Global automotive trends to watch in 2023

The car industry is expected to grow in the coming years, despite the volatile macroeconomic backdrop. Global car sales in 2023 are forecast to top 69 million, fuelled by greater penetration in emerging markets, growing adoption of electric vehicles and the reopening of China following its relaxation of Covid-19 restrictions. When coupled with consistent production volume and the sector’s demand backlog, these opportunities offer some resilience to the cost-of-living crisis and supply chain problems that are impacting sales and production. We expect car sales to rise further to 74 million in 2024, continuing the upward trajectory we have seen since 2020 toward the levels attained in the years before the pandemic.

Untapped potential in emerging economies

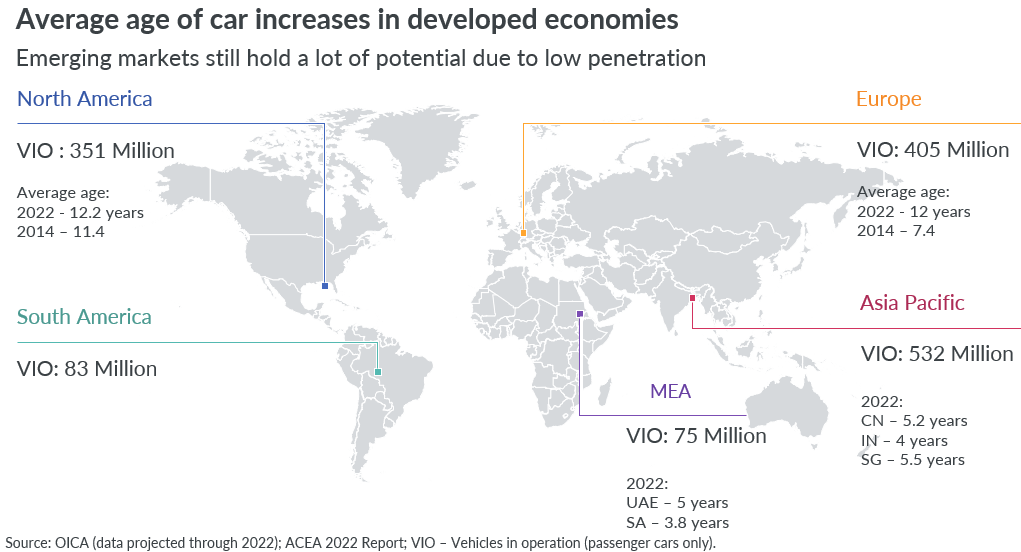

More than 85% of the world’s population live in Asia Pacific, the Middle East and Africa (MEA) or South America, yet these regions combined have fewer cars than North America and Europe. We expect to see some of this potential unlocked in the years ahead, with higher penetration in both car sales and automotive aftermarket categories.

Steady growth in the automotive aftermarket

Cost-conscious motorists in Western developed economies are increasingly reluctant to trade in their cars for newer models, creating the opportunity for growth in their automotive aftermarkets. There are three principal factors driving this market saturation:

- better quality and longer-lasting cars,

- strong second-hand car markets

- and consumers waiting for the price of electric vehicles to drop so they can switch.

The average age of a car in Europe is now 12 years, compared with just 7.4 years in 2014. In North America, too, the average age of cars has crept up, from 11.4 years in 2014 to 12.2 years in 2022. With a combined total of over 750 million passenger cars in operation on the two continents, this consumer behavior is expected to lead to greater demand for tires, spare parts and car chemicals.

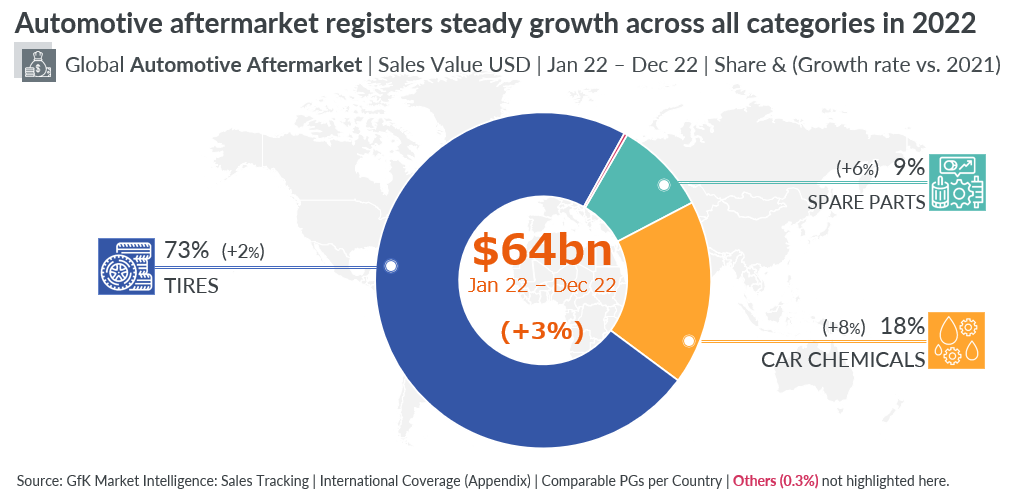

Indeed, the global automotive aftermarket grew by 3% to $64 billion in 2022, with steady growth across all categories and all regions, except for China and Developed Asia.

Tires, which account for almost three-quarters of aftermarket sales value, were up by 2% in 2022, spare parts by 6% and car chemicals by a robust 8%.

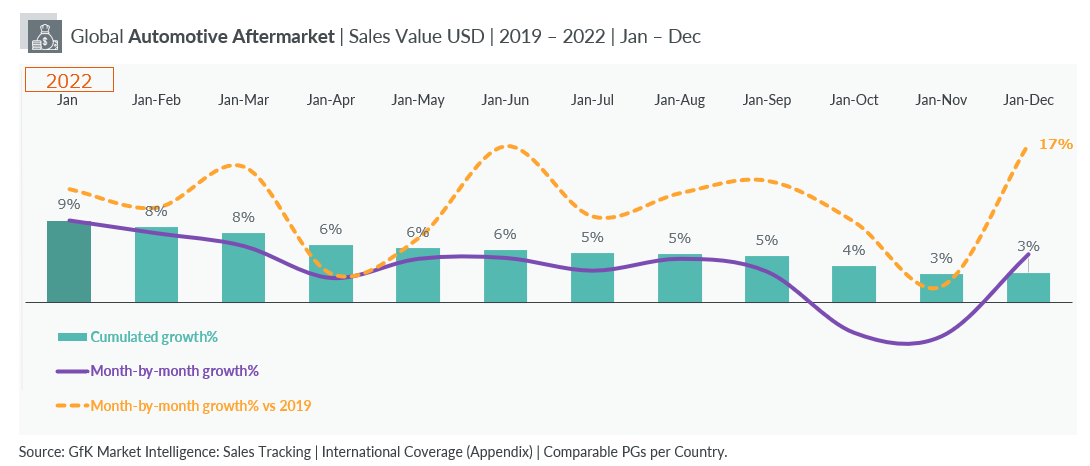

Revenue was also 10% up on pre-pandemic levels, most noticeably for car parts, which saw a 20% increase between 2019 and 2022.

The growth in the aftermarket is driven largely by post-pandemic mobility and higher product prices due to recent spikes in shipping and commodity costs, rather than demand, which fell in most regions in 2022 and in every category except for car chemicals. Bucking the trend were MEA and Emerging Asia, where both revenue and sales volume saw double-digit growth in 2022, another indicator of potential being unlocked in emerging markets.

The automotive aftermarket was certainly not immune to the impacts of the cost-of-living crisis, however. Following a buoyant 2021, growth slowed steadily throughout 2022 and especially in Q4 as motorists felt the double pinch of high energy and food prices.

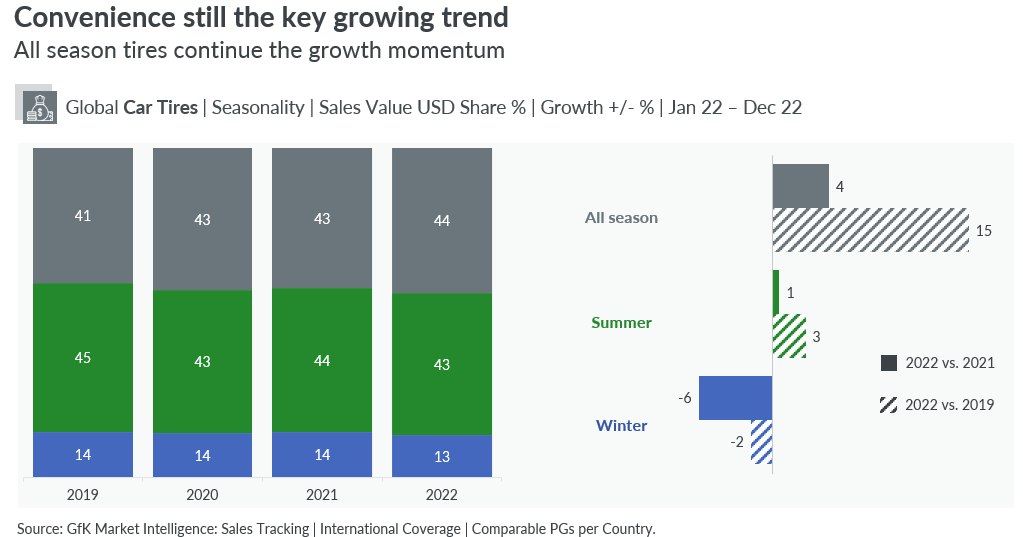

Tire trends: big and budget

All-season tires and those with the biggest rim sizes continued their strong growth trajectory, driven by the growing appetite around the world for bigger cars. We are seeing innovation that means consumers no longer have to purchase separate sets of winter tires in areas where winter weather is not typically harsh. For consumers, this means cost savings as they change their tires once each year while paying a higher rate for the service.

Light truck tires were a standout performer in 2022, growing by 5% on 2021 levels and 22% vs 2019 amid increased demand for logistics drivers and last-mile delivery. However, this growth is mainly being driven by the US market where there is a higher saturation of bigger cars.

Passenger car tires, though still dominating the market, performed weakly by comparison, up only 1% on 2021 and there was no growth in 4×4 tires over the year.

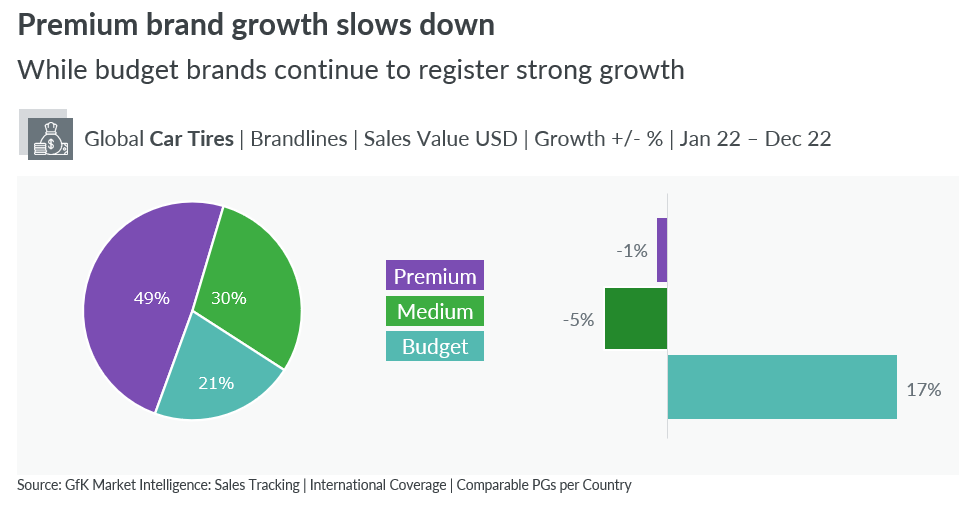

Budget brands for car tires grew across most regions, especially Latin America and the United States, as consumers tightened their belts in response to inflationary pressures. Another reason behind budget brand growth is availability. During the pandemic budget brands especially from China looked for growth in other regions, resulting in higher stocks in market. When these markets reopened, consumers with limited budgets went looking for the best deals. As a long term trend, medium and budget brands have increased their distribution as well as prices and will likely continue cannibalizing the premium share.

In most cases this meant a decline or only very modest growth in premium brands. The exception was in MEA which saw double-digit growth at all price levels, led by strong premium brand growth.

There were price hikes for tire brands across the board, especially budget lines, which took 21% of the sales value share in 2022 compared with 17% in 2019. Tapping into the sweet spot between tighter household budgets and the appetite for SUVS, brands also increased the range of large-rim tires available at low-end prices.

Small and synthetic engine oil trends

Global engine oils saw strong year-on-year revenue growth of 6.6% in 2022, driven mostly by price increases. There was also modest year-on-year unit growth of 2.2% although performance was slightly weaker than pre-pandemic levels.

Globally, sales value was up 13% on 2019, with the greatest increase seen in Europe and Emerging Asia.

Fully synthetic oils that offer better performance and convenience at a higher price continued their upward trend to command 54% of the market, and we expect this premiumization to continue in 2023.

Another trend we registered was the rise of smaller brands, such as Idemitsu and Motul, who continue to encroach on the market share of larger market leaders. However, the two largest companies combined still have a 29% stake in the market.

After the sharp rise in oil prices following Russia’s invasion of Ukraine in February, prices of global engine oils began to stabilize at high levels towards the end of the year, but uncertainty remains regarding future prices due to high market volatility.

E-mobility trends: sustainability and efficiency

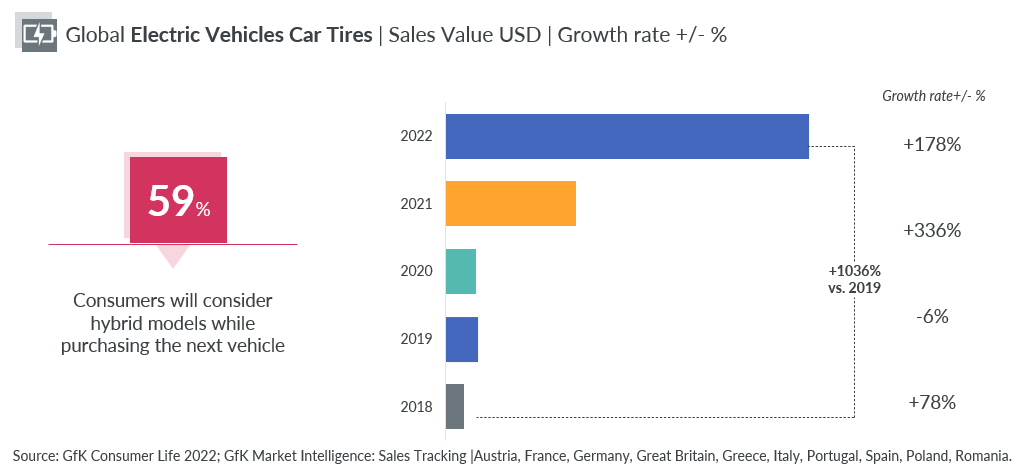

Battery-electric and plug-in hybrid vehicles accounted for 13% of global car sales in 2022 compared with 8% in 2021, as key markets pressed on with targets to phase out internal combustion engines over the next two decades. Almost six out of 10 consumers say they will consider a hybrid vehicle as their next purchase and the relentless march towards electrification can be seen in metrics such as global revenue from electric vehicle car tires which jumped up by more than 1,000% between 2019 and 2022.

The electric car industry could see high levels of growth over the coming years. For smart automakers and their tier 1 suppliers, there are opportunities to innovate in the growing software-defined vehicle (SDV) space with new software-centric features and functions that improve safety, convenience and the in-vehicle experience. As businesses come under increasing pressure to cut carbon and optimize logistics to mitigate inflation, there is also growing interest in efficient electric fleet vehicles that reduce the total cost of ownership.

Outlook for 2023

Managing high inventories and navigating market price volatility of raw materials are among the challenges the automotive aftermarket and car industry are likely to face in 2023. Inflation, food and energy costs will continue to be at the forefront of consumers’ minds, pushing them toward more affordable products.

However, premium segments that offer performance and convenience, such as all-season, bigger rim sizes and synthetic oils, will continue to fuel growth. Emerging economies will offer opportunities for smart manufacturers while China’s reopening will support the sector’s resilience. Meanwhile, the sustainability imperative will reward innovative brands whose products respond to mounting regulatory and consumer pressure for more environmentally friendly alternatives.

Get a deeper understanding of your market, with GfK’s Future of Mobility report

![]()