seeking better measurement solutions and 68% reporting they’re actively seeking efficiencies.2 These challenges are further compounded by the proliferation of large language models (LLMs) and agents shopping on consumers’ behalf.

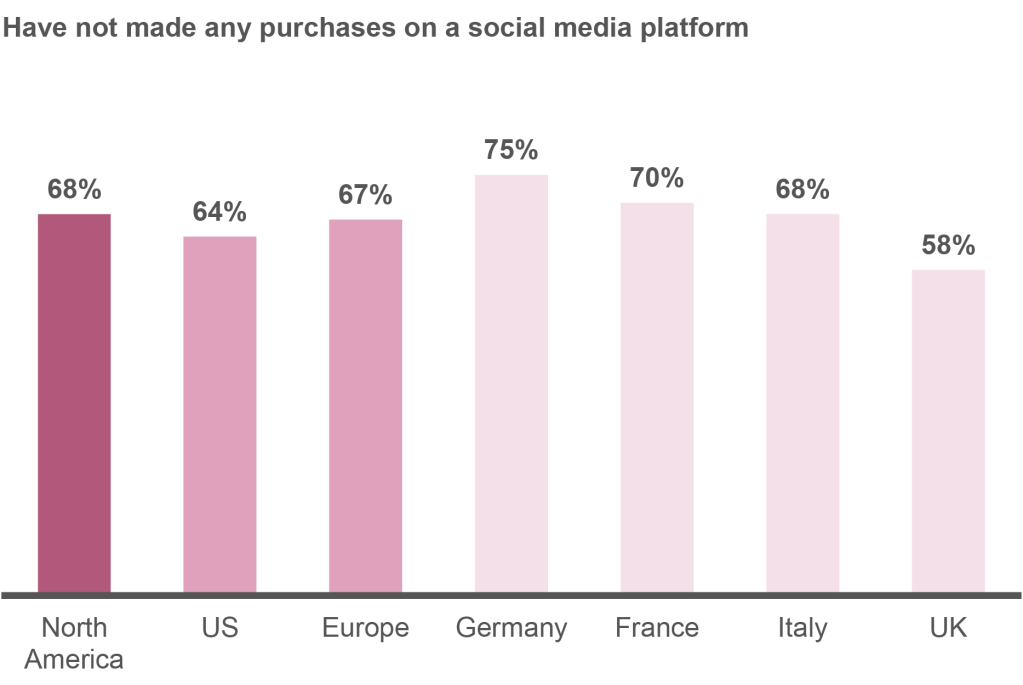

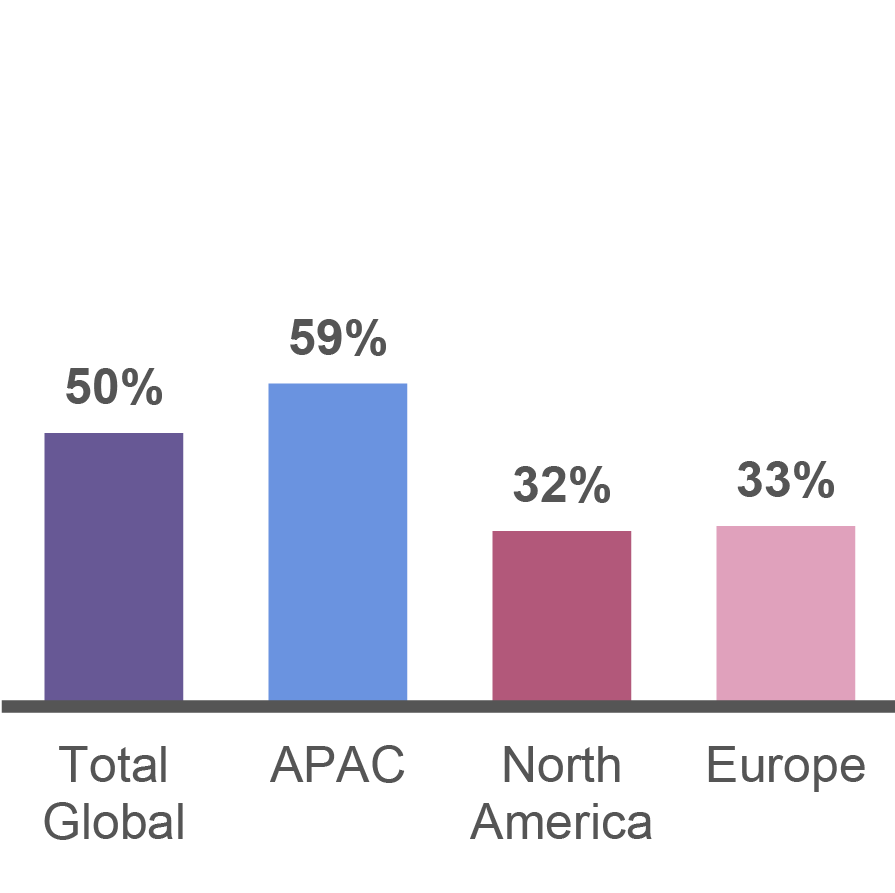

Notably, we also see relatively low penetration in Western markets across key digital channels currently driving growth in the East—with roughly 69% of North American consumers and 66% of European consumers having never used quick commerce; 67%–68% having never purchased via social media; and only 10%–13% reporting increased social and live commerce usage.3 But consumer adoption is accelerating.

Conversely, in Asia Pacific (APAC), 58% of consumers have adopted quick commerce and 59% are using social commerce.4 Also critical to note is that social and live commerce in the East are becoming increasingly intertwined, as live commerce is often hosted on social apps like Douyin, Kuaishou, and Xiaohongshu.

While consumers in APAC are leveraging retail media, it remains far from the campaign-driven approach seen in the West. “Super apps” embed retail media within a cohesive platform, enabling hyper-personalized experiences and the development of deep user profiles.

Further differentiating this model is the advanced use of AI, through which platforms both capture purchase intent and stimulate demand—reinforcing a system in which commerce is continuously optimized around the individual consumer.

What can appear today as fragmented channel growth is, in reality, the early stages of a connected global commerce ecosystem—with the consumer at the center. In the East, platforms have married discovery, content, and purchase into a single consumer model. In the West, retail media networks (RMNs) have built monetization and measurement infrastructure to scale that model. AI is now the connective tissue between the two. As this continues to develop, commerce will no longer be a set of discrete channels or functions, but rather an integrated, continuously optimizing, intelligent ecosystem.

So when we discuss a unified commerce system, we’re conveying that three forces are colliding—and will redefine growth in the modern commerce era:

- A robust infrastructure that facilitates commerce at record speed

- Content experiences that transcend channel and format

- AI-driven technologies that deliver across both at unprecedented speed and with hyper-personalization

As it specifically relates to the opportunity for brands and retailers, commerce intelligence—the ability to connect what brands and retailers need to know, what consumers need to discover and decide, and how platforms operate through a unified, data-rich view of the ecosystem—will redefine how consumer demand is generated, captured, and measured.

- Skai x Stratably 2026 State of Retail Media Study

- Skai x Stratably 2026 State of Retail Media Study

- NIQ 2025 Consumer Outlook survey

- NIQ 2025 Consumer Outlook survey

Read the full report now.

Premium chapters

What’s happening in the East

APAC remains the global leader in e-commerce, accounting for almost 55% of global revenue in 2025. But more importantly, when we examine its digital scale, it clearly reflects the most advanced expression of a commerce “system” where discovery, engagement, purchase, transaction, and fulfillment operate as one.

Much of this growth is driven by continued investments in developed channels such as live commerce, social commerce, and quick commerce. Markets like China, India, Indonesia, and South Korea offer clear examples of what’s happening across the region today—and what’s likely to continue moving West in the years ahead.

Critical to note: While describing growth often necessitates highlighting distinct “channels,” live, social, and quick commerce in APAC increasingly function as interconnected arms of a single ecosystem. We will therefore break down growth and trends through the lens of each channel below.

Live commerce

The East has the most mature live commerce market, where creators showcase hundreds of items per session.5 Live commerce operates at high velocity, with APAC creators using ultra-short formats—some as brief as three-second product showcases—and individual livestream posts that can generate up to $111,000 in earned media value (EMV).6

Live commerce experiences born in the East continue to demonstrate large-scale impact for brands. For example, SKIMS’ December 2025 Kimsmas Live! TikTok Shop event attracted more than 678,000 viewers and generated roughly $127,000 in gross merchandise value (GMV) in under an hour. These successes also underscore that performance increasingly depends on cross-platform execution—with “live” content experiences taking place across social media platforms and being amplified by influencers who have built their audiences on those platforms.

Microdramas are another highly profitable content format delivered through social media platforms in a “live” format. They began in China and have gained popularity across Southeast Asia, with Singapore becoming a hub for production. The business model is “pay as you go” after getting a consumer “hooked” on several free episodes. For brands, the big ROI is showcasing the products they sell in the ads viewers watch to move to the next chapter of each drama—a model consumers in the West experience through mobile gaming.

What’s more, these ads are cheap for brands to produce—especially with AI delivering highly cost-effective content. For the user, this experience provides a frictionless journey, fueled by AI, where product discovery, brand engagement, and purchase are inextricably woven. Platforms like Douyin (the original Chinese version of TikTok), Kuaishou, Xiaohongshu, Instagram, and YouTube now host these serialized microdrama formats.

- WeArisma

- WeArisma

Market view

Across APAC, China is the most mature live commerce market. By 2023, an impressive 57% of live commerce users in the country had already shopped the format for three years, and first-time users made up just 2% of live users. China also boasted the highest share of frequent live users, with 87% attending events once (or more) per month. To put this into perspective: The live commerce market in China is $900 billion (USD)—nearly the same size as the entire e-commerce market in the US.

Despite these impressive numbers, counterintuitively, brands’ live commerce investments in China are on the decline. This isn’t a reflection of the efficacy of the channel, but rather an adjustment in how brands are maximizing ROI at scale across it. As the cost of advertising has exploded, brands have shifted their strategy to introduce new products and SKUs via the channel—building early brand awareness—and then pivot quickly to reallocate the dollars to more cost-effective offline channels once awareness is built. As such, live commerce is shifting from a conversion engine to a margin-negative awareness play.

One notable exception is the Beauty category, where structurally higher margins enable brands to maintain live commerce as a viable long-term investment, supporting both awareness and sustained conversion at scale.

Also worth noting is the shift of live commerce dollars in China from key opinion leaders (KOLs)—valued thought leaders within a specific industry or area of expertise—to a decentralized group of “everyday” influencers who are reaching niche audiences.

South Korea is another significant market for live commerce. The channel is projected to grow in South Korea at an annual rate of 36% through 2030, to reach nearly $4 billion. It should come as no surprise that the country was a very early adopter of live commerce, upholding its reputation for rapid technology adoption.

Three key forces will continue to drive this forward:

- AI-driven efficiency: AI will continue to redefine live commerce by shifting the focus from manual production to algorithmic efficiency. AI-driven virtual hosts, real-time script generation, and AI-produced advertisements will enable 24/7 hyper-personalized broadcasting and product placements, significantly reducing operational overhead while maximizing consumer engagement through data-led, instant responsiveness.

- Direct to consumer (DTC) enhancements: Leading consumer brands will increasingly leverage live commerce as a tool to strengthen their competitive edge. By pivoting toward DTC channels, brands can secure first-party data ownership and build deeper loyalty, ensuring sustainable margins in an increasingly fragmented retail environment—mirroring the approach more typically seen in the West.

- Convergence of quick service restaurants (QSR) and fresh food: Live commerce will transcend traditional retail categories, becoming a channel for QSR and fresh grocery. The synergy between live streaming and “last mile” delivery infrastructure will transform the medium from a mere discovery tool into a high-frequency, frictionless fulfillment channel for immediate consumption.

Much of the growth in South Korea can be attributed to the confluence of live commerce and the robust creator and influencer space. The average consumer in South Korea is also spending more time on social media than any other country, at three hours per day. The major players for live commerce here include Naver, Coupang, and Kakao.

Although China and South Korea are further along in their adoption of live commerce, both India and Indonesia are exhibiting signs of growth.

In 2025, India’s live commerce market was valued at $7 billion; by 2034, it’s projected to reach nearly $215 billion, growing at a compound annual growth rate (CAGR) of nearly 45%. This growth will be driven by social media proliferation, influencer-led shopping (particularly in the Fashion, Beauty, Lifestyle, and Wellness categories), and widespread smartphone adoption, highlighting the codependent growth between social media platforms and live commerce.

Notably, consumer trust remains a major barrier to widespread live commerce adoption in India. Many shoppers are reluctant to buy directly from standalone live commerce apps due to concerns over product authenticity, returns, and platform reliability. Traction is strongest on established, trusted ecosystems like YouTube, Instagram, and large marketplaces that already offer secure payments and reliable return policies. The market opportunity here is real, but widespread adoption will depend on stronger buyer protection, verified sellers, and platform-backed trust mechanisms.

In Indonesia, the live commerce market is expected to grow from $5.7 billion in 2026 to $8.7 billion by 2031, at a CAGR of 8.71%, fueled by the same market dynamics at play in the other countries analyzed. Categories leading this growth include Fashion and Lifestyle, which accounted for nearly 23% of market share in 2025, as well as Grocery and fast-moving consumer goods (FMCG) products such as fresh produce, frozen food, and household staples.

Key takeaways

When examining a single channel like live commerce in the East, rapid evolution and convergence with adjacent channels are already underway.

- In emerging markets such as India and Indonesia, where adoption is still developing, brands have an opportunity to establish an early presence and capture share as the ecosystem matures.

- In more advanced markets like China and South Korea, the focus shifts toward optimizing investments—diverting spend toward decentralized creator ecosystems, moving beyond reliance on high-cost KOLs, and pairing live commerce with complementary channels that improve overall return on investment.

Migration West

Live shopping is gaining traction in the West as social platforms and retailers create interactive shopping features, but the market is still in its infancy. In 2023, just 5%–7% of consumers surveyed in Europe, Latin America, and the US shopped on live commerce apps. In 2025, 10%–13% of surveyed consumers in Europe and North America reported increased purchase through live commerce on social platforms—up from 9% and 10%, respectively, the previous year—indicating steady growth across these channels.7

Users in the West also participate less frequently than in more mature markets like China. Just 43% of users in the US said they’d shopped live at least once in a given month. Europe and Latin America were slightly higher (at 52% and 64%, respectively), but nowhere near the 87% seen in China.

The biggest opportunity for retailers in the West is to leverage live shopping to transform passive browsing into real-time, personalized engagement. Users in the East interact more frequently, and impulse purchases are very common. However, success in both markets depends on fully integrating behind-the-scenes content, founder/owner participation, and a full commerce content funnel rather than isolated events (“lives”).8

TikTok will continue to be a major player in live shopping as it expands its capabilities into more countries in the West and deepens its role in the social commerce landscape. Walmart and Amazon are both making significant investments in this space to capitalize on these opportunities. Livestreaming is also assisting established players like eBay with revitalizing engagement as sellers leverage its robust ecosystem of product reviews and tutorials.

Whatnot, which specializes in selling collectibles through livestreams, has also quickly emerged as a major player in the space. The company generated $6 billion in GMV last year, and its shoppers spend more time a day watching content than the average person spends on YouTube and TikTok. The app is currently available in the US, UK, Europe, and Australia.

Along with Western brands and platforms leaning into live commerce, major players out of the East are accelerating growth in the West by expanding into the region. TikTok serves as a prime example. JD.com is another, with the top Chinese retailer expanding into Europe and quickly becoming a global omnichannel powerhouse. (For more on JD.com, see the case study below.)

Western lives are also being influenced by talent from the East. Fashion Weeks and other tentpole events are capitalizing on the fanbase of celebrities from China, South Korea, and Thailand to generate outsized earned media value (EMV) in the West.9

Live commerce performance in the West is still very category-specific, however. Many retailers are following the Eastern playbook and investing in Beauty and Fashion categories due to their strong margins and performance. When examining TikTok performance, it’s therefore unsurprising that both are top-selling categories on the channel.

- NIQ 2025 Consumer Outlook survey

- WeArisma

- WeArisma

Key takeaways

As platforms integrate commerce capabilities directly into content ecosystems, brands that successfully blend storytelling, creator engagement, and transactional experiences will be best positioned to capture growth.

Live and social commerce saturation is far from mature in the West. Brands that make early investments in live content formats across social platforms are well-positioned for significant growth in the mid- and long term.

Social commerce

Outside of “lives,” there’s significant growth occurring on social platforms in other content formats. Over half of all consumers in APAC make purchases through social commerce, while the West remains less mature, with roughly one-third of consumers in both North America and Europe purchasing via social commerce.

And as the global social ecosystem continues to evolve, discovery is increasingly shaped by AI-driven recommendations rather than solely user-dictated journeys. Within this environment, early signals of agentic commerce are emerging, in which AI is beginning to function as a decision engine—not only surfacing hyper-relevant products but interpreting consumer intent and prioritizing options. While social platforms remain the primary layer for discovery and influence, agentic solutions are starting to shape how consideration sets are formed and, ultimately, how demand is generated within social commerce.

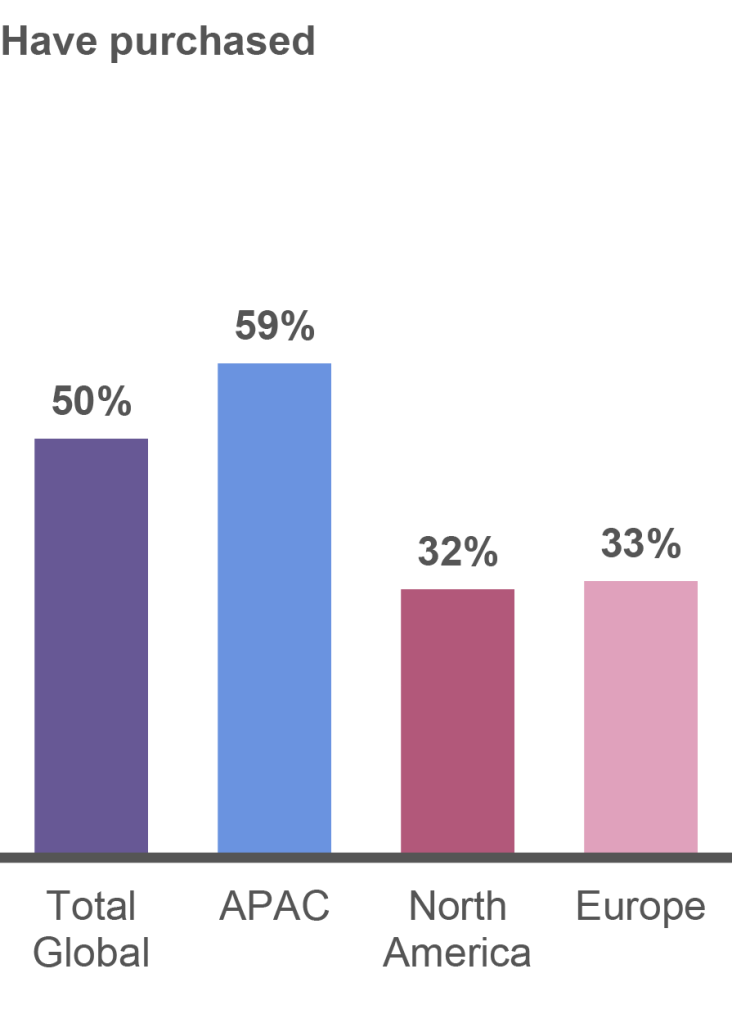

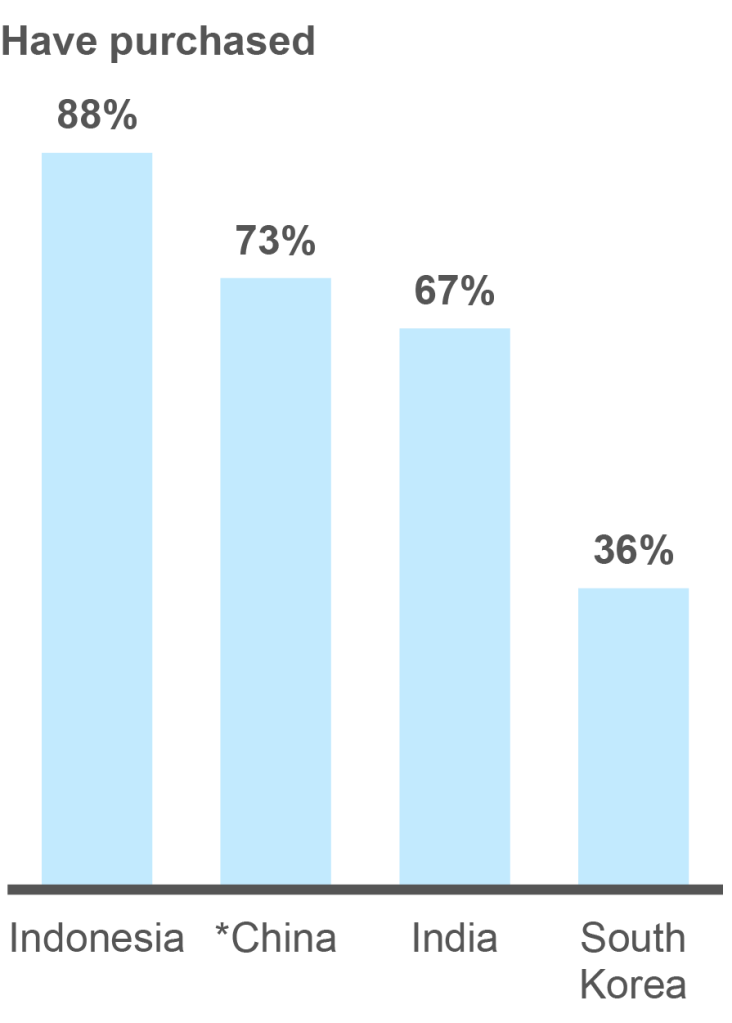

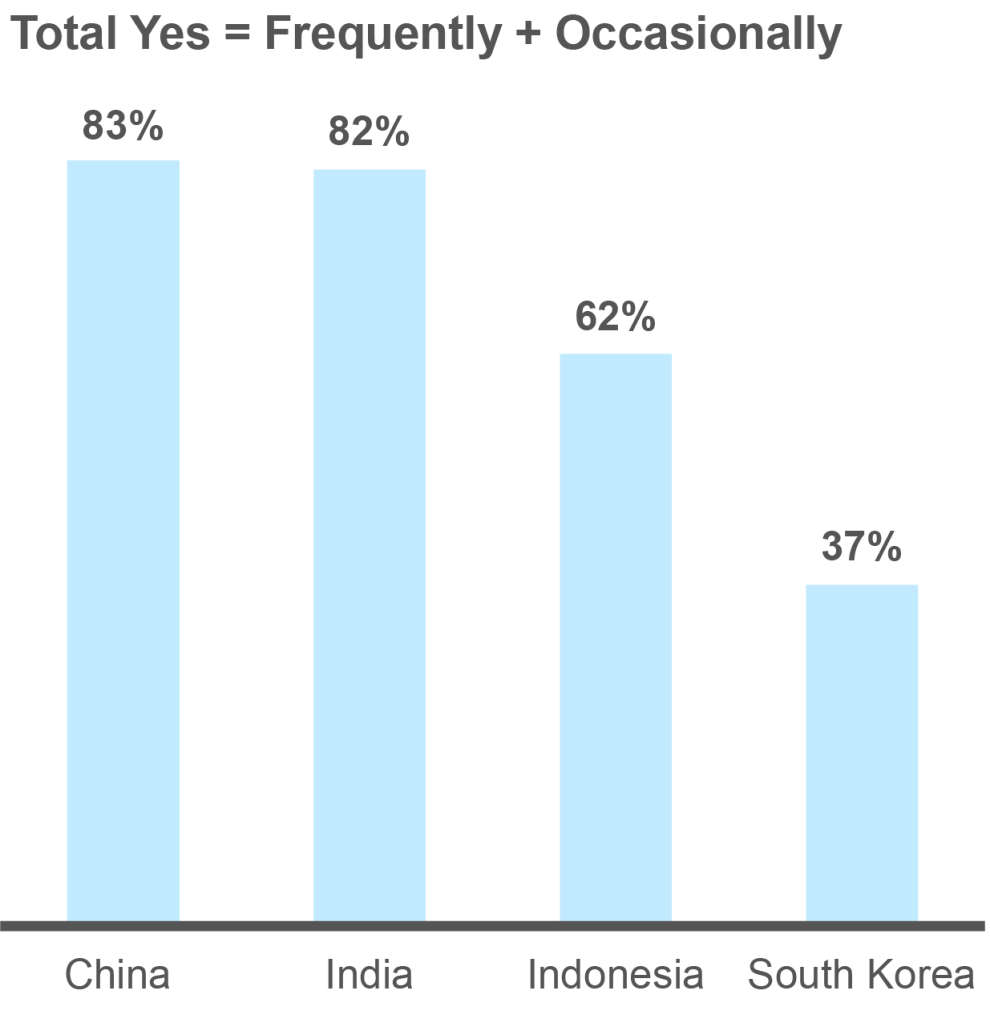

A clear runway to grow: Social commerce is mainstream in APAC, still early‑stage in the West

Q: Have you ever purchased a product directly through a social media platform?

*China figures reflect minimum reported social commerce participation based on the highest platform reach

And because social commerce can’t be viewed in isolation from the live commerce market, it should come as no surprise that China is a leader in social commerce, with India and Indonesia also seeing impressive growth and rising penetration.

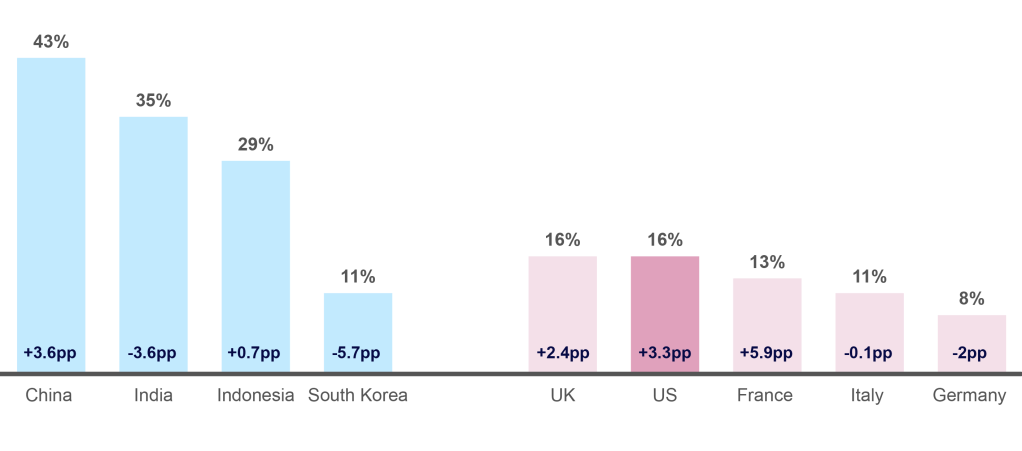

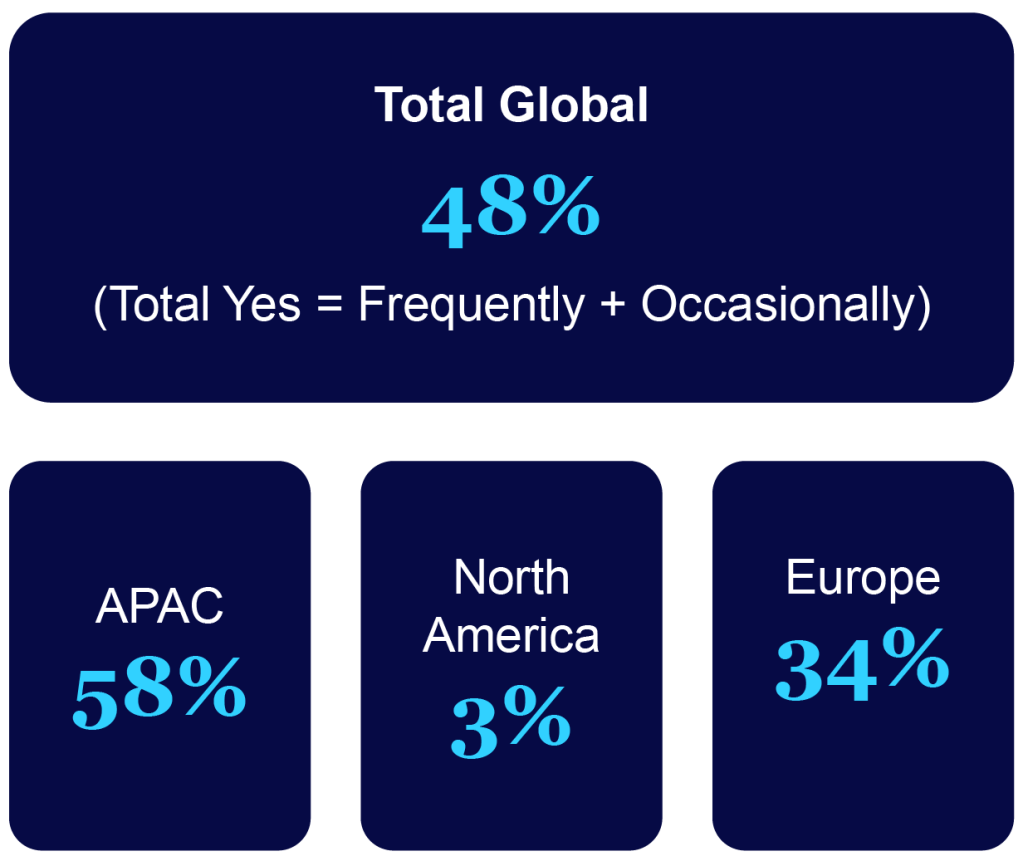

Signs of convergence in social/live commerce penetration worldwide

% of respondents who said they shopped more for everyday grocery items via social/live commerce channels vs. the prior year

Percentage point change vs. year ago

When we look at global social media investment by CPG/FMCG brands, the average share of spend is 27.4%, and the average ROI is $1.35.10 However, 58% of brands are seeing an ROI under $1. Influencer investment, which is often allocated to social media budgets, is under 10% share of spend, but performance is also lower, with a $0.68 ROI.11

- NIQ social media norms

- NIQ social media norms

Market view

Examining notable markets across APAC, China demonstrates what scaled convergence looks like when content, platform, and transaction are fully integrated. Its social ecosystem includes major players such as Douyin, Xiaohongshu, and WeChat Mini Programs.

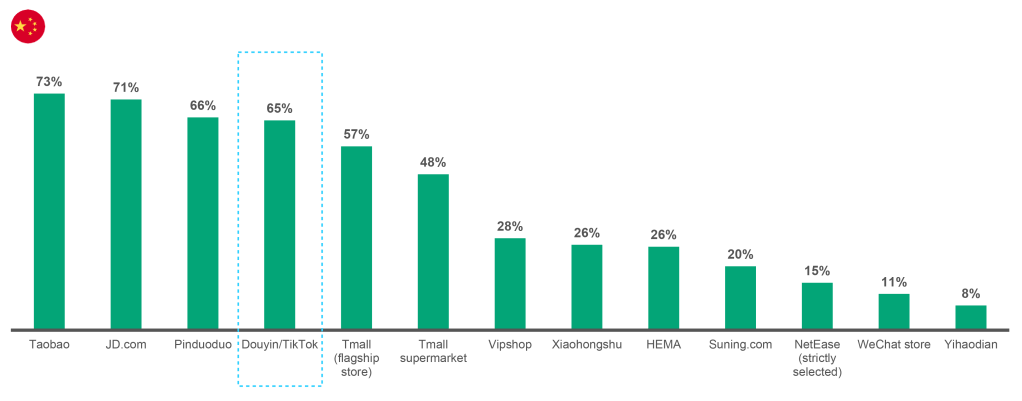

Which platforms Chinese consumers are using when they buy

In China, most purchases still come from major buying apps like Taobao (73%), JD.com (71%), and Pinduoduo (66%). Yet, despite being a social media platform, Douyin/TikTok has broken into the top 5 purchase channels (65%), standing alongside traditional e‑commerce leaders.

Today, China’s social commerce market in China is valued at approximately $500 billion and is projected to reach $1.8 trillion by 2030. While early growth was driven by celebrity influencers, the next wave is being fueled by a more decentralized creator ecosystem, where influencers at scale drive sustained engagement and conversion.

South Korea also has a mature creator and influencer economy. It’s estimated that upward of 70% of consumers in the country discover products through social media. South Koreans are also buying—with sales reaching over $21 billion in 2024.

South Korea is already a mobile-first market, with almost three-quarters of online sales happening on a mobile device. As more social platforms integrate e-commerce capabilities, the channel is anticipated to see a CAGR of 13% through 2030.

Indonesia is one of the largest social commerce markets today, with TikTok and YouTube accounting for over three quarters of all its digital transactions. The market is expected to reach an impressive $22 billion GMV by 2028. Driven by young, tech-savvy consumers, this fast-growing channel is helping brands convert three times higher than traditional e-commerce platforms.

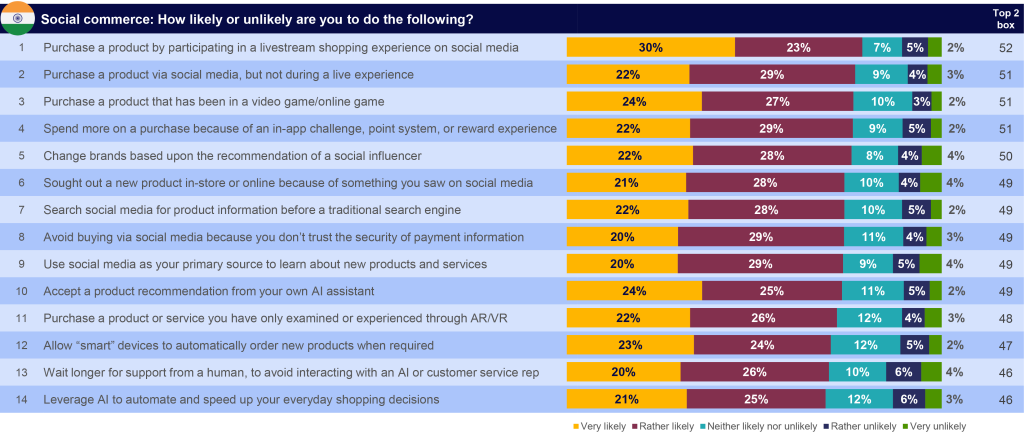

India has seen a mild deceleration in growth rates but is still growing; around half of consumers use social media to research products before they purchase. Just over 50% of consumers are also likely to purchase through social.

Product purchase via social media (with or without livestream) has emerged as the most popular activity in India. But trust and tech comfort are deterrents.

Base: All online grocery shoppers, 2025 (n=1714)

Ref QXX6: How likely or unlikely are you to do the following?

Unsurprisingly, the young population of consumers who are active on social platforms will continue to create opportunities for brands to grow in India, and projections put social commerce growth in India at a 10.3% CAGR through 2030, potentially valuing the market at $14 billion.

Key takeaways

Mature social commerce markets demonstrate how powerful the channel becomes when content, creators, and commerce infrastructure operate within the same ecosystem—but delivering measureable ROI remains paramount. Lessons from markets such as China and South Korea show how brands can accelerate a full-funnel commerce model.

As adoption expands across emerging markets, companies that invest early in creator ecosystems and integrated content-commerce strategies will be best positioned to capture future growth.

Migration West

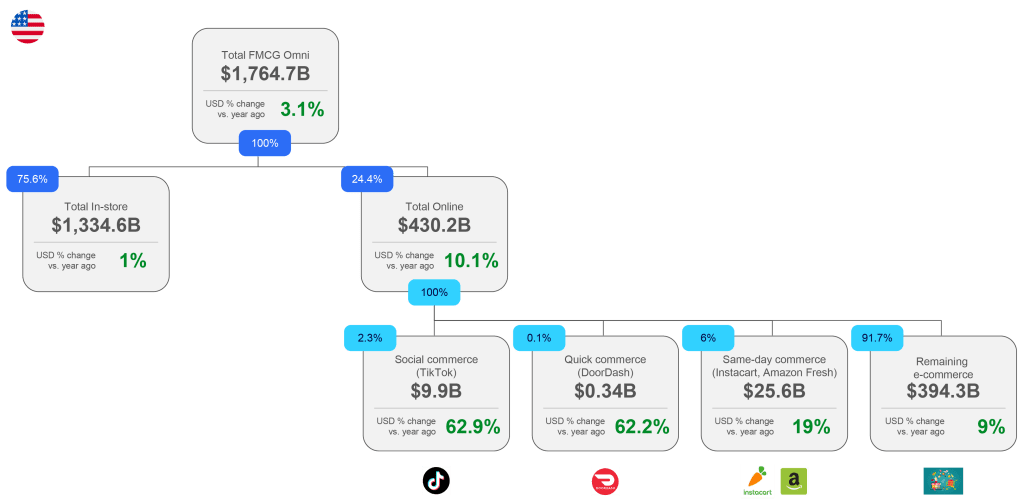

Social commerce is one of the few channels where brands are seeing incremental growth for FMCG in the West. In the US, for example, traditional e-commerce growth is up 9%, while social commerce (+62.9%) and quick commerce (+62.2%) drive most incremental growth—despite accounting for less than 10% of online FMCG value.12 The platform infrastructure is nowhere near as robust as it is in the East, however. Additionally, many consumers still view social media as a way to connect with individuals—not brands. As such, when it comes to buying decisions, trust in the platform is low.

It’s understandable, then, that social commerce is just a small piece of total retail e-commerce in large Western markets like the US. It’s growing, however, and could make up 10% of US retail revenue by 2030 if growth projections hold. This trajectory would see the market go from roughly $87 billion today to over $100 billion next year.

Even though many consumers in the West aren’t yet buying through social media, their purchase decisions are increasingly influenced by the channel. Almost one-third of consumers in Germany, the UK, and the US say they’ve purchased a product after learning about it through social.

The migration of Eastern platforms into Western markets is also driving growth. TikTok Shop, now live in 17 markets, captured 18.2% ($15.82 billion) of the social commerce market in the US last year. It’s expected to gain another 6% of the market within the next two years. The broader TikTok platform is also expected to grow its user base to 50% of all social buyers in the US by the end of this year. Some of this growth may be fueled by potential changes in ownership, which could encourage data-aware consumers to join the platform.

- NIQ US Omnisales

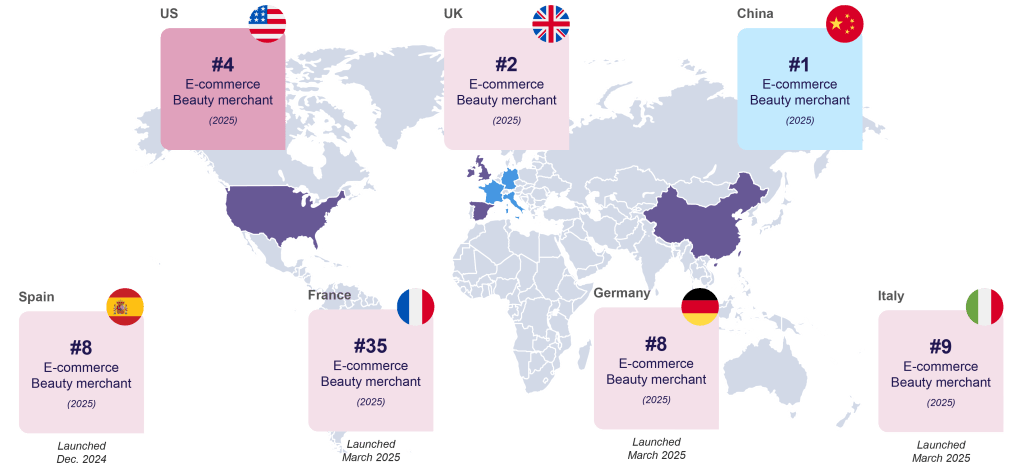

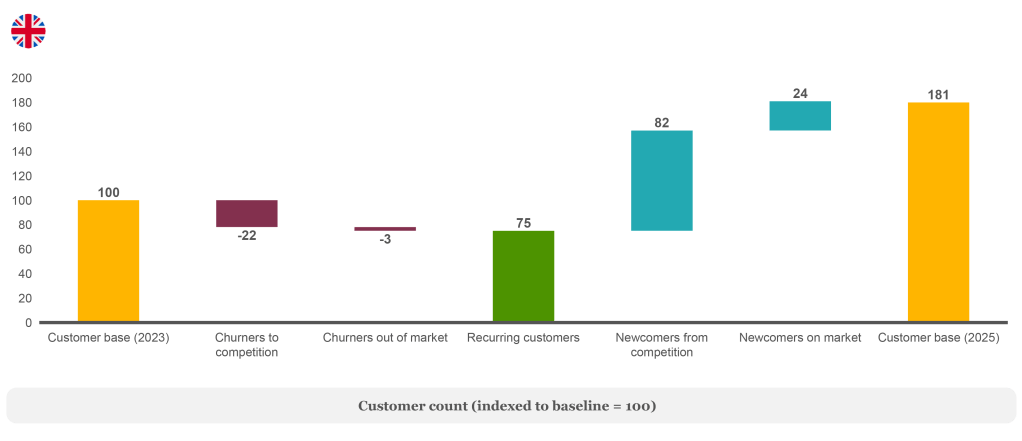

TikTok Shop continues its global expansion

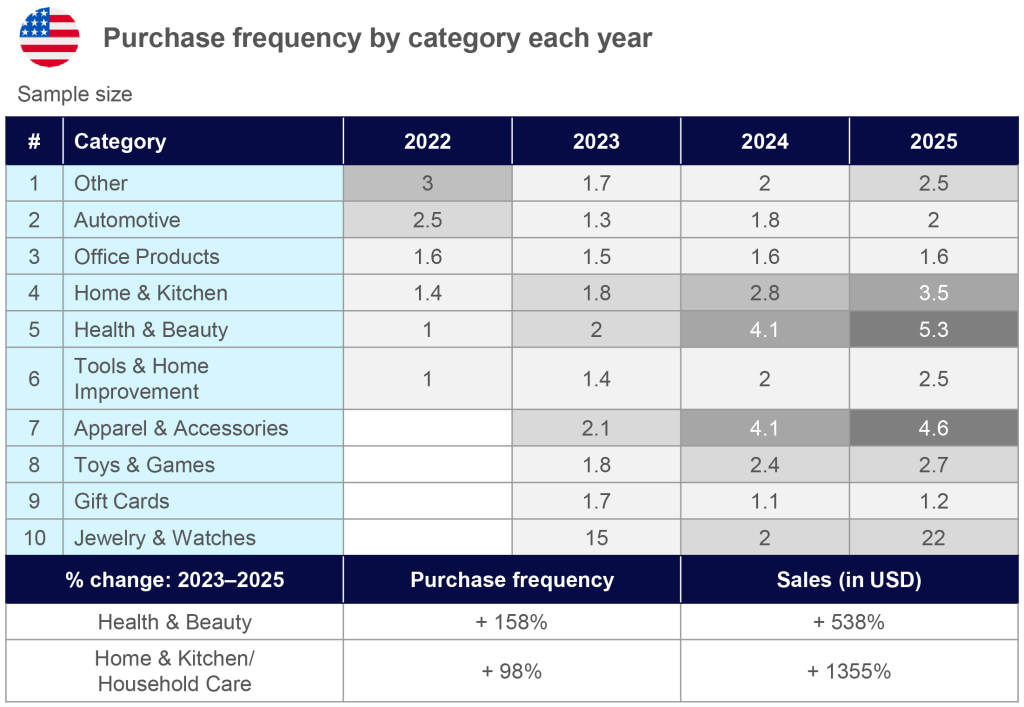

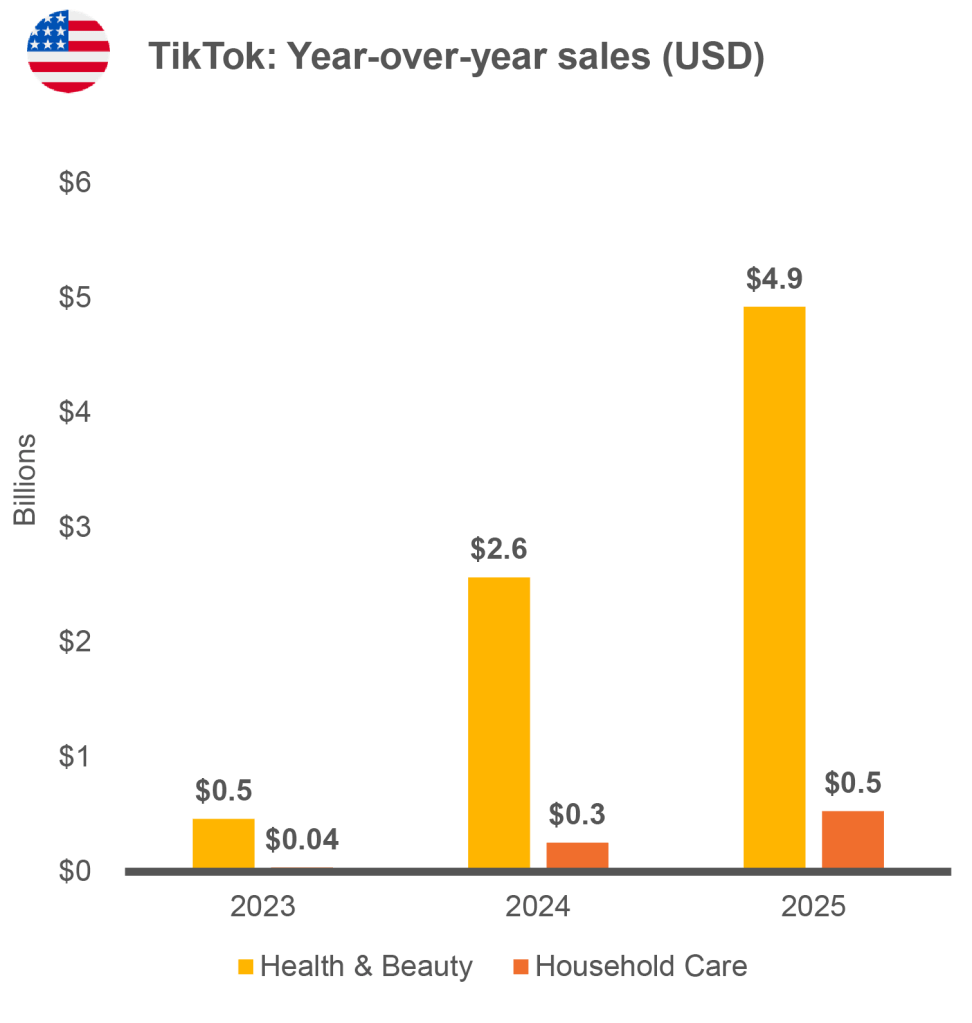

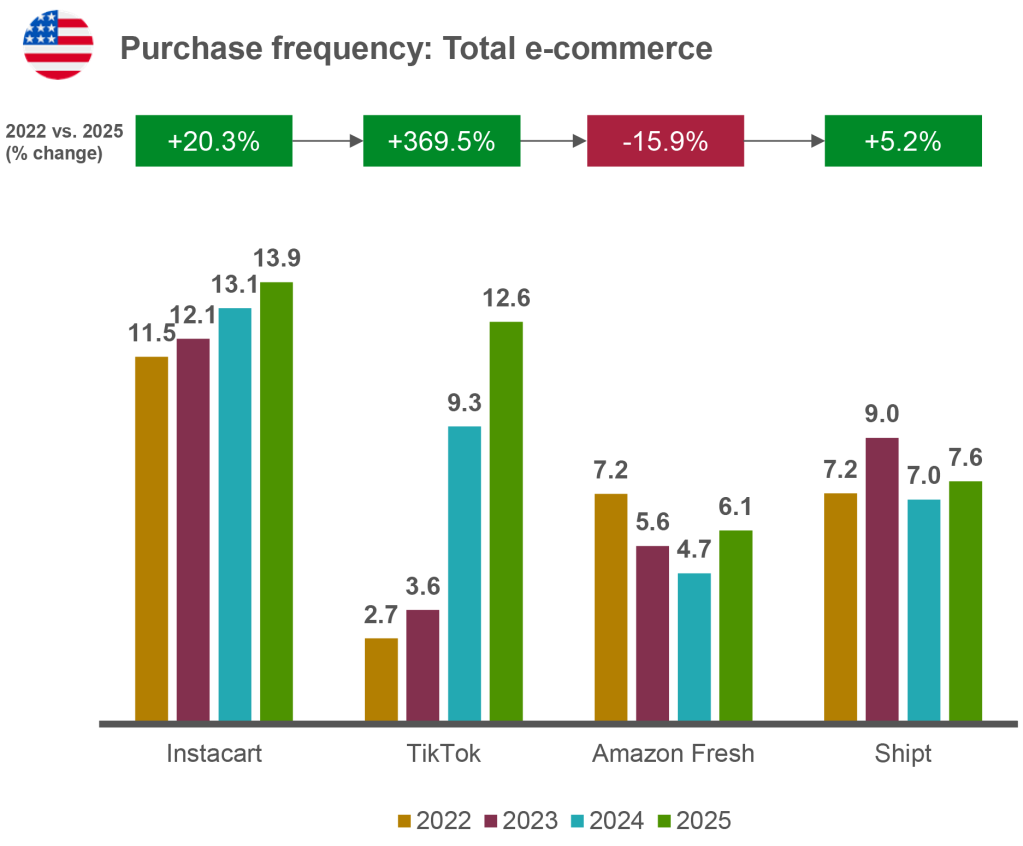

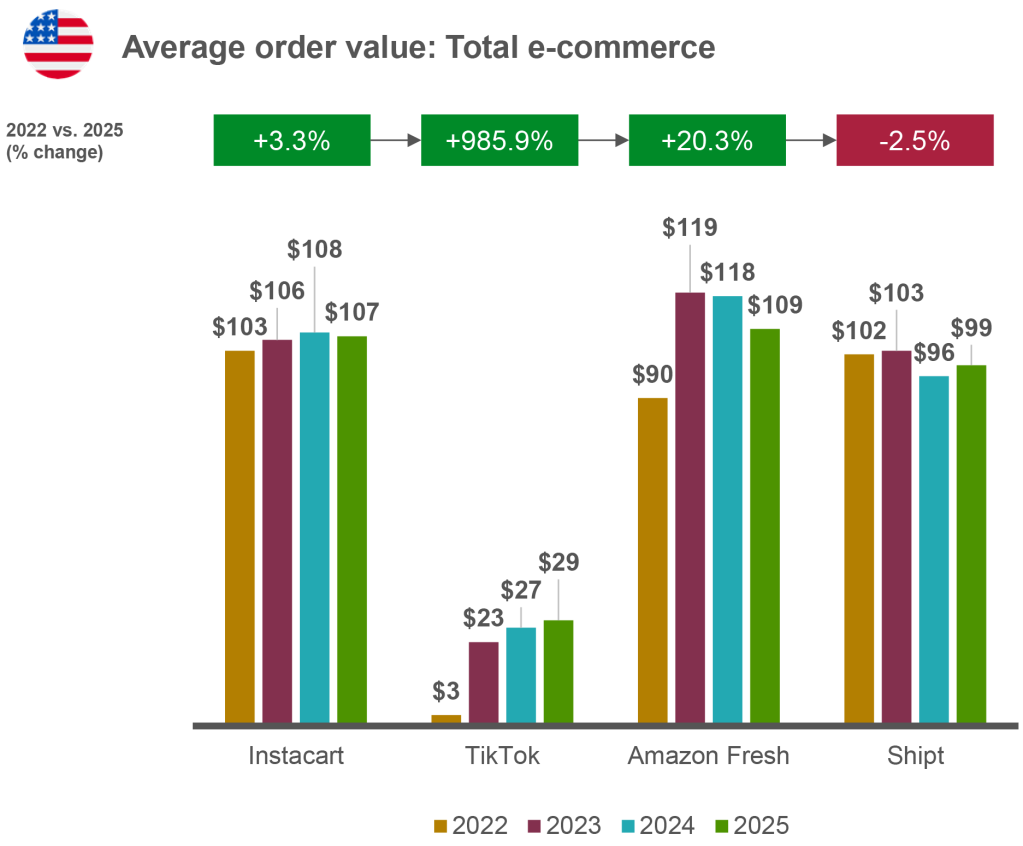

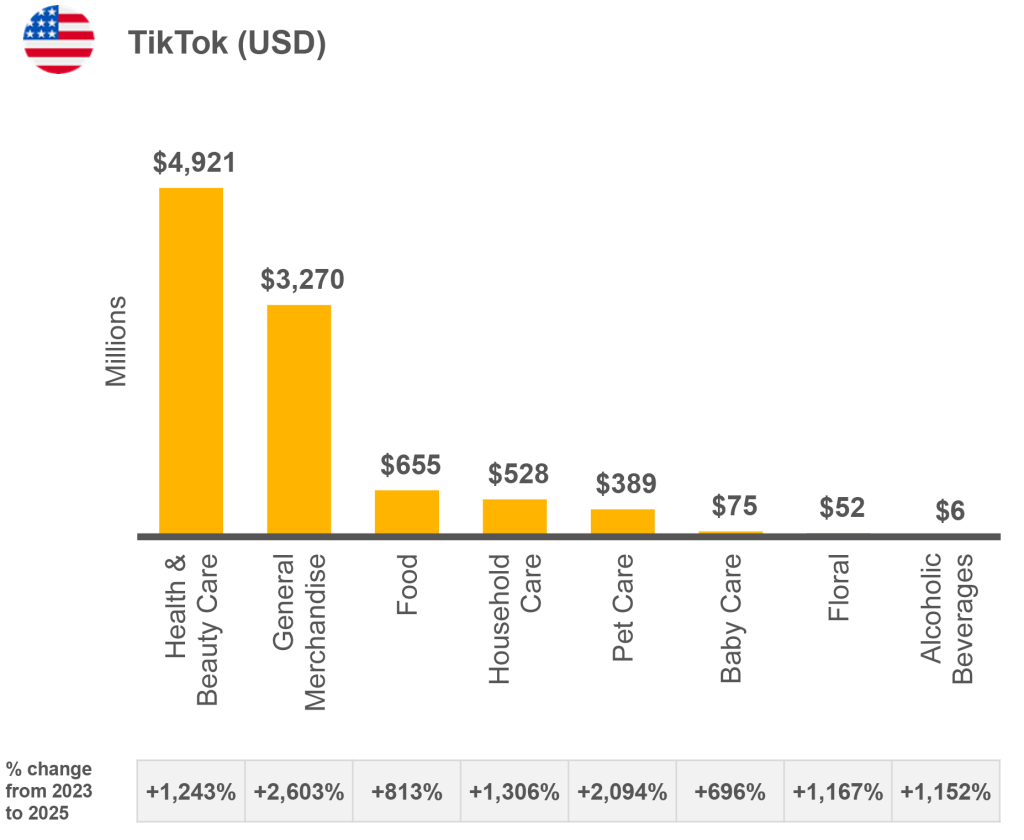

While TikTok only commands 2.3% of online FMCG, it’s the fastest-scaling driver, showing how engagement-led platforms are beginning to convert discovery into real spend in the West. Purchase frequency in the US is up 369% (when compared with 2022), with average order value (AOV) rising from approximately $3 to about $29. These changes indicate a shift from impulse buys to repeatable basket-building behaviors.

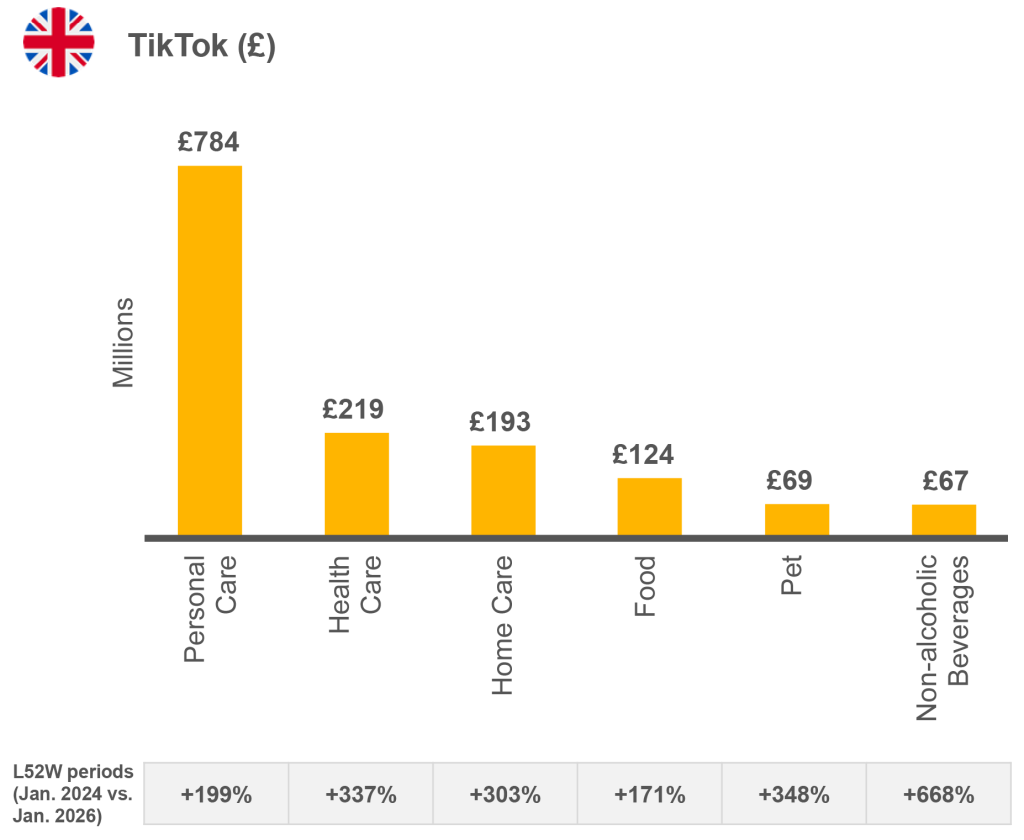

TikTok US growth is led by Health & Beauty ($4.9B) and General Merchandise ($3.3B), while the UK is scaling in Personal Care (£784M) and Health Care (+337% over the past two years).

What drives TikTok sales among US consumers

Health & Beauty attracts the most repeat buying; Household Care records the sharpest dollar sales lift among categories shown.

What’s interesting is that social commerce growth for TikTok in the UK is coming from channel or platform switching, rather than market expansion. Brands that can convert social media users to social commerce shoppers stand to unlock significant revenue.

How TikTok is gaining users in the UK e-commerce market

Note: Index shows relative customer counts vs. the starting period (baseline = 100); not absolute customer numbers.

Unsurprisingly, the young population of consumers who are active on social platforms will continue to create opportunities for brands to grow in India, and projections put social commerce growth in India at a 10.3% CAGR through 2030, potentially valuing the market at $14 billion.

Key takeaways

As social platforms continue to blend capabilities, brands have an opportunity to convert discovery-driven engagement into measurable retail outcomes. Always-on content and user-generated content (UGC) programs can seed trends, generate real-time consumer insights, and accelerate conversion within social commerce environments.

The goal for Western brands should be reducing friction between brand messaging and product discovery by integrating commerce naturally into consumers’ social media journeys.

Quick commerce (“q- commerce”)

Delivery in under one hour is the hallmark of the rapidly growing quick commerce channel, driven by rising consumer demand signals and evolving consumer spending behavior tied to immediacy and convenience. To fuel this, companies stock dark stores or ghost stores that have no physical storefront and place them in strategic locations for use as a logistics hub or warehouse. Adoption is category-specific, and carts in this space are lean, with most shoppers only purchasing one to five items at a time.

APAC again leads the way when it comes to quick commerce. Key drivers for success include limited-time deals (57%), immediate needs (56%), and impulse buying (55%). These drivers reinforce the urgency and spontaneity of fast commerce behavior. Social media—creator content specifically—also plays a key role, influencing almost 40% of all q-commerce buyers in APAC.

70%

of APAC consumers shop fast commerce at least once per month

Global ultra-fast delivery apps (quick commerce) usage varies from East to West

Q: Have you used any “quick commerce” or ultra-fast delivery apps or services that deliver groceries, household items, or electronics to your door in less than 30 minutes?

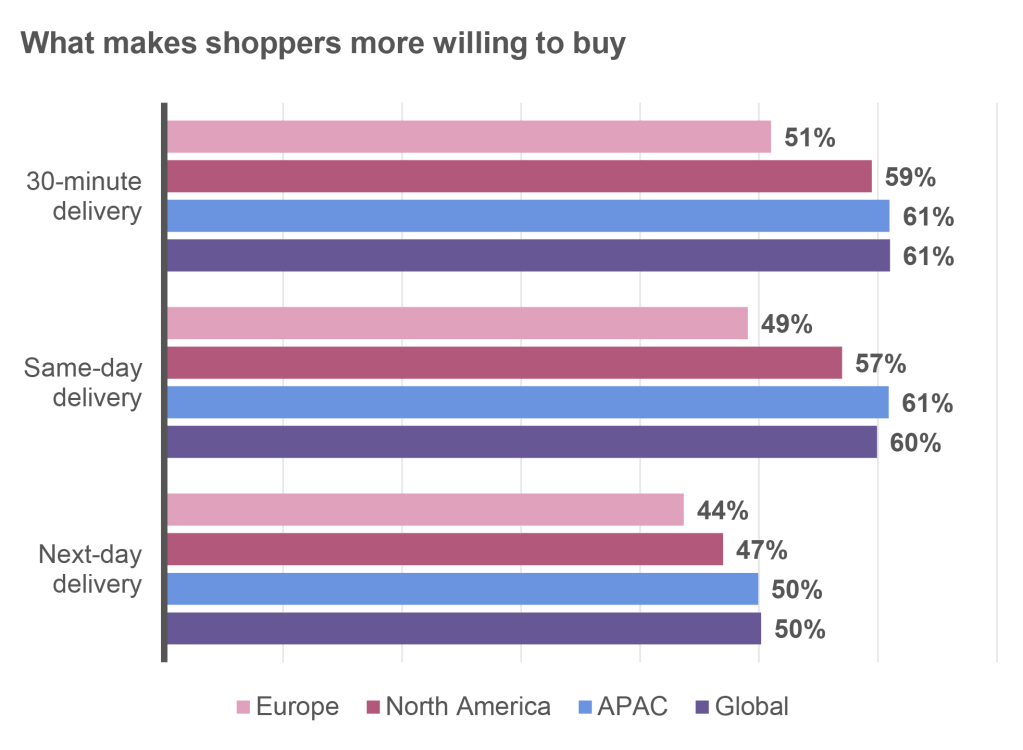

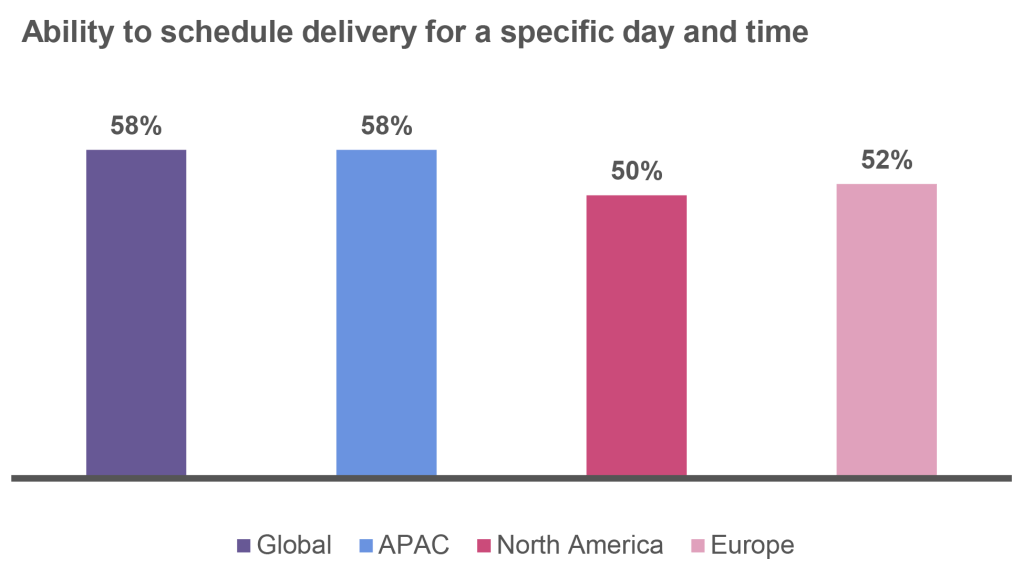

Globally, consumers view same-day and 30-minute delivery as similarly impressive, indicating that ultra-fast fulfillment isn’t a differentiator in every market. Delivery scheduling is the feature with the strongest impact on purchase intent, at 58%. This tells us that brands looking to enter the quick commerce market should focus on reliability and convenience rather than just extreme speed.

Impressive features that drive higher purchase intent

Q: When purchasing on a digital shopping platform, what are your expectations regarding delivery timing?

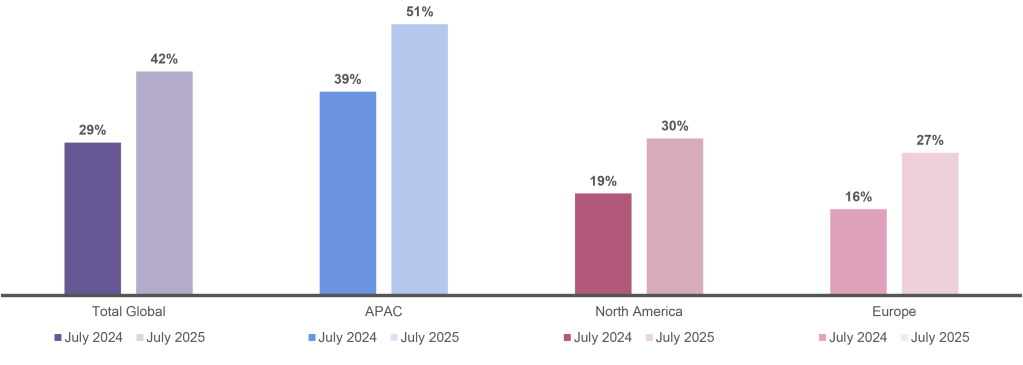

Global consumers increasingly are willing to spend more for products that can guarantee “30 minutes or less” delivery

“Super apps” are largely driving quick commerce in the East. These apps, which began delivering one service—such as payments or ridesharing—have expanded into food delivery, grocery, and other services. While they’re abundant across Southeast Asia, there are fewer players in the West due to regulatory and competitive barriers.

Market view

Quick commerce adoption is already mainstream in China, with 83% of the population making purchases through the channel. Similar to live commerce, Chinese consumers are accustomed to a busier interface, with coupons flying in and out of frame and deal-driven selling. Their willingness to pay for sub-30-minute delivery is also among the highest globally. (Six in 10 consumers in China are willing to pay more for products that will arrive in 30 minutes or less.)13 These trends are expected to push the quick commerce market valuation to over one trillion yuan this year.

The dark store warehouse infrastructure in China is unparalleled. Today, roughly 10,000 dark stores operate across the country, with a combined capacity of approximately 90,000 convenience stores—each reaching consumers within three to five kilometers. It’s expected that this number will double in the next two years, undoubtedly reshaping reshaping the broader retail landscape.

We also see a growing trend of unmanned vehicles assisting with express deliveries in China. The nation reached 199 billion parcels in 2025—an almost 14% increase over the prior year. This technology is helping expand q-commerce delivery networks for retailers in both urban and agricultural areas.

Q-commerce usage in South Korea is significantly lower than China, India, and Indonesia, at just 37% penetration. This may be because awareness of ultra-fast delivery is limited. Interestingly, South Korea’s e-commerce players are homegrown, with little to no crossover with Chinese or Japanese platforms. Many local players in the country are scaling quick commerce by combining direct inventory and third-party partnerships. In 2025, the market was valued at around $3 billion.

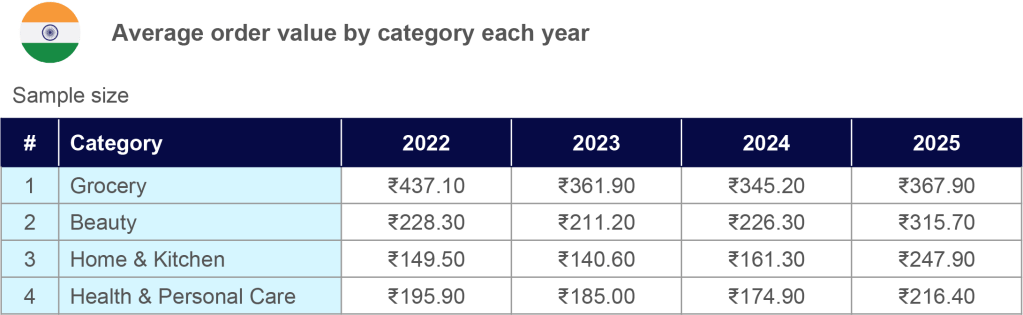

India is perhaps the biggest growth story in APAC as it relates to q-commerce. It’s already responsible for most e-commerce transactions in major cities, representing roughly 75% of e-commerce sales, with 82% of the online online shopper population using the channel. India’s dark store network has expanded significantly in recent years—and is projected to exceed 5,000 locations by year’s end. Each dark store processes as many as 1,800 transactions per day. Key players in this space include Blinkit, Instamart (née, Swiggy), and ZeptoNow, with marketplace giants Amazon and Flipkart now operating their own quick commerce arms (Amazon Now and Flipkart Minutes, respectively) as well.

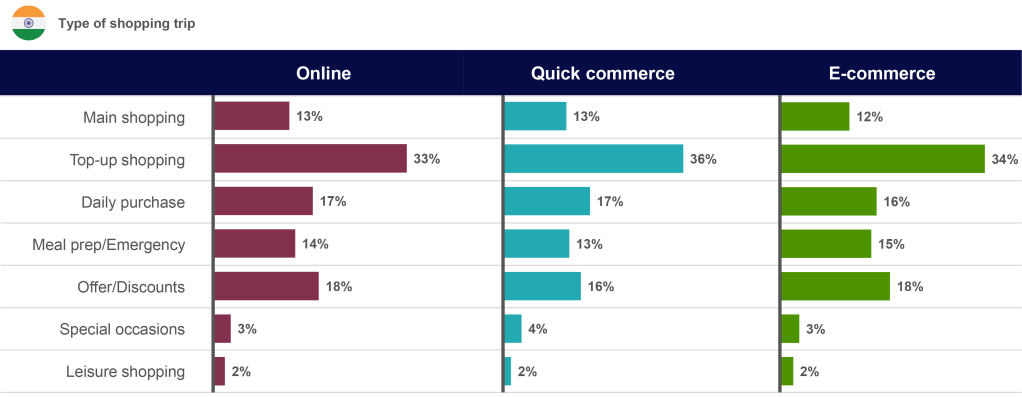

One of the biggest boosts to sales has been 10-minute delivery combined with “top-up shopping”—just-in-time replenishments of essential items like milk, bread, or fresh produce when consumers run out or on the verge of running out (as opposed to waiting for their next planned—often weekly—shopping trip).

- NIQ 2025 Consumer Outlook survey

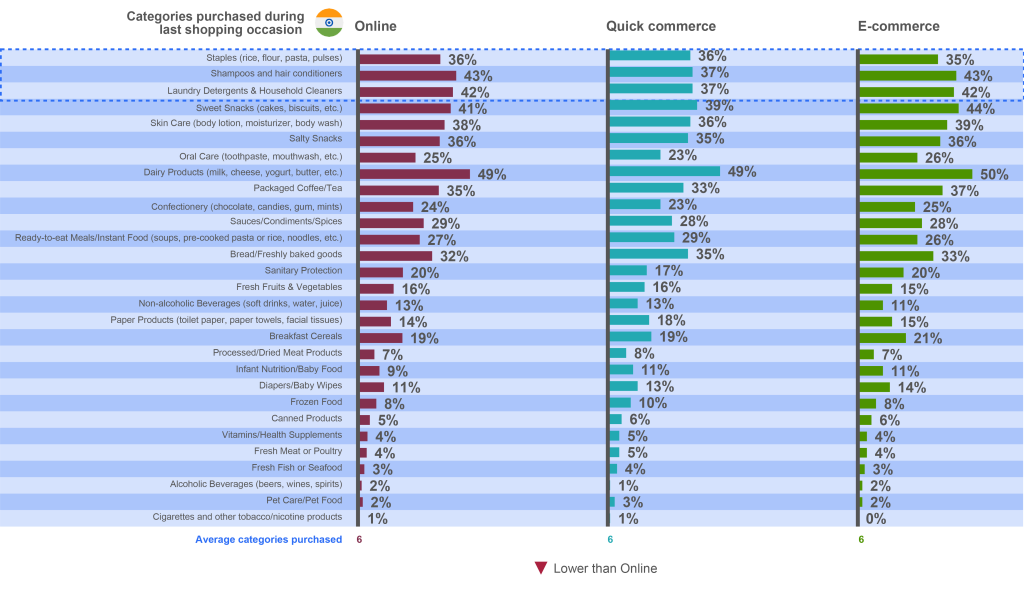

Indian shoppers turn to digital channels primarily to restock items they regularly buy (but not in bulk)—aka, “top-up shopping”

Base: Online (n=1079), Quick commerce (n=742), E-commerce (n=735)

Ref Q200: On your latest trip, which of the following best describes the type of shopping trip at a traditional trade outlet?

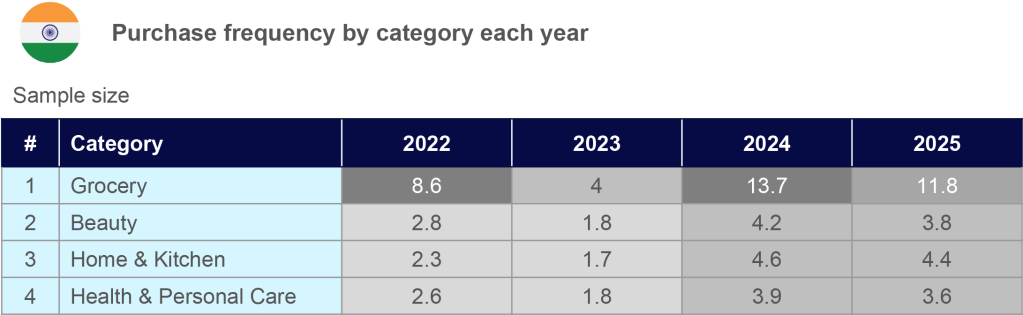

Quick commerce is also becoming a major grocery channel across India, with rising basket sizes showing it’s increasingly used for full pantry shopping, not just top-ups. As the market has matured here, consumers have also expanded from groceries to categories like Beauty and Home Care. Both categories are experiencing rising AOVs, with Beauty up 40% (vs. a year ago) and Home Care up 54% over the same period.

Increasing basket size is also a factor, as shoppers add “top-up” items to their baskets to avoid delivery fees (and stock up on items they know they’ll need later anyway).

Quick commerce (Amazon Now, Blinkit, Instamart) in India

Grocery drives the highest repeat buying in India’s quick commerce marketplace, while Beauty and Home categories show rising engagement and steadily increasing order values.

Within Grocery, Dairy (49%) and Sweet Snacks (39%) stand out as successful outlier categories in India. Growth in these categories has helped q-commerce climb to 80% of FMCG sales in the country.

Shoppers in India prefer to buy Hair Care and Home Care items via e-commerce channels

Base: 2025 – Online (n=1074), Quick commerce (n=741), E-commerce (n=731)

Ref Q142, Q161, Q8j: In which of the following categories did you buy on your latest visit to …?

It’s also notable that there are now platforms delivering smartphones and laptops in 15 to 20 minutes (or fashion in roughly 90 minutes).

India’s densely populated cities—combined with relatively low delivery labor costs—have been key to this channel’s growth. In fourth-quarter 2025, the nation’s q-commerce market grew 68% year over year.

Indonesia remains an underpenetrated but high-opportunity market for quick commerce, with 62% of consumers purchasing through the channel. The country shares many characteristics with India, including dense urban centers and a rapidly expanding e-commerce ecosystem. Jakarta, the largest city in Southeast Asia, provides particularly strong conditions for q-commerce growth.

We anticipate Indonesia will be one of the next major markets for quick commerce as e-commerce adoption continues to expand across the region.

Key takeaways

Quick commerce represents the convergence of proximity-driven logistics, retail infrastructure, and lifestyle-driven consumption. Brands that design products and promotions around specific consumption occasions—while leveraging localized logistics hubs—will be best positioned to succeed in this rapidly evolving channel.

Migration West

The early quick commerce boom in the West has sharply corrected, revealing fundamental weaknesses in the initial operational model. Several US players exited after heavy losses, with the remaining operators (e.g., DoorDash, Gopuff, and Instacart) shifting to more durable strategies—namely longer delivery windows, deeper retail partnerships, and an increased reliance on advertising revenue. Meanwhile, major retailers like Amazon and Walmart continue to invest in q-commerce in both major cities and less densely populated areas.

Western markets generally show low awareness and adoption of quick commerce brands. When surveyed, between 19% and 47% of consumers said they weren’t familiar with at least some (if not all) of them. Despite these headwinds, quick commerce in the US experienced 62.2% growth in 2025.

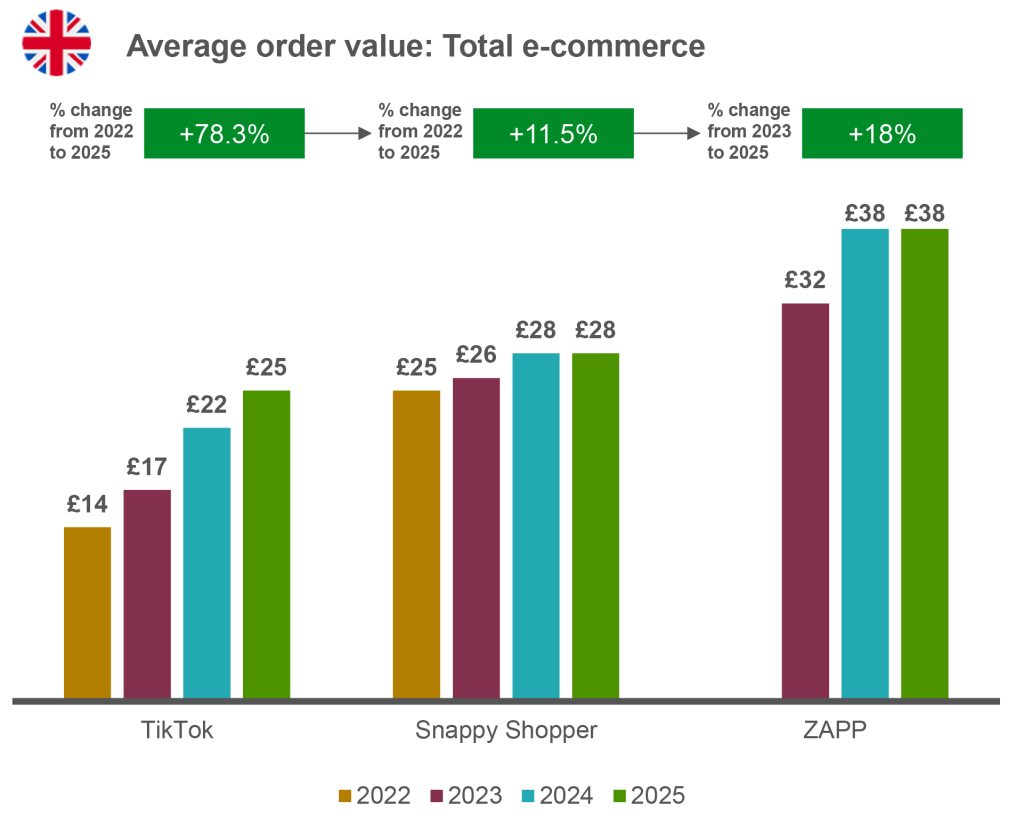

TikTok leads in purchase frequency and spend growth (USD)

TikTok is the fastest‑growing US e‑commerce merchant in both how often people buy and how much they spend—reshaping digital shopping behavior. Quick commerce platforms are also growing but at a comparatively slower pace.

While consumers in the East are often promotion-focused, Western consumers are won on convenience—but the higher platform and delivery fees are certainly impacting adoption. There’s also the reality that in the US and other Western countries, the population is highly dispersed. Without as many densely populated cities, warehousing and delivery routes for quick commerce retailers become more challenging. Indeed, retention is what sustains platforms in this region. In the US, for example, 54% of q-commerce users are repeat shoppers.

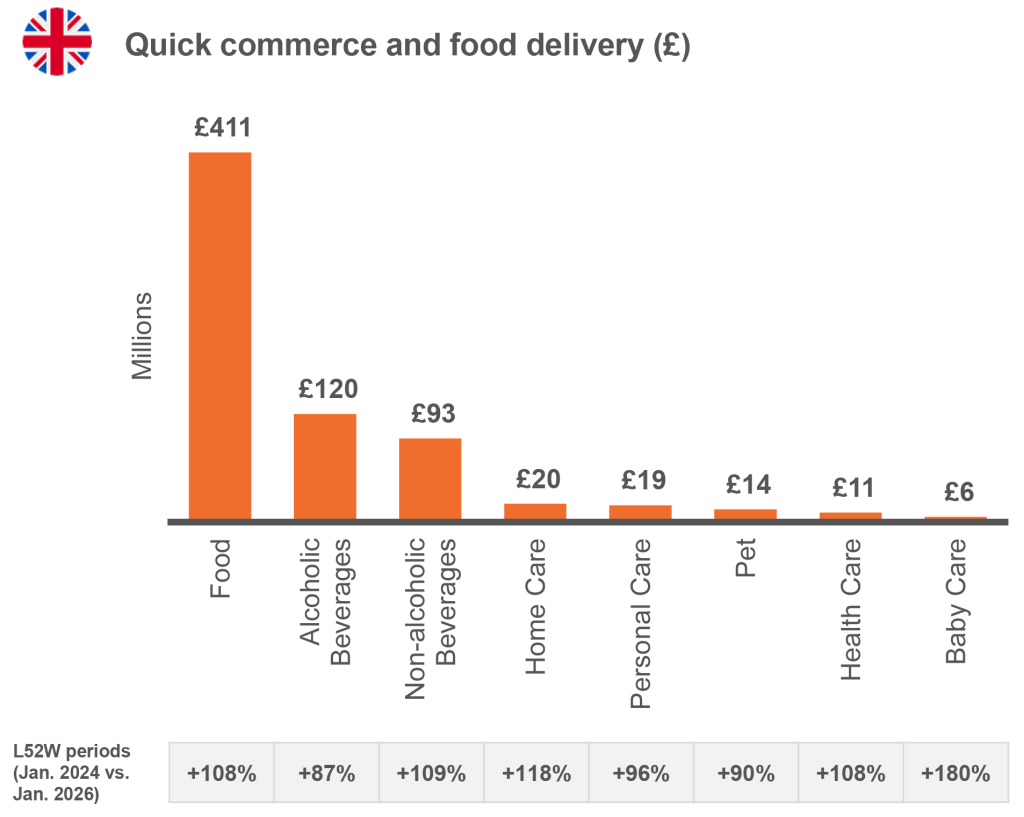

As we saw in the East, quick commerce is anchored to Food category, accounting for nearly $22 billion in US sales and £411 million in the UK. Alcohol and Non-alcoholic Beverages are also experiencing positive momentum in the UK, reinforcing the channel’s role in immediacy-driven and replenishment occasions.

Non-food categories driving surge in TikTok growth in the US; Food dominates quick commerce usage in the US

Non-food categories driving steady growth in TikTok usage in the UK; Food dominates quick commerce usage in the UK

Quick commerce expansion remains limited across the UK, with growth largely driven by channel or platform switching (63%). Secondary gains are coming from rising AOVs and increased repeat purchase frequency.

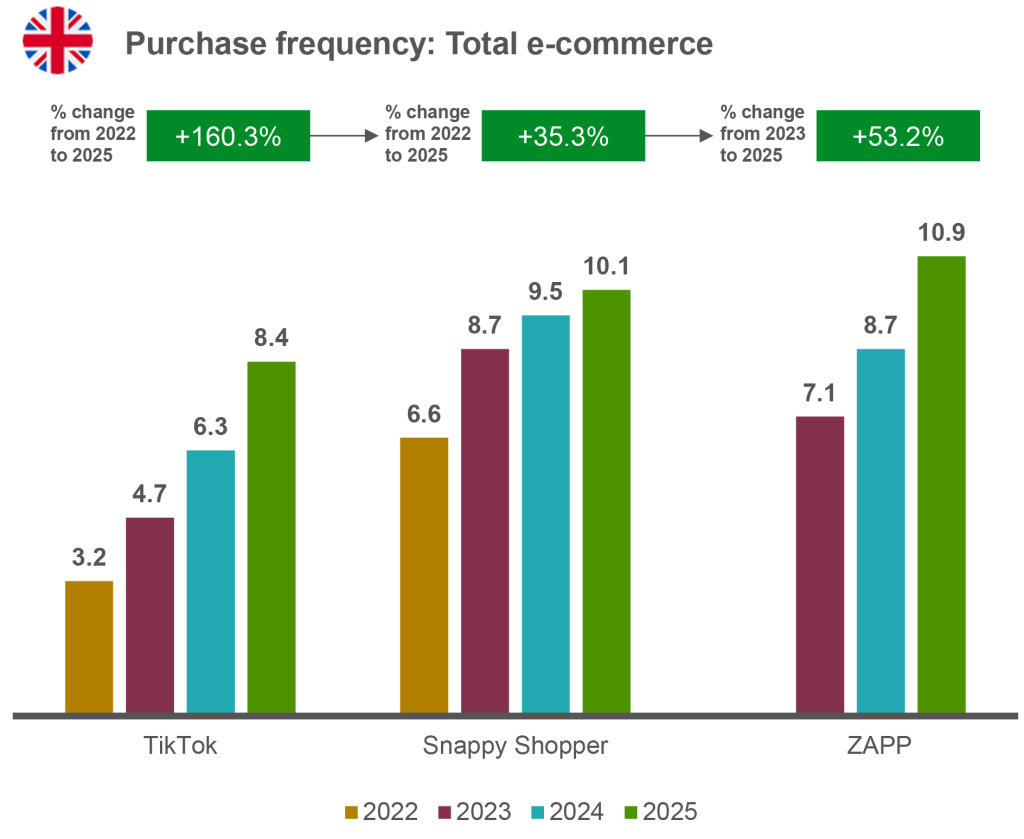

Frequency drives growth in social commerce; value follows in quick commerce in the UK

Social commerce (TikTok) is exploding through discovery-led frequency, while quick commerce is maturing by combining high repeat usage with rising basket values.

Additional challenges for quick commerce brands in the UK include limited assortment depth and higher out-of-stock volatility. Where traditional grocers carry approximately 50,000 stock-keeping units (SKUs), dark stores in the UK typically average just 2,000 SKUs.

Indeed, q-commerce is struggling to gain a foothold across Europe. In France, quick commerce accounts for roughly 0.2% of FMCG e-commerce value, underscoring how marginal ultra-fast delivery remains in the French FMCG landscape. In fact, NIQ’s data reveal that many q-commerce categories in France are shrinking sharply, with Food down 74% and Non-alcoholic Beverages down 79%, for example.

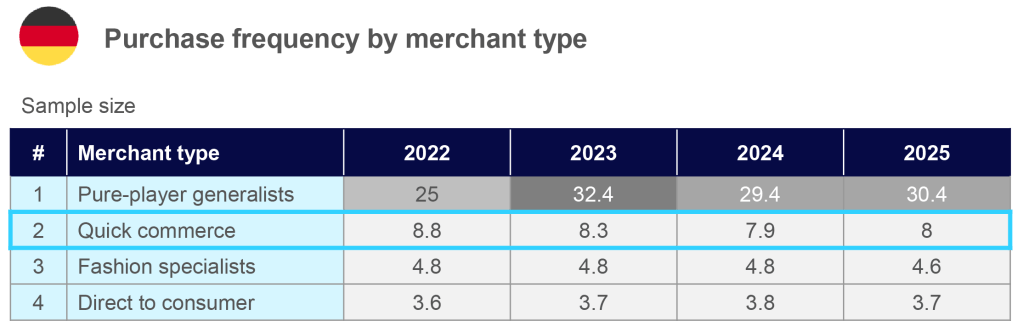

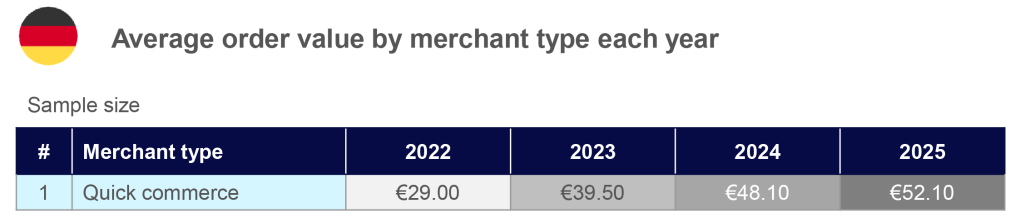

Germany, meanwhile, is seeing basket growth rather than increased shopping occasions. Outlier categories driving growth include Home Care (+15% vs. two years ago), Pet Care (+65% vs. two years ago), and Food (+3% vs. two years ago). Even with this growth, the market accounted for less than 6% of total e-commerce revenue in 2025.

Stable quick commerce frequency, rising order values in Germany

Italy stands out in Southern Europe as a momentum market, contrasting France’s stagnation despite similar regional context. Quick commerce is small but accelerating across all tracked categories, signaling early-stage adoption rather than saturation. Food (+115% vs. two years ago) and Non-alcoholic Beverages (+136% vs. two years ago) lead growth, highlighting immediacy-driven consumption moments. moments. Alcohol (+91% vs. two years ago) and Personal Care (+45% vs. two years ago) show additional traction, suggesting early diversification beyond food delivery.

Though in its infancy in the West, quick commerce is beginning to integrate content-driven formats. Gopuff represents the clearest example of a quick commerce platform blurring the lines between inspiration and purchase. For example, the launch of their recipe hub fuels product discovery (for an entire basket of goods) and promises delivery in under 15 minutes.

Key takeaways

While quick commerce scaled rapidly in APAC from concentrated infastructure and super-app ecosystems, Western markets are still searching for more sustainable operating models. Growth is largely driven by shopper retention, increasing basket sizes, and expansion into higher-margin categories rather than new user adoption.

Platforms that can successfully balance convenience, consumer utility, and logistical hurdles will be best positioned to profit from quick commerce.

What’s happening in the West

When examining total spend, Western consumers stlll gravitate toward traditional e-commerce and in-store shopping. However, significant growth is occurring in evolving channels. Consequently, manufacturers and retailers looking for growth opportunities can no longer afford to ignore these new commerce models.

The winning strategy: a true omnichannel approach that pairs legacy and evolving channels with first-party data—enabling deeper consumer insights and a more complete understanding of retail consumer behavior.

New commerce models are outpacing traditional online growth in the US

Retail media networks

The retail media sector has grown around 23% per year globally since 2020, and there are now more than 270 active RMNs. The advantage for brands is clear: move beyond awareness to conversion when consumers are in a shopping mindset.

In the West, RMNs are often viewed by brands as a cost of doing business. They invest to get premium real estate, create better relationships with retailers, and gain access to retailers’ troves of first-party data. For the retailer, RMNs provide a highly profitable monetization mechanism. Qustions still abound, however, about the true value of these investments to brands, how sustainable the investments are in the mid- and long term, and how to maximize efficiency across competing platforms.

$184 billion

Retail media global spend in 2025

Source: Global Media Retail Forecast, 2025 to 2030 (Forrester, Oct. 9, 2025)

Market view

US retail media ad spend is estimated to reach $107.6 billion in 2026, nearly tripling over the past five years. This growth reinforces that RMNs are playing an even bigger role in the media mix for marketers.

On average, brands in the US will work with eight RMNs this year. Performance measurement is a challenge, however. Almost half of brands say their measurements are only somewhat effective or not effective at all. Incrementality and cross-channel measurement top their list of measurement pain points.

As agentic commerce continues to evolve, this challenge becomes more acute and critical. AI agents shape consumers’ discovery and transaction—directly influencing not only what they see but what they ultimately purchase. This, in turn, requires legacy methods of targeting, optimization, and measurement to adapt to account for agent-driven interactions—both on retail media networks and within large language models (LLMs)—driving consumers off platform to purchase on RMNs.

In-store retail media spend is also growing as retailers like Walmart, Kroger, Sephora, The Home Depot, Sam’s Club, and others look to monetize as much of the store as possible. From “buy it again” ads on RMNs to in-store electronic shelf tags and TV screens, advertisers have more options than ever to capture—and convert—shopper attention.

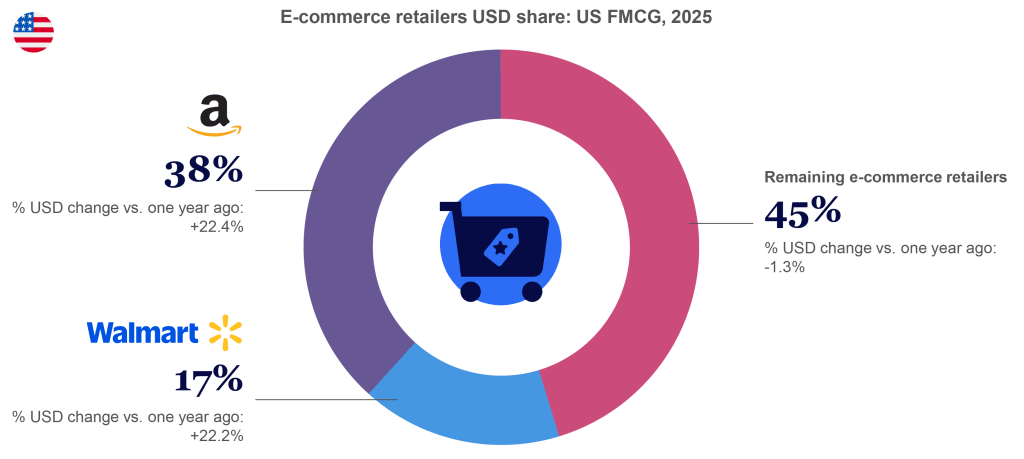

Amazon and Walmart are e-commerce leaders in the US

Amazon and Walmart together capture over half of the $432B US online retail (fast-moving consumer goods) market, reinforcing the growing dominance of large marketplace platforms.

Retail media leaders in the US are also beginning to apply AI more broadly to help with campaign measurement, optimization, and analytics. The hope is this will continue to drive hyper-personalized experiences for consumers. However, a lack of technical expertise and concerns about reliability are keeping some brands from deploying it on a national scale.

In the UK, the total retail media spend is projected to be £4.8 billion this year. More share of advertising budgets is going to retail media, and it’s one of the most crowded RMN markets—with more than 28 active networks.

Cross-channel and platform targeting is currently limited in the UK and Europe due to privacy regulations. An obvious way to overcome these challenges is by further leveraging super apps in the East, creating a self-contained, multi-benefit environment for consumers—and a data-rich environment for brands and retailers.

Meanwhile, Mexico’s RMN market is growing at a CAGR of almost 10%—though it’s nowhere near the penetration in the US or UK. To the North, Canada’s ad spend is expected to increase fivefold between 2020 and 2029, reaching almost $3 billion.

One new trend in the West is RMNs expanding outside of the retail brand space. Their first-party data is attracting non-endemic placements for insurance, travel, banking, and more. Several large retailers, including Walmart, are rapidly monetizing this model. RMNs that can also connect brands to consumers off-site should also anticipate substantial revenue growth, with off-site media spend anticipated to grow two to three times faster than on-site media.

Key takeaways

The West currently leads in retail media monetization, but sustained growth will depend on greater transparency, stronger measurement, and clearer proof of incrementality for brands. As privacy regulations limit cross-platform targeting, the super-app ecosystems born in the East may provide a blueprint for the future—integrating commerce, media, and consumer data within unified platforms that create more measurable and privacy-compliant advertising environments.

Migration East

The retail media landscape in the East is growing but fragmented. There are many large retailers across APAC, yet there are no big customer relationship management (CRM) platforms comparable to those supporting RMNs in Western markets.

RMNs in the region are also more about content, engagement, and consumer participation than direct ad buys and exact measurement of ad dollars. As retailers look for opportunities to diversify revenue, in-store retail media is scaling quickly. Some retailers are now building programmable retail environments that link point of sale (POS), loyalty programs, signage, and sensors with their content management systems (CMS), giving them real-time sales attribution and SKU-level performance.

In China, retail media winners include super apps like Alibaba, Douyin, JD.com, Meituan, and Tencent. These apps have more advanced personalization than RMNs in the West and use deep user profiles, plus product graphs coupled with AI, to capture intent and stimulate latent demand. This allows them to feature promotions and ads that change every few seconds and follow users throughout the entire experience.

Offline retailers in China remain fragmented, hold relatively small market shares, and have built weaker tech stacks by comparison.

South Korea currently has the highest share of FMCG online penetration globally, at 42%.14 This deep e-commerce penetration, led by Coupang and Naver, makes the market ripe for retail media innovation. Just a few years ago, retail media accounted for 1% of total online sales revenue in South Korea. By 2028, it’s expected to have grown over 40%, to $178 billion. AI-powered recommendation systems and robust first-party data are helping drive this new profit center for retailers.

In India, meanwhile, quick commerce platforms are prime real estate for retail media. They have an active and engaged user base that’s delivering higher return on ad spend (ROAS) than channels like social media. Campaigns are now shifting toward anticipatory targeting using AI prediction models, and RMN intelligence is scaling through integration with CRMs and other measurement tools. This market should see a CAGR of 10% through 2030.

- NIQ Market Intelligence

Key takeaways

Retail media in the East is evolving inside powerful super-app ecosystems, where commerce, content, and consumer data are already deeply integrated. While these platforms lead in personalization and engagement, Western RMNs offer important lessons in measurement transparency, advertiser accountability, and scalable monetization.

For retailers across APAC, the opportunity lies in strengthening data infrastructure and attribution capabilities while leveraging the integrated ecosystems that already shape consumer behavior.

What’s emerging globally: Agentic commerce

While the channels examined in this report (live, social, and quick commerce and retail media) represent the current architecture of global commerce, a new force is rapidly reshaping all of them simultaneously. Agentic commerce, in which AI agents autonomously discover, compare, and purchase products on behalf of consumers, is collapsing the traditional purchase funnel across every channel and region.

Unlike the other shifts examined here, agentic commerce didn’t originate in one region and migrate to the other: It’s emerging in both the East and the West at the same time, built on different infrastructure, and scaling at very different speeds.

The infrastructure in the West: open protocols and platform competition

In the West, agentic commerce is being built through competing open standards backed by the largest technology platforms. Perplexity announced its PayPal partnership in May 2025 and launched its free agentic shopping product with PayPal-powered Instant Buy for US consumers in November 2025, connecting users to merchants including Abercrombie & Fitch, Fabletics, and Newegg. OpenAI and Stripe launched the Agentic Commerce Protocol (ACP) in September 2025, enabling checkout directly within ChatGPT conversations.

Etsy was the first live integration, with over one million Shopify merchants (including Glossier, SKIMS, and Vuori) and PayPal following in subsequent months. Google then announced the Universal Commerce Protocol (UCP)—co-developed with Shopify, Walmart, Target, and Wayfair and endorsed by more than 20 global partners, including Visa, Mastercard, and American Express—at the National Retail Federation conference in January 2026. Most large merchants will ultimately need to support multiple protocols to remain visible to AI-driven shoppers.

The commercial velocity has been striking. OpenAI’s ChatGPT advertising pilot surpassed $100 million in annualized revenue in roughly six weeks after launch, with more than 600 advertisers participating, while ads were shown to fewer than 20% of eligible users on a daily basis. The company projects $2.5 billion in ad revenue for 2026. AI-sourced traffic to US retail websites surged 1,200% year over year, and AI-referred shoppers converted 31% more than those arriving from other sources, according to Adobe. Morgan Stanley estimates that agentic shoppers could represent $190 billion to $385 billion in US e-commerce spending by 2030, capturing 10% to 20% of total online retail. McKinsey projects the global opportunity at $3 trillion to $5 trillion over the same period.

Despite this momentum, the Western ecosystem remains fragmented. Protocols compete with one another, each platform handles checkout differently, and the measurement infrastructure to track agent-driven conversions doesn’t exist at scale—yet. Amazon, which controls approximately 38% of US online FMCG, hasn’t joined either ACP or UCP—and is building proprietary AI shopping agents (Rufus, Alexa+, Buy for Me) within its closed ecosystem, further fragmenting the landscape.

The infrastructure in the East: super apps at scale

China is already operating agentic commerce at production scale, enabled by the integrated super-app ecosystems that have no equivalent in the West. Alipay’s AI Pay solution processed more than 120 million agent-driven transactions in a single week in February 2026. Alibaba’s Qwen chatbot reached 100 million monthly active users within two months of launch. Users can now compare products on Taobao, book flights on Fliggy, and pay via Alipay—all without leaving the conversation. ByteDance has integrated agentic capabilities into Doubao and is developing AI-enabled smartphones with ZTE. Tencent is embedding similar functionality into WeChat. Industry analysts estimate Chinese tech companies are spending approximately $42 million per month on AI shopping tools as they race to establish consumer habits.

The structural advantage in the East is clear: Because commerce, payments, content, and logistics are vertically integrated within platform ecosystems, the interoperability challenge that Western companies face with competing protocols simply doesn’t exist. AI agents in China can execute end-to-end transactions across categories because the underlying infrastructure was built for exactly this type of vertical integration. Analysts have compared this moment to the battle for mobile payment dominance between WeChat Pay and Alipay over a decade ago, which created the infrastructure that now makes agentic commerce possible.

Why this changes the game for manufacturers and retailers

Agentic commerce is distinct from every other channel examined in this report because it changes who is making the purchase decision. In live commerce, social commerce, and quick commerce, consumers remain the primary decision-makers, guided by content, creators, and convenience. In agentic commerce, the AI agent becomes the decision-maker, evaluating structured product data, real-time pricing, inventory availability, and reviews on the consumer’s behalf—often across multiple retailers simultaneously.

This has immediate consequences for how brands compete. Legacy methods of targeting, attribution, and incrementality measurement were designed for human-driven browsing behavior—they don’t account for agent-driven interactions. When an AI agent recommends a product, the traditional funnel (impression to click to cart to checkout) collapses. Brands that invest now in structured product data, AI-readable attributes, and cross-platform measurement infrastructure will be positioned to capture share. Those who wait risk becoming invisible to the agents that will increasingly determine what consumers buy.

For both manufacturers and retailers, the question is no longer whether AI will reshape commerce—it already is. The question is whether their data, systems, and measurement capabilities are ready to compete in a world where the human shopper may never visit their website, open their app, or see their ad.

Key takeaways

- Agentic commerce is emerging globally, with the East scaling faster due to unified super-app infrastructure and the West building through competing open protocols.

- Perplexity/PayPal (announced May 2025, live November 2025), OpenAI/Stripe (ACP, September 2025), and Google (UCP, January 2026) all moved to formalize agentic shopping capabilities within an eight-month window, signaling rapid platform convergence around this model.

- China’s super-app ecosystems are already processing agentic transactions at scale (120 million in a single week), while Western platforms are still onboarding merchants and refining checkout infrastructure.

- The shift from human-driven browsing to agent-driven purchasing requires new approaches to product data, measurement, and attribution that don’t yet exist in most organizations.

- Brands that build agent readiness now, including structured product data, real-time inventory signals, and AI-optimized attributes, will capture disproportionate share as adoption accelerates.

AI-powered agentic commerce is rewriting the rules of growth at extraordinary speed.

Discover how to get—and stay—ahead in The New Growth Frontier: How agentic commerce and AI tilt the scales toward challenger brands.

Why it all matters

The marriage of Eastern platform ecosystems and Western monetization infrastructure is not only reshaping commerce—it’s redefining how growth is created, captured, and sustained. What we see emerging is a blended consumer landscape where formats from one region operate on the monetization rails of the other.

For manufacturers and retailers, this signals a significant shift from managing channels to orchestrating systems—where success depends on the ability to connect data, media, and commerce into a single, continuously optimizing engine.

As emerging digital channels continue to redefine online growth, global retail is moving toward a more integrated omnichannel ecosystem—with less distinction between digital channels and in-store retail environments and the continued eradication of silos in which consumers previously engaged.

In the East, AI is fueling this shift by enhancing discovery, content generation, and real-time optimization—advancing integrated, discovery-led commerce models. Meanwhile, AI is leveraged in the West to advance pricing, supply chain, targeting, and measurement capabilities.

Together, these models are giving rise to a new, channel-agnostic commerce system where AI-driven systems increasingly inform—and in many cases execute—purchase decisions for consumers while helping to automate core business functions.

Imagine a world where real-time, personalized, content-first retail experiences collide with five-minute delivery, programmatic SKU-level advertising, and closed-loop audience measurement that proves value and drives repeat purchase and loyalty. This is the East Meets West reality that’s emerging in the near term.

At the center of this new system is an intelligence layer fueled by connected, continuously updating data—defined as commerce intelligence, where the depth, breadth, and granularity of that data become an integral source of brands’ and retailers’ competitive edge.

These changes create new opportunity—and new complexity—for global brands. Consumers now have more ways than ever to interact with products, and retailers and manufacturers that want to stay at the center must operate more like technology, data, and media companies. Content creation paired with strong data and measurement capabilities will separate the brands that lead from those that fall behind.

Those that can turn data into commerce intelligence will define the next era of global commerce.

Retailer and market case studies: Convergence at work

Retailer case study

Inside Joybuy, JD.com’s international expansion from East to West

JD.com is China’s largest retailer by revenue, with more than two decades of experience in the e-commerce space. As global commerce models continue to converge, JD.com is emerging as a clear example of how Eastern platform capabilities can move West—not through replication, but through deliberate localization.

According to Jack Li, CEO of JD Worldwide, JD.com’s international expansion is a long-term strategy rooted in the technology and services company’s e-commerce infrastructure, logistics, and end-to-end supply chain management prowess. Rather than directly replicating the model built in China, JD.com selectively applies its capabilities—exporting technology-driven strengths such as systems, supply chain, and automation across markets, while tailoring its product selection, logistics operations, and compliance protocols to align with local consumer expectations, regulatory requirements, and market conditions.

This approach is now live across Europe with the March 2026 launch of its online retail arm, Joybuy, in six markets: the UK, Germany, the Netherlands, France, Belgium, and Luxembourg. By adopting a localized e-commerce model—encompassing local teams, logistics, sourcing, partners, and delivery—and supported by a compliance-first infrastructure, Joybuy caters to a region defined by diverse markets, strict regulation, and varied consumer expectations. “For JD.com, compliance is the necessary foundation,” Li says. “We seek to compete in a transparent and regulated market where our focus can truly distinguish us from the rest.”

Don’t just buy, Joybuy: “Win at shopping”

Fast delivery is a central pillar of Joybuy’s European strategy. Drawing on proven models from China, JD.com has built a self-operated logistics network in Europe, enabling end-to-end control from procurement to fulfillment. Today, JINGDONG Logistics operates more than 60 warehouses and delivery depots supporting Joybuy across the region.

An example of these improvements can be found in UK–based smart warehouses in Milton Keynes and Luton, where a goods‑to‑person automation model has delivered an approximately four-fold increase in picking and outbound efficiency.

While these operational gains improve efficiency behind the scenes, JD.com’s focus in Europe has been translating supply-chain performance into a fulfillment experience that better aligns with local consumer expectations. Joybuy’s own courier service, JoyExpress, now operates in more than 30 major European cities, helping address longstanding consumer trade‑offs between price, delivery speed, and reliability.

By introducing delivery standards modeled on JD.com’s “211” (aka “Double 11”) service—where orders placed before 11 am are delivered before 11 pm, and orders placed before 11 pm arrive the next day—JD.com is responding to unmet expectations around convenience and certainty in European e-commerce. The focus is less on speed alone, and more on providing predictable, high-quality service in markets where consumers have historically had to compromise.

Joybuy illustrates how Eastern commerce capabilities—when executed at the local level—can translate system-driven advantages into scalable growth across global markets.

Market case study

How India is building the world’s most connected commerce ecosystem

India is a present-day example of the convergence of Eastern-style commerce with Western-style data ecosystems.

The country has a young population of tech-savvy consumers driving strong conversion across live commerce, social commerce, and quick commerce. Brands are seeing conversion rates of up to 10%–15% for live commerce, compared with 2%–5% for traditional e-commerce, while buyers in densely populated cities use q-commerce so ubiquitously that it now accounts for most e-commerce sales in those markets.

When India’s technological innovation and commerce platforms combine with a growing ecosystem of RMNs, marketwide closed-loop attribution becomes possible. We are already seeing this emerge through major platforms such as Amazon India, Flipkart, and Reliance Retail’s JioMart, alongside the country’s unified payments interface (UPI), which handles roughly 85% of digital transactions. This consolidiated consumer data environment is expected to more than double India’s retail media market—from $1.5 billion in 2024 to $3.5 billion by 2030.

As digital commerce continues to expand, brands are increasingly viewing the platforms on which they operate as components of a single ecosystem. This enables deeper customer journey insights and unlocks new opportunities for targeting, personalization, and measurement. The result: a rapidly evolving omnichannel commerce landscape where physical and digital retail increasingly operate as one connected system.

India represents “channel” convergence in action—where format-led discovery, payments infrastructure, and retail media combine into a unified, measurable commerce system.

What’s next: Key takeaways for manufacturers and retailers

As commerce shifts from channels to systems, manufacturers and retailers must rethink how growth is orchestrated, measured, and scaled.

Keep the following in mind as you navigate today’s rapidly transforming global commerce landscape:

- Global commerce is evolving into a unified ecosystem. Eastern innovations in discovery-driven platforms and Western investments in data monetization and measurement capabilities are quickly merging, creating a new model where content, data, commerce, and fulfillment function as a single system.

- Growth will come from orchestration, not channel expansion. Live, social, and quick commerce are no longer standalone channels; they’re interconnected “arms” of a broad infrastructure where discovery, transaction, and product delivery converge—requiring a truly holistic view of performance.

- Discovery—rapidly shifting toward agent-driven decisioning—will drive demand. The shift from consumers shopping via search to content- and AI-powered discovery is accelerating, forcing manufacturers and retailers to rethink how they’re measuring influence—and how they’ll connect engagement to conversion.

- Measurement will determine mid- and long-term winners. As retail media continues to evolve and scale globally, brands will continue to demand increased transparency relative to incrementality and attribution, likely shifting dollars toward retailers that can clearly demonstrate the impact of brand investments.

- The future belongs to retailers who invest in deep integration. To gain a competitive edge globally, retailers must bring their data. media capabilities, logistics, and customer engagement into a cohesive infrastructure. Doing so gives brands the ability to reach, optimize, and measure performance across the entire journey.

Why NIQ?

NIQ is uniquely positioned to measure and understand the convergence of evolving commerce formats and channels—and the systems that connect them. As live, social, and quick commerce intersect with retail media and AI-driven consumer journeys, brands must be able to quantify incrementality, understand how channels interact and diverge, and connect consumer behavior across the ecosystem—from discovery to purchase.

As agentic commerce accelerates this convergence, the need for trusted, independent commerce intelligence becomes even more critical. AI agents making purchase decisions on behalf of consumers will rely on structured product data, verified availability, and accurate pricing to surface recommendations. Brands and retailers will need to understand how agent-driven interactions influence demand and whether those interactions generate incremental growth or simply redirect existing spend. NIQ’s depth of purchase verification data, global retail measurement footprint, and AI-powered analytics infrastructure provide the foundation for answering these questions as they emerge.

Those that can operationalize commerce intelligence will define the next era of global growth.

From insights to action

| Action | Why it matters | How NIQ can help |

| Quantify where growth is coming from across emerging channels (live, social, quick commerce) | Emerging formats are now driving the majority of incremental digital growth. Retailers and manufacturers need clear visibility into which platforms, markets, and categories are moving fastest—and which represent the most profitable opportunities. | NIQ Omni E-Commerce Measurement Consumer Behavior & Insights Marketing Mix Modeling NIQ Matched Market Testing |

| Strengthen retail media investment with transparent, cross-platform measurement | As global RMN spend accelerates, brands need to understand true incrementality, avoid duplication, and optimize spend across fragmented networks. Better measurement delivers more efficient budgets and stronger retailer partnerships. | Retail Media Intelligence Retail Measurement Services Marketing Mix Modeling |

| Design assortment, pricing, and fulfillment strategies tailored to real-time consumption occasions | Quick commerce and omnichannel fulfillment models require mission-based assortments, precision pricing, and optimized availability. Brands that align to consumer need states win share and earn loyalty. | Assortment Planning & Optimization Omnichannel Commerce Scenario Forecasting |

With a global footprint, deep consumer insights, and AI-powered analytics, NIQ enables manufacturers and retailers to navigate this increasingly complex landscape. By linking consumer behavior, commerce platforms, and media performance, NIQ helps companies identify growth opportunities, measure what truly drives sales, and make confident decisions in the next era of globally interconnected retail. Contact us today.

Glossary

Core concepts

Closed-loop measurement

A measurement approach that directly links marketing exposure or engagement to actual purchase outcomes, enabling brands and retailers to assess true performance and return on investment across channels

Commerce intelligence

The ability to connect what brands and retailers need to know, what consumers need to discover and decide, and how platforms operate—through a unified, data-rich view of the commerce ecosystem

Unified commerce system

A model of commerce in which formats (e.g., live and social), infrastructure (e.g., payments, logistics, retail media), and AI-driven decisioning increasingly operate as an interconnected ecosystem—while still executed across distinct platforms and channels—enabling more seamless and personalized consumer experiences across the path to purchase.

AI and emerging commerce

Agentic commerce

A commerce model in which AI agents autonomously discover, evaluate, and purchase products on behalf of consumers, using real-time data such as pricing, availability, and preferences.

AI agent

A software system powered by artificial intelligence that can interpret user intent, make decisions, and take actions—such as recommending or purchasing products—on behalf of a consumer.

Large language model (LLM)

An AI system trained on large volumes of text data that can understand and generate humanlike language; increasingly used to power conversational interfaces, product discovery, and agent-driven commerce experiences.

Channels and formats

Live commerce

A format in which products are promoted and sold through real-time video streams—often hosted by creators or brands—combining entertainment, interaction, and immediate purchasing within a single experience.

Quick commerce (q-commerce)

A retail model focused on ultra-fast delivery—often within 30 to 60 minutes—enabled by localized inventory and designed to meet immediate or top-up consumer needs.

Retail media network (RMN)

A platform operated by a retailer that allows brands to advertise directly to shoppers using the retailer’s first-party data across digital and physical touchpoints, typically near the point of purchase.

Social commerce

The integration of product discovery and purchasing directly within social media platforms, where content, creators, and community influence drive awareness, consideration, and conversion.

Infrastructure and ecosystem

Dark store/Ghost store

A retail fulfillment location not open to the public, used exclusively to process online orders and support fast delivery models such as quick commerce.

Last-mile delivery

The final stage of the fulfillment process, in which goods are delivered from a distribution point or local hub to the consumer.

Super app

A digital platform that integrates multiple services—such as social media, payments, shopping, and delivery—into a single ecosystem, enabling seamless end-to-end consumer experiences.

Regional and market terms

Key opinion leader (KOL)

An influential individual—often with subject matter expertise or a strong following—who drives consumer trust, engagement, and purchasing decisions, particularly in Asian markets

Microdramas

Short-form, serialized video content—typically 60 to 90 seconds per episode—designed for mobile viewing and often used to integrate product promotion into storytellin

Top-up shopping

A purchasing behavior focused on replenishing a small number of essential items as needed, rather than completing a full shopping trip; commonly associated with quick commerce

Meet our contributors

Thank you to Skai and WeArisma for the data and insights they contributed to this report.

Thanks as well to our NIQ collaborators:

Disclaimer

All product and company names are trademarks™ or registered® trademarks of their respective holders. Use of them does not imply any affiliation with or endorsement by them.

Forward Looking Statement

This report may contain forward-looking statements regarding anticipated consumer behaviors, market trends, and industry developments. These statements reflect current expectations and projections based on available data, historical patterns, and various assumptions. Words such as “designed to,” “enable(s),” “allowing,” “creating,” “are enabling,” “offers,” and similar expressions are intended to identify such forward-looking statements. These statements are not guarantees of future outcomes and are subject to inherent uncertainties, including changes in consumer preferences, economic conditions, technological advancements, and competitive dynamics. Actual results may differ materially from those expressed or implied in these statements. While we strive to base our insights on reliable data and sound methodologies, we undertake no obligation to update any forward-looking statements to reflect future events or circumstances, except to the extent required by applicable law.