For decades, established European brands benefited from a powerful, often unspoken advantage: trust. Heritage, origin, and scale acted as shortcuts in consumers’ decision-making. Quality was assumed. Relevance was rarely questioned.

That era is ending.

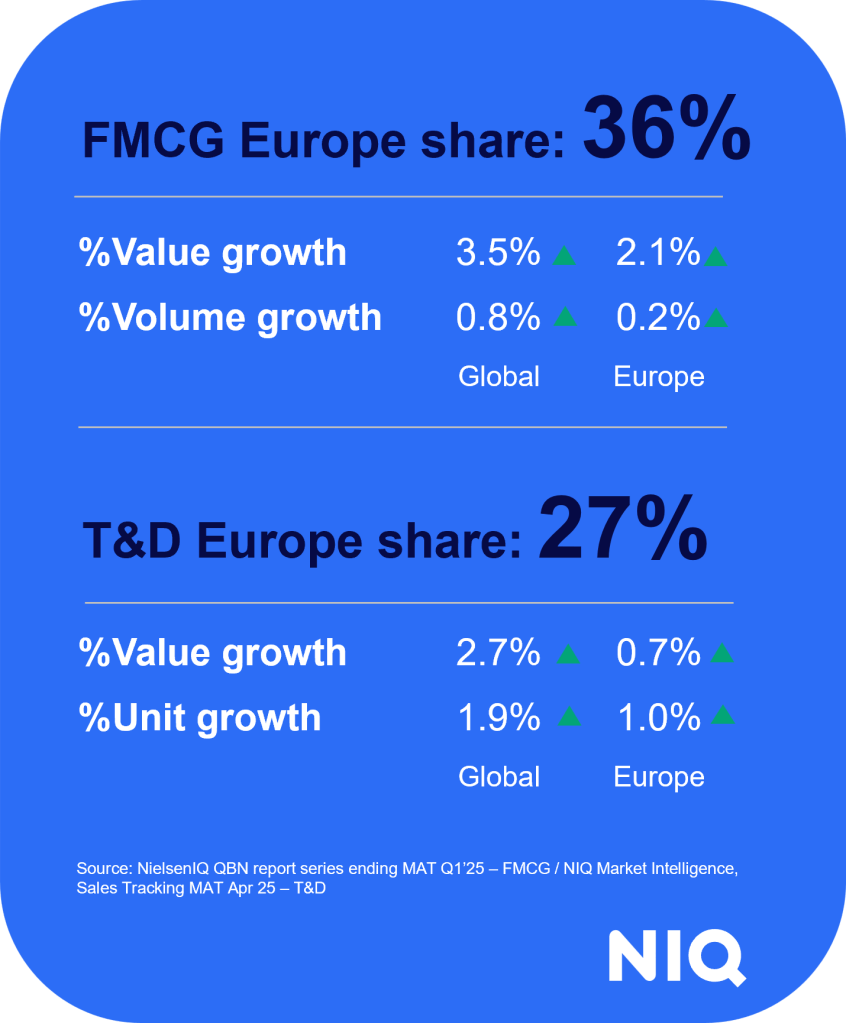

Western Europe, representing 36% of FMCG and 27% of T&D total global sales, has become the largest growth engine for Chinese brands.

As Chinese brands accelerate their expansion across Europe, they are not simply increasing competition. They are reshaping how brands are perceived, evaluated, and chosen. The real disruption is not price alone. It is redefining how brand equity is built.

From inherited equity to earned relevance

Brand equity was once cumulative. Years, sometimes generations, of presence created familiarity and reassurance. Today, consumers grant far less benefit of the doubt.

NIQ insights from the Automotive sector illustrate this shift clearly. In 2024, Chinese OEMs were no longer testing Europe quietly. At the Paris Motor Show, China was the most represented country, with a wave of brands from established names to new EV challengers, signaling long-term commitment to the European market. This visibility matters: it reframes Chinese brands from outsiders to credible alternatives.

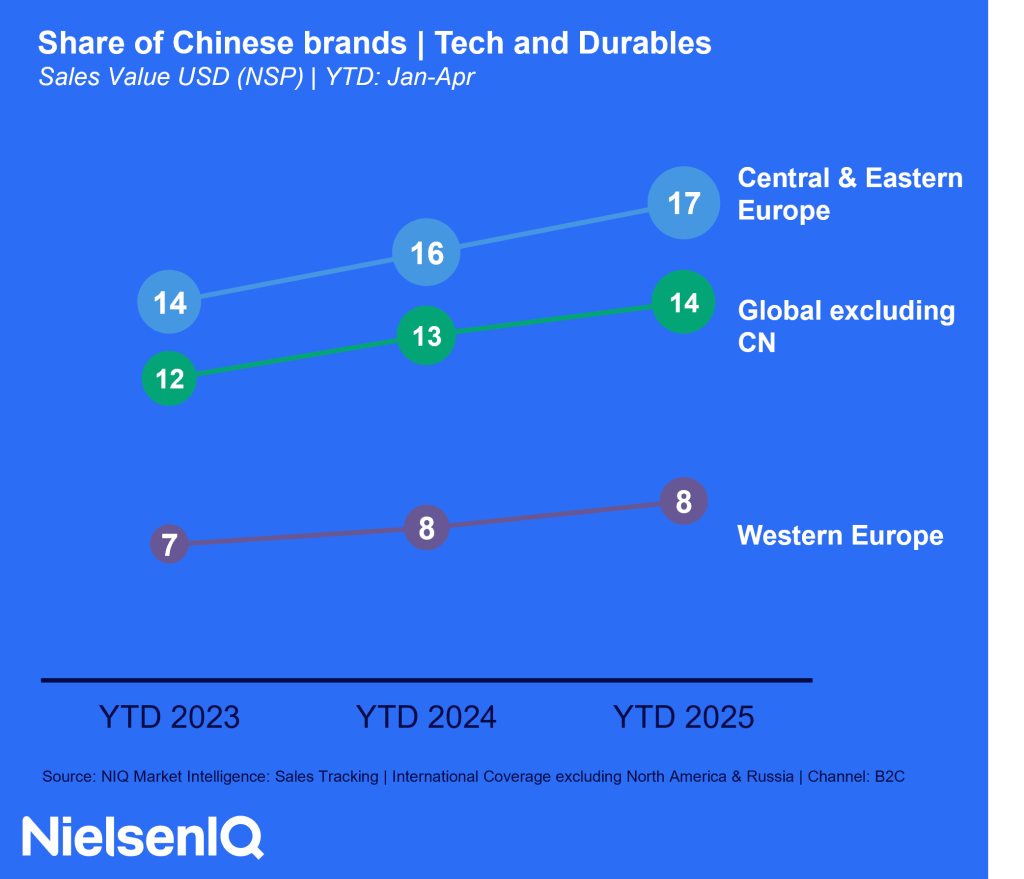

And this shift isn’t limited to automotive. Across Tech & Durables, Chinese brands are already reshaping competitive dynamics. In Consumer Electronics, Chinese players have moved beyond entry-level positioning to compete on feature performance and ecosystem integration. In Major Domestic Appliances, Chinese brands are gaining share by offering well-designed, energy efficient products at accessible price points.

If value-led disruption can successfully rewrite brand hierarchies in these high consideration T&D categories, then FMCG may well be the next frontier.

The implication for established European brands is stark. Heritage still matters, but it no longer closes the sale. Brand relevance must now be demonstrated at the point of purchase.

Where perception breaks: promise versus experience

Many European brands continue to rely on narratives of craftsmanship, tradition, and engineering excellence. Yet consumers increasingly anchor brand perception in lived experience: usability, performance, and perceived value for money.

Across both Automotive and Major Domestic Appliances, NIQ data shows that Chinese brands are closing, the experience gap. In Auto, earlier concerns around quality and reliability remain, but once consumers engage with the product, skepticism fades. In MDA, certain Chinese brands demonstrate a similar pattern: brand consideration grows when experience consistently meets consumers’ expectations.

When experience outpaces expectation, brand perception shifts quickly and brands that rely too heavily on storytelling without experiential proof risk losing credibility.

Confidence is re-earned, not inherited

Want to learn more?

Contact Us

Many established brands benefit from deep reservoirs of consumer confidence built over decades. Familiarity reduces risk, and legacy historically acted as a shortcut for quality. Today, that advantage is no longer guaranteed. Confidence has become more fluid and more conditional.

Chinese brands are not competing on heritage. Instead, they are earning consumer confidence through speed: faster innovation cycles, rapid market entry, and visible, frequent upgrades. In Automotive, the pace of EV rollout and feature iteration has made responsiveness itself a signal of relevance. In MDA and consumer electronics, energy efficiency, smart connectivity, and AI enabled features are resetting expectations just as quickly: shifting attention away from what a brand has been, toward how well it keeps up.

This shift is reinforced by more value literate consumers, growing awareness of global supply chains, and the scale Chinese brands enjoy in their domestic markets, allowing them to prioritize activation and relevance before fully building equity. Outcomes are already tangible: a Chinese brand takeover of a leading Japanese brand TV operations shows how quickly leadership can change when speed and value alignment outpace legacy. As familiarity with global tastes grows and consumers become more open to trying new benefits, the question is whether CPG could be next.

A shift in who holds the power

As adoption barriers (e.g. increased physical availability and online search) fall, discovery is easier and consumers are less constrained in their choice of brands. They compare more, switch more easily, and question price premiums more directly.

Automotive shows how quickly this can happen once switching feels “safe enough.” What begins as curiosity becomes normalization. Loyalty becomes conditional.

For European brands across industries, this marks a fundamental shift: brand power no longer sits with the brand alone, but with the consumer’s ability to validate value instantly.

Reading brand signals in a changing competitive landscape

The rise of Chinese brands does not signal the decline of European brands. But it does re-create the rules of how brand equity is built.

Familiar brands are questioned rather than assumed, and these signals often emerge well before any visible impact on sales. This is where brand tracking plays a different role.

Rather than acting as a retrospective scorecard, brand tracking becomes a way to observe how brand meaning evolves in real time: how trust is built or eroded, how relevance is gained or lost, and how the competitive frame itself is changing. It helps leaders see who consumers are starting to compare them with, and why.

The organizations best equipped to respond are not those that react fastest to headline threats, but those that notice the subtle changes early, understand what they mean, and adjust before those changes harden into lost relevance.

In a market where consumers no longer buy brands for who they used to be, the brands that win will be those that prove their value.

Brand equity is no longer inherited. It is earned every day.