Navigating uncertainty with resilience

Today’s business leaders are facing a uniquely challenging moment: Shifting policies, fluctuating consumer sentiment, and economic uncertainty have created an unpredictable environment where day-to-day decision-making—let alone planning for the future—feels overwhelming.

In moments like these, most economic outlooks offer broad trends or surface-level forecasts. This one is different.

We’re delighted to once again collaborate with Yale economists Martha Gimbel and Ernie Tedeschi to bring you this business resiliency playbook. Taking a deep dive into 50 years of historical US data, they reviewed consumer behavior across major economic shocks—from recessions and stagflation to geopolitical crisis. Their analysis reveals not only how consumers respond in each scenario, but also the key signals that indicate shifts are coming.

Making this playbook actionable is our business resiliency framework—a detailed guide that outlines how to interpret these signals, along with specific steps retailers and manufacturers can take to respond to them with agility and confidence. We hope you’ll use it as a strategic compass to guide your planning and position your business for resilience and growth in the months ahead.

Vice President, Global Thought Leadership, NIQ

Courtenay Verret is Vice President, Global Thought Leadership at NIQ, where she connects data-driven insights with compelling narratives that position the company at the forefront of consumer intelligence. Her work spans critical topics such as AI, innovation, and brand marketing, helping shape strategic conversations. Courtenay plays a key role in amplifying NIQ’s brand authority by fostering influential partnerships, driving executive engagement, and delivering insights that resonate across industries and markets.

About the authors

Economist

Martha Gimbel is the Executive Director of The Budget Lab at Yale. She has worked as an advisor and an economist in senior roles across government, the private sector, and philanthropy, including the White House Council of Economic Advisers, the Department of Labor, the Joint Economic Committee on Capitol Hill, Schmidt Futures, and Indeed.com. She is an expert in a range of economic data, including the labor market, consumer spending, inflation, and economic growth, and in how economic and policy dynamics intersect.

Economist

Ernie Tedeschi is the Director of Economics at The Budget Lab at Yale and a Visiting Fellow at the Psaros Center for Financial Markets and Policy at Georgetown University. He is also a regular Bloomberg Opinion columnist. Until March 2024, he was the Chief Economist at the White House Council of Economic Advisers (CEA). Prior to CEA, Ernie was Managing Director and Head of Fiscal Analysis at Evercore ISI. He has also been an economist at the US Department of the Treasury and a contributor to the New York Times Upshot column.

What drives consumer behavior in periods of uncertainty? Get a preview of what you’ll find in The Business Resiliency Playbook—and then keep reading!

Want to read later?

Planning for business resilience? Or decision-making in the dark?

Where is the economy heading?

And how will consumers respond?

These questions are undoubtedly top of mind for manufacturers and retailers as they face a global economic landscape marked by an extraordinary degree of uncertainty. But in our quest to forecast what’s coming, are we overcomplicating what really matters for building business resilience?

From shifting trade policies and geopolitical tensions to volatile financial markets and evolving consumer behaviors, today’s environment is more unpredictable now than at any point since the pandemic five years ago. This uncertainty is not an abstraction—it’s a daily reality, shaping the decisions of businesses, policymakers, and consumers alike.

For business leaders, this unpredictability presents a challenge: Decisions about pricing, hiring, supply chain investments, brand positioning, and innovation pipelines must be made in the face of incomplete information and rapidly changing conditions. Traditional models and former precedents may no longer provide reliable guidance, making it difficult to chart a clear path forward. Yet, choosing not to act—delaying key decisions or defaulting to the status quo—is also itself a decision, one that can leave organizations exposed to risks and missed opportunities.

In a 2022 report, McKinsey found that the actions a company takes before any sort of economic shock—for example, what it does to prepare or where it invests—could account for as much as half of the gap in shareholder returns between leaders and those who lag behind.

In this context, business resiliency planning isn’t just advisable—it’s essential. The manufacturers and retailers best positioned to navigate uncertainty are those that have proactively developed strategies to withstand shocks and adapt to new realities. But before crafting a resilient plan, it’s crucial to first understand the potential scenarios that could unfold over the next couple years. This requires a rigorous assessment of both the risks of the current environment and a thoughtful exploration of how similar risks played out in the past.

For this report, we’ve designed an analysis to give business leaders the insights they need to anticipate and prepare for a range of possible futures. By mapping out distinct scenarios for consumer spending, we aim to provide a framework that enables agile decision-making and strategic foresight. Our goal isn’t to predict the future, but to help organizations develop robust plans that can adapt as conditions evolve.

To do this, we draw on experiences of the past to help calibrate what the next couple years might hold. Historical episodes—the stagflation of the 1970s, the significant recession of the early 1980s, the mild recession of 1990, the soft landing of the mid-1990s, and the oil/geopolitical shock of 2022—offer invaluable lessons in how consumers respond to economic disruptions and uncertainty. During such periods, consumer priorities often shift rapidly, with spending on essentials taking precedence over discretionary purchases, and brand loyalty being redefined by perceived value and trust.

Importantly, our analysis suggests three key findings:

1

First, across each of the historical episodes we reviewed, consumer behavior followed similar patterns, regardless of the stimulus. Moving forward, it’s crucial that business leaders not put too much weight on which stimulus consumers will react to. Consumers don’t care why they’re stressed—they just know that they are. And they tend to respond accordingly.

2

Second, as predicted, in each of the economic scenarios we reviewed, consumers pulled back on “nice-to-haves” and gravitated toward value-seeking behavior, to greater or lesser extents, depending on the size of the shock. Rather than anticipating an infinite number of scenarios, business leaders should instead stay attuned to the key data signals flagged here that could indicate a behavioral shift is coming.

3

Critically, at the time of this analysis (summer 2025), the NIQ data we reviewed indicates that consumers aren’t demonstrating widespread signs of stressed behavior, despite recent fluctuations in sentiment. This could change at any time, given dynamic conditions on the ground, but it reinforces the idea that consumer sentiment is only one data point to act on. Business leaders must stay vigilant—and balance what consumers say with actual shifts in what they do.

“Our goal isn’t to predict the future, but to help organizations develop robust plans that can adapt as conditions evolve.”

Past is prologue: Five historical scenarios that could mirror future outlook

The outlook for the US economy over the next two to three years is unusually uncertain, with several plausible scenarios—each carrying different implications for growth, inflation, and consumer spending.

Despite volatility month to month, real consumer spending is still up nearly 1% since last October, and real durable goods spending is up nearly 2%. A largely stable labor market has been supporting the consumer (although recent data suggests signs of weakening), while wages and income growth have grown faster than inflation, providing some support to consumer purchasing power despite persistent price pressures. Inflation is still slightly elevated but has come down from the unusually high levels (e.g., 7–9%) of 2022.

Consumer sentiment and broader economic indicators are mixed, however. The Consumer Confidence Index and University of Michigan’s Survey of Consumers have both shown a rebound since their lows earlier this year; however, consumer attitudes are still down from late 2024. Meanwhile, preliminary results from NIQ’s annual Consumer Outlook survey indicate overall increased levels of optimism since a year ago; however, concerns about the potential for rising food prices, economic downturn, and geopolitical conflict remain top of mind for most—illustrating just how challenging it is to keep up with consumer mindsets during this time.

Economic growth has also been mixed: Real GDP growth was negative in Q1 2025 but beat expectations, at 3%, in Q2. Even with this bounce back, average growth over these first two quarters was still only 1.2%, down from 2.5% in 2024. There also could be upward inflation pressure and labor supply contraction over the next year, depending on evolving US policies (e.g., trade, immigration, Federal Reserve prime rate, reconciliation tax package).

Drawing on both current data and historical parallels, we can outline five principal scenarios that could impact the US economy and challenge business resilience over the next few years:

- Stagflation

- Mild recession

- Deep recession

- Soft landing

- Geopolitical shock

Note that these are not intended to cover all possibilities, nor are they mutually exclusive. A recession may be “stagflationary,” for example, while geopolitical shocks may underpin all of them. The direction the economy ultimately takes will depend on the interplay of monetary and fiscal policy, the trajectory of inflation, the evolution of global trade and geopolitical risks, and the resilience of consumer demand.

Stagflation (1970s)

“Stagflation” is characterized by slow growth, high unemployment, and persistent inflation. This scenario echoes the 1970s, when oil shocks and policy missteps produced a toxic mix of high prices and stagnant output. During that era, consumers sharply curtailed discretionary spending, trading down in categories like Apparel and Durable Goods, while prioritizing essentials such as Food, Energy, and Housing.

Like in the 1970s, brands with strong value propositions, including private label alternatives, might gain share, while loyalty could erode in the face of rising prices.

Mild recession (1990–1991)

A recession is a sustained contraction in economic activity. A “mild” recession would be reminiscent of 1990–1991, when growth slowed sharply but systemic financial distress was avoided. Typically, the unemployment rate would rise. In the wake of 1990, it ultimately rose about 2 percentage points, but in principle a smaller rise might still be consistent with a recession call. In the end, real goods spending declined by 4% between July 1990 and January 1991.

In this scenario, like in the early 1990s, consumer spending would likely decline—especially for big-ticket categories like Autos, Home Furnishings, and Travel. Essentials would be less affected, but even here, consumers would likely trade down or delay purchases.

Deep recession (1980–1981)

A deeper recession, akin to the early 1980s, could result in a significant unemployment spike and a more pronounced slump in discretionary and durable goods spending. The unemployment rate rose 5 percentage points after 1980, and real goods spending dipped 6% lower, not recovering to January 1980 levels until early 1983.

Historically, these periods see sharp drops in home construction, vehicle sales, and luxury goods, while discount and value retailers outperform.

Soft landing (mid-1990s)

A “soft landing” is the most optimistic scenario we’re examining, in which the US Federal Reserve successfully brings inflation down to its 2% target without triggering a recession. In this case, growth could slow but remain solidly positive (around 1.5–2% annually), the unemployment rate would edge up only slightly (stay below 5%), and, as mentioned, inflation would gradually return to target levels. The mid-1990s offer a historical parallel: The Fed preemptively raised rates to cool inflation, but the economy continued to expand, and consumer spending remained resilient, albeit with some shifts toward value and essentials.

In this environment, discretionary spending would likely stabilize, and categories tied to home improvement, travel, and experiences could see renewed growth as consumer confidence recovers.

Geopolitical shock (2022)

Geopolitical events—such as escalated conflict in Eastern Europe or instability in the Middle East—could also deliver sudden shocks to the economy. The 2022 Russian invasion of Ukraine, for example, caused energy and commodity prices to spike, eroding consumer purchasing power and triggering market volatility, but ultimately having little to no impact on the labor market. The 1973 energy shock had much more serious consequences.

In such scenarios, inflation could re-accelerate even as growth slows, leading to a “stagflation-lite” environment. Consumers would likely respond by further prioritizing necessities, trading down in food and household goods, and deferring discretionary purchases. Supply chain resilience and pricing flexibility would be critical for businesses navigating such shocks.

Key takeaways:

- Economic signals are currently mixed: While spending is up, growth has slowed from last year and consumer sentiment is in flux.

- Multiple economic paths are plausible—each with distinct business implications.

- The direction the economy ultimately takes will depend on the interplay of monetary and fiscal policy, the trajectory of inflation, the evolution of global trade and geopolitical risks, and the resilience of consumer demand.

Different shocks, familiar patterns: Decoding consumer behavior under pressure

In a soft landing, we would expect current consumer trends to continue and not see a huge break from present-day behaviors. But how does consumer spending for different goods respond under the other macroeconomic scenarios?

To assess this question, we share two layers of analysis:

- The first looks back historically at periods that align with the macroeconomic scenarios laid out above and calculates how real consumer spending (inflation-adjusted Personal Consumption Expenditures—or PCE—from the US Bureau of Economic Analysis) changed over the subsequent two years.1 We show the results for four of these periods relative to the soft-landing period that began in January. PCE categories cover all monthly consumer spending, including services, but lack the detail to answer important questions—for example, the ability to distinguish within categories among different brands.

- In the second analysis, we use NIQ data to dig more deeply into some of the most historically sensitive product categories, which allows for more differentiation between products and high-frequency detail.

1 Full results of the analysis are in the chart labeled “Full historical real PCE consumer goods analysis.” In summary, the analysis calculates the percent “gap” of monthly real consumer spending per capita for each of nearly 200 PCE categories against trend. “Trend” here is calculated as the Hodrick–Prescott (HP)–filtered trend of log real spending per capita for each category with a band-pass window of 20 years (equivalent to an HP smoothing parameter of roughly two million). The calculation of trend allows the analysis to account for long-run consumer preference changes. The change in the gap shown in the chart for each historical period is the average percentage point gap over the second year out (13–24 months from the beginning of each period) minus the average gap over the 12 months ending with the period start (the month of the period start itself plus the 11 preceding months).

The outcome of our first analysis suggests a perhaps surprising result: To prep for consumer behavior under one outcome is to be well-prepared for the other outcomes as well. In general, across all economic shocks we evaluated, consumer behavior followed similar patterns.

During times of economic stress—regardless of its classification or cause—consumers tend to pull back on bicycles, cars, sugar and sweets, and photographic equipment, among other goods. Few goods are left unaffected—although some are affected less (e.g., tobacco). Unsurprisingly, “nice-to-haves” are more affected than “need-to-haves” when consumers have to pull back—the exception being a small treat or affordable luxury that can substitute for bigger savings (e.g., an increase in spending on meat in the face of a recession likely reflects that consumers are no longer going to restaurants and are instead buying more to cook at home).

Interestingly, as the continuation of our chart below shows, some categories actually saw increases in spending—including watches and “pleasure aircraft.” This may suggest that luxury spending can hold up relatively well during times of change, as more well-off consumers remain insulated from economic swings.

Although the stress response across scenarios is similar, the scale and speed of that response is likely proportional to the magnitude of the shock. In other words: The more severe the disruption, the faster and more pronounced the behavioral shifts will likely be. A major recession may trigger swift and widespread pullbacks, whereas a mild downturn or stagflation might result in more gradual or limited adjustments. Similarly, some geopolitical shocks could rival the economic impact of traditional recessions, depending on their scope and consumer visibility. Understanding this scaling effect is critical for anticipating the depth and duration of demand shifts across categories.

Especially in periods of change, building business resiliency means being prepared and staying attuned to the data to see trends as they emerge. Unfortunately, this can pose a challenge for several reasons:

1

Leaders must navigate not only where to look, but also what to look for. They must determine which data sources are the most effective for their business, as well as the most relevant shifts in consumer behavior they should be monitoring in uncertain times.

2

Leaders must understand not only the overall spending picture, but also how consumers are adjusting their behavior in the shopping aisle and across channels in real time. Are they trading down, switching to private label or seeking deals, pantry loading, or pursuing other money-saving strategies?

3

Leaders must anticipate change. Due to the publishing lag time and backward-looking nature of government data, it can be difficult to capture trends as they emerge.

Regardless of category, fast-moving consumer goods (FMCG) data makes an ideal use case for pulse checking the state of the consumer. Given its high turnover rate, variety of purchasing channels, and opportunities to trade up or down, we can see even slight behavioral shifts that, in combination with our historical analysis and consumer sentiment data, might signal larger emerging trends. By regularly monitoring overall market and category data—especially those that are historically sensitive during economic shocks—businesses can anticipate needed price adjustments and promotions, right-size their product portfolios, and adjust marketing strategies and budgets.

Premium content below

To demonstrate what this looks like in practice, we reviewed our historical analysis and selected a number of FMCG categories sensitive to growth and decline that may indicate consumers are moving toward a more pressured state.

The pressured consumer: Areas of pullback

- Seafood (e.g., shrimp, salmon, crab, tuna)

- Sugar & Sweets (e.g., Candy, Gum & Mints; Sweet Snacks; Desserts)

- Household Care (e.g., cleaning products)

The pressured consumer: Areas of growth

- Ready-to-Eat (RTE) Cereal

- Meat (e.g., beef, pork, lamb, chicken)

These spending behaviors are consistent with consumers pulling back on “nice-to-haves” and trying to retrench at home: While purchasing meat to cook versus dining out can save money, seafood is often the pricier option. Likewise, consumers may simplify cleaning routines or cut back on sweets to save a few dollars, whereas cereal can often stand in as a cheap meal on its own.

Price, pressure, and pullback

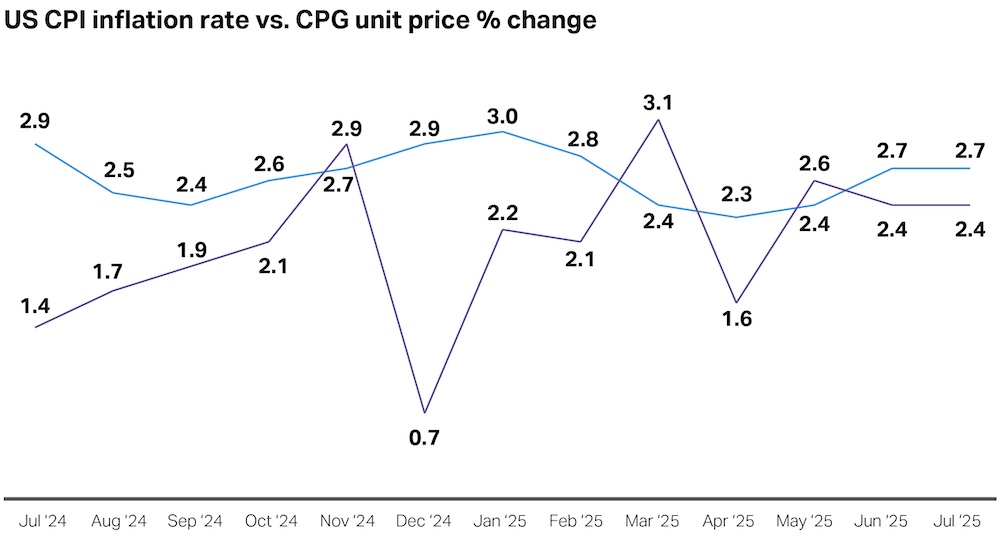

To begin, let’s take a look at our present state of inflation.

Headline Consumer Price Index (CPI) grew 2.7% over the 12 months ending in July 2025, whereas core CPI, which excludes volatile food and energy prices, grew 3.1%. With some month-to-month exceptions, CPG inflation overall has been trending lower than CPI numbers and remains stable at 2.4% as of July.

Source: US Bureau of Labor Statistics, Consumer Price Index; NielsenIQ, Total US Full View, through July 26, 2025

On the one hand, at the time of this writing in summer 2025, these inflation rates are down substantially from the heights they reached in 2022, and some important categories, like rent, are still seeing inflation easing, keeping down the topline number. On the other hand, inflation is still meaningfully above the Federal Reserve’s target of 2% PCE inflation.

Goods prices—the category of spending most exposed to tariffs—are firming. Over the first six months of 2025, prices of core commodities grew 0.6%; they typically fall in price over most years. Moreover, key tariff-sensitive goods like furniture, electronics, and appliances are seeing even faster price increases. Private sector analysts expect additional pricing pressure during back-to-school shopping season, as pre-tariff inventories are further exhausted. The Budget Lab at Yale projects that if current tariffs stay in place, they will eventually raise the price level by 1.8% over the course of one to two years, assuming the Fed ignores their price effects.

With the big picture in mind, we turned to NIQ data in our historically sensitive categories to determine whether any patterns are emerging there.

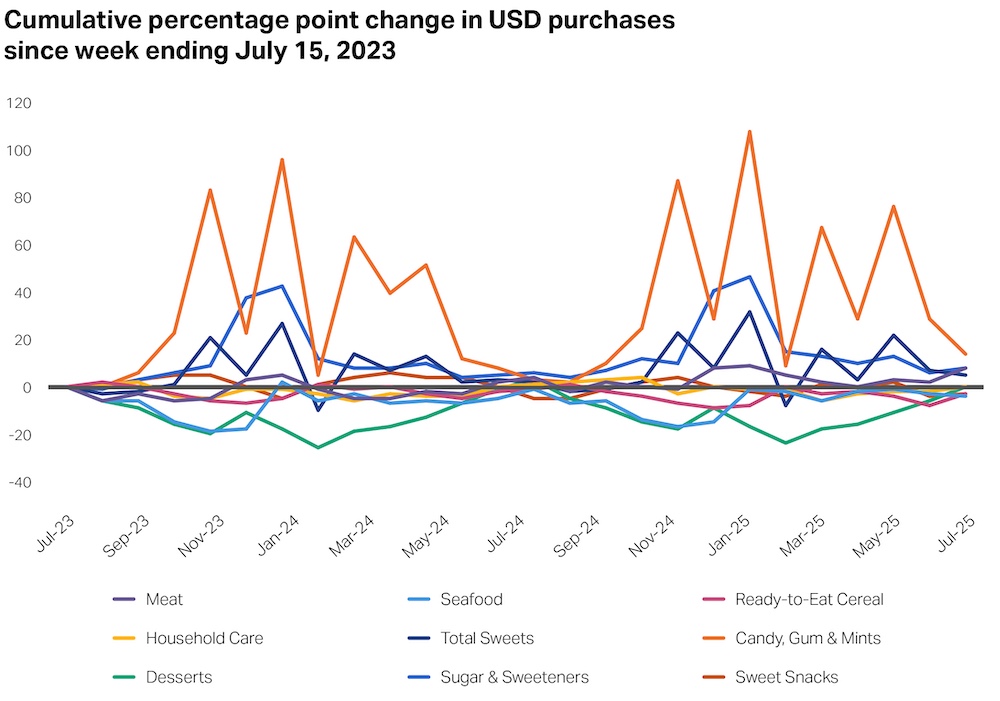

Although price levels have gone up as normal, there hasn’t been much movement aside from normal seasonal patterns, which likely reflects that consumer behaviors have been relatively calm overall.

Source: NIQ RMS Total US Full View

Relative to July 2023, overall spending in all these categories is also functionally flat (the spikes for sugary foods also largely reflect seasonal variation—i.e., Halloween, Christmas, Easter, etc.).

Source: NIQ RMS Total US Full View

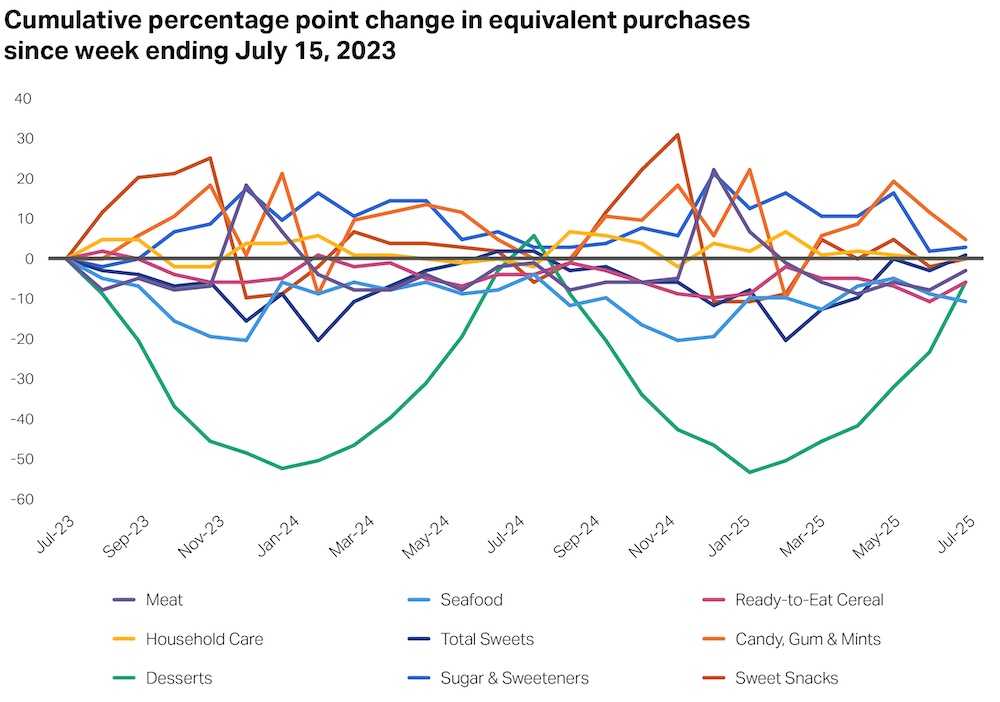

Similarly, apart from some seasonal variation, there hasn’t been a big change in the overall number of units of these goods that consumers are buying.

Source: NIQ RMS Total US Full View

In many ways, these charts may reflect what many businesses have been observing— and what recent data has indicated: Despite fluctuating confidence and sentiment, consumers are continuing to spend overall. That said, over the past year (through mid-June 2025), unit purchases in these represented categories are modestly down across the board. This finding illustrates how hard it can be to divine consumer stress from the data. Sugary foods in particular may be down due to the rise in GLP-1/anti-obesity medication availability and usage. Price dynamics unrelated to consumer stress or tariffs also may be playing a role.

Source: NIQ RMS Total US Full View

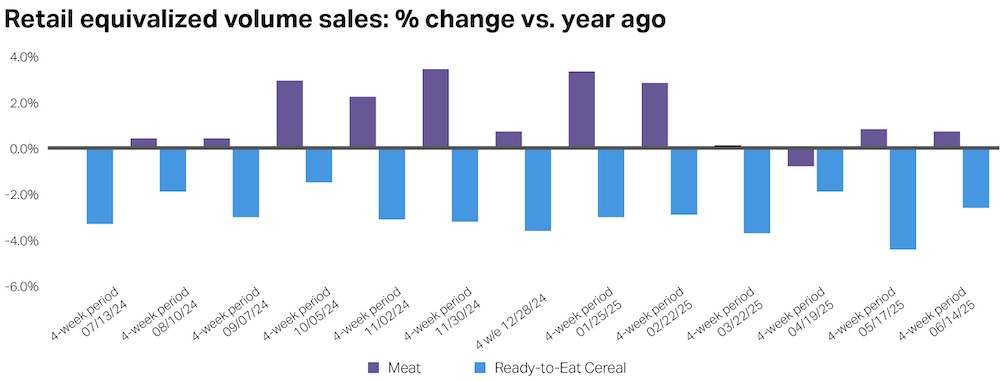

Focusing on growth, not levels, we see mixed evidence of stress. Growth in Meat sales, for example, has turned weak over the last several months. Based on historical patterns, this could indicate a lack of growing consumer pressures. However, it more likely reflects accelerating prices: Beef and veal prices have grown 6.5% year to date in the CPI (versus 1% over the first six months of 2024).

Likewise, RTE Cereal purchases have seen consistent negative growth over the past year, with growth from end of April through mid-May 2025 being the weakest during this period. Unlike Meat, RTE Cereal prices are down 0.6% year to date—and are only slightly (0.6%) higher than a year ago. Weaker cereal demand could likewise indicate less stress among consumers, but it could also reflect meaningful shifts in consumer preferences, such as against processed foods.

Source: NIQ RMS Total US Full View

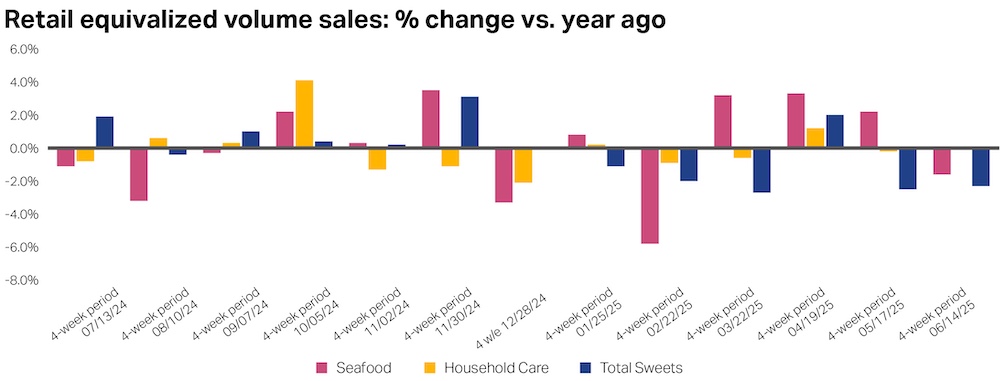

On the other hand, many products for which we would expect to see sales declines under stress scenarios are, in fact, declining. While Seafood, Household Care items, and Total Sweets don’t always grow in tandem, over the 52 weeks ending in mid-June 2025, equivalent sales for all three categories fell or remained flat, as we saw earlier.

Note that this has not been a consistent monthly pattern, however: As recently as mid-April, all three categories experienced growth.

Source: NIQ RMS Total US Full View

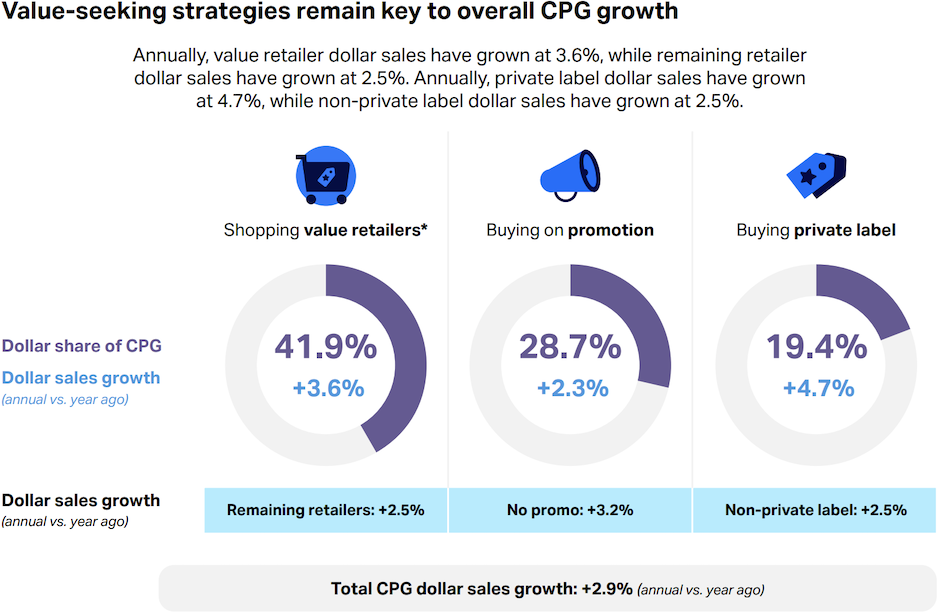

Value-seeking strategies

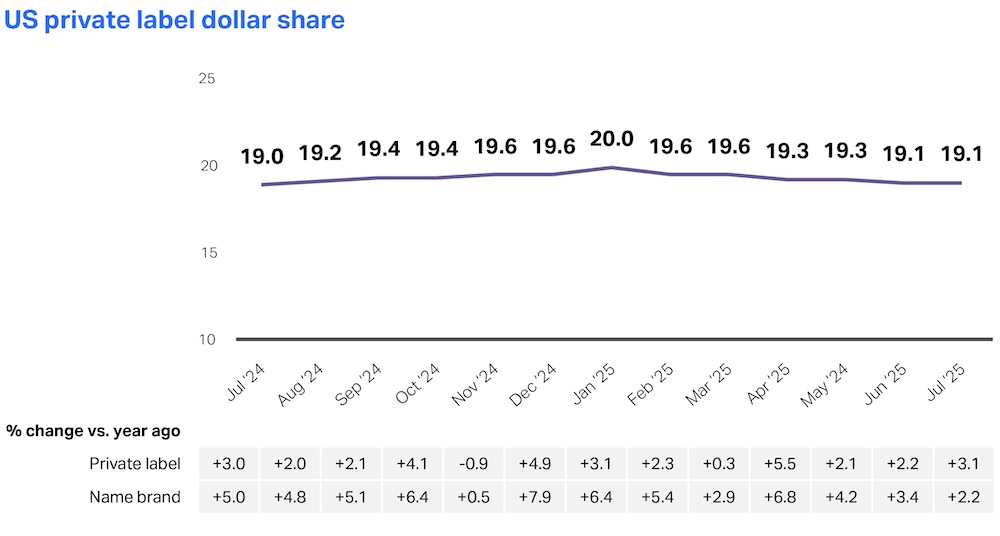

But what about pre-emptive, value-seeking strategies as a whole? In a recessionary period, for example, we tend to see outsized growth for value retailers and private label brands. Even if prices are currently steady overall, is it possible that consumers are beginning to prepare for harder times ahead by switching to value retailers, shopping for promotions, or proactively trading name-brand products for private label ones?

Source: NielsenIQ, Total US Full View, 52 weeks ending July 26, 2025; *value retailers (Mass Merch + Club + Dollar)

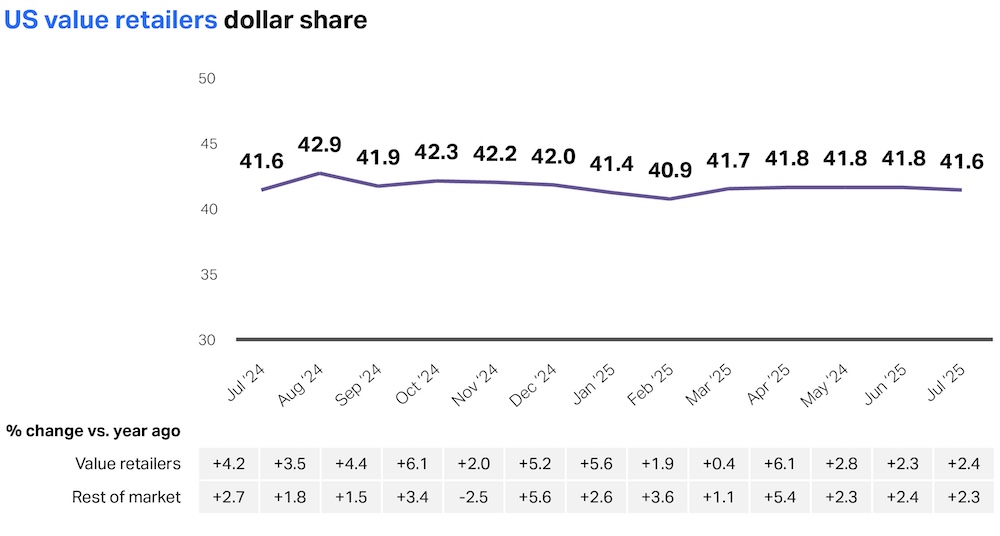

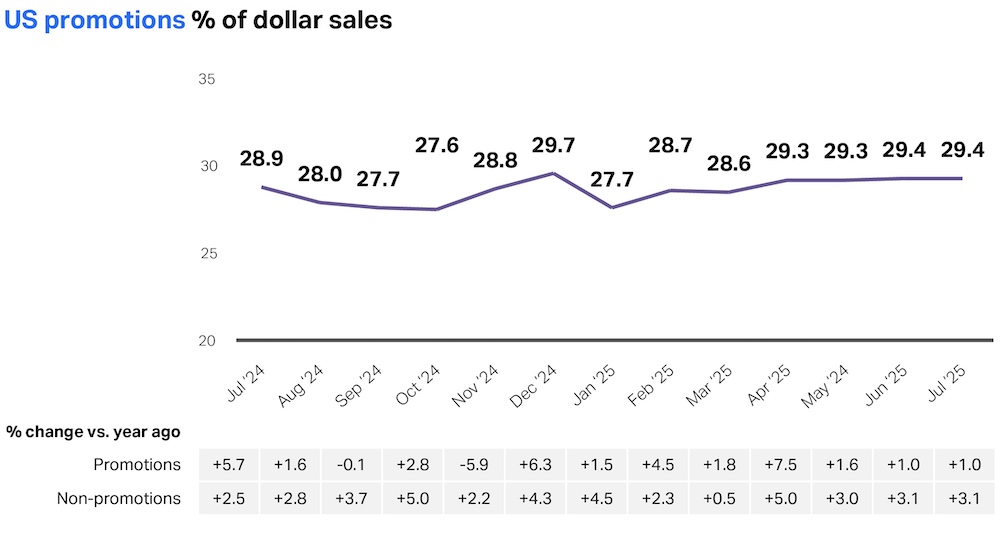

In the big picture, value-seeking strategies are up overall in the last year—an indication that consumers continue to be intentional about their spending habits. However, when we look at month-to-month growth for value retailers, promotions, and private label, the trajectory is slow—and, over the last few months at least, quite stable.

Source: NielsenIQ, Total US Full View, value retailers (Mass Merch + Club + Dollar), 4 weeks ending July 26, 2025

Source: NielsenIQ, Total US Full View, promotional dollar sales 4 weeks ending July 26, 2025

Source: NielsenIQ, Total US Full View, private label dollar sales : 4 weeks ending July 26, 2025

Private label makes for a particularly interesting case: Although its overall growth rate has begun to slow while brand names see a resurgence, the positive perception of—and retailer investment in—private label quality means that if hard times return, switching to a value option is less of a sacrifice than it might have been in years past.

For now, it appears that private label in the US is maintaining its modest growth trend as consumers discover or return to some of their favorite brands.

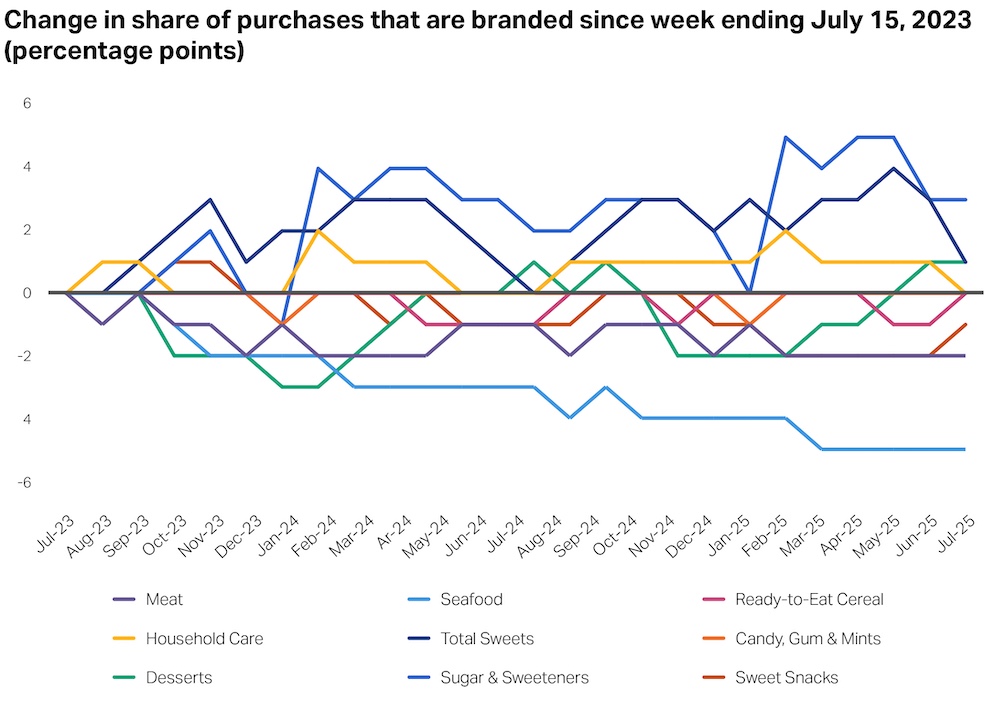

But what about in our historically sensitive categories? Given that these areas typically see some of the biggest pullback or growth during economic shocks, could there be any indications that a trade-down for nice- or need-to-have products is underway?

Source: NIQ RMS Total US Full View

That behavioral response doesn’t seem to be happening. Here, too, we see that consumer spending on branded items in most of these categories has stayed functionally flat, though Seafood is a notable exception, with a steady 5 percentage point decline in branded purchases since mid-2023. Although we will need to keep an eye on this trend, for now, consumers still seem to be choosing products according to their full value proposition instead of price alone.

Key takeaways:

- Across all economic shocks we reviewed, consumer behavior followed similar patterns: pulling back on “nice-to-haves” while leaning into “need-to-haves.”

- While the consumer response to stress is similar under all scenarios, the scale and speed of their response is likely proportional to the magnitude of that shock.

- By regularly monitoring overall market and category data—especially those that are historically sensitive during economic shocks—businesses can better anticipate their next moves.

- At the time of this analysis (summer 2025), we see no overt signs of behavioral shifts in our present-day NIQ consumer data that could signal a sudden downturn. This could change at any time—and it will be important for business leaders to stay attuned to the signals and actions we outline in our next section.

Plan for business resilience: Key signals and strategies to guide future scenario planning

Now that we’ve grounded ourselves in the data to understand past outcomes and present scenarios, what do we do with that information?

The good news: As we stated at the outset, despite the high level of uncertainty about where the US economy is heading, there’s no need to overcomplicate scenario planning to the point of paralysis. As our analysis showed, in an economic shock, consumers aren’t concerned with the hows and whys of being pinched—they simply know that they are, and their behavior follows similar patterns across each environment.

The trickier news: Consumer sentiment can be misleading in a vacuum, given the disconnect that often occurs between what consumers say and what they do. As we saw in our analysis, despite fluctuating levels of optimism, overall spending remains steady. This means business leaders will need to stay attuned to consumer sentiment alongside other data sources for any emerging signals that might indicate an increase or decrease in economic pressure.

To guide manufacturers and retailers in navigating next steps, we’ve assembled a framework outlining critical signals to pay attention to in the coming months—along with corresponding actions to meet them. We should note that these signals are not all-inclusive and could shift with evolving economic conditions on the ground. Likewise, these corresponding recommendations should not be viewed as a one-size-fits-all action plan but as a valuable jumping-off point to build your own business resiliency strategies in a manner that makes sense for your company’s unique position, challenges, and opportunities.

Scenarios: Recession | Stagflation | Geopolitical shock

What to watch for

| Signals | Behavioral insights | Manufacturer actions | Retailer actions | How NIQ can help |

Inflation continues to steadily rise more than expected; CPG inflation follows suit. | Tariff costs and labor shortages are likely showing up in supply chains and production more prominently, raising prices. The Federal Reserve could react with higher interest rates or fewer interest rate cuts. | Re-evaluate supply chain diversification Determine how much price you can absorb—and how much must be passed on to consumers Create well-supported price and promotional strategies to offset increases while still driving revenue | Diversify sourcing to relieve pricing pressure Build or strengthen customer loyalty programs, focusing on personalization, incentives, and a seamless omnichannel experience Focus on transparency in messaging while emphasizing value Adjust prices strategically and monitor consumer response | Analytics & Activation Brand & Media Consumer Behavior & Insights Market Measurement |

Manufacturers experience decreased pricing power as consumers lose capacity to absorb increases; basket compositions are reflective of pantry loading and/or bundling. | Consumers are at practical limits for price increases and are possibly experiencing stagnating or declining real incomes. | Audit portfolio to identify SKUs currently driving incrementality and those cannibalizing the brand Run elasticity-led promo testing across tiers Proactively manage higher-elasticity SKUs to deliver value; evaluate price-pack architecture; consider value tiers of innovation and/or mixed tier bundling | Expand multi-tier private label (value, mid-, premium) Use loyalty data to personalize value messaging and assortment | Analytics & Activation Brand & Media Consumer Behavior & Insights Innovation |

Value retailers and private label brands begin to see consistent and/or outsized growth. | Rising prices, a challenging labor market, and perceived high quality of private label products are empowering consumers to trade down or switch brands. | Protect margin in low-elasticity categories Prioritize core, low-elasticity SKUs for shelf presence and promotion Consider renovation to address new consumer needs or usage occasions, along with brand messaging focused on value proposition and unique features and benefits | Expand private label and value-tier adjacencies Shift space to high-turn, high-loyalty SKUs | Analytics & Activation Brand & Media Consumer Behavior & Insights Innovation Market Measurement |

Unemployment rate growing, approaching 5%. Consumers are shopping across retailer channels in search of value. | Income and consumer spending soften due to higher joblessness, lower job switching, and higher risk aversion. | Consider co-investment in EDLP (everyday low price/promo) for retailer alignment Right-size innovation pipelines to align with dynamic economy, focusing on brand defenders | Develop “essential buys” messaging to retain traffic Incentivize wallet consolidation (loyalty, app-based incentives) Emphasize basket-building promotions over category-deep discounts | Analytics & Activation Brand & Media Consumer Behavior & Insights Innovation Market Measurement |

Scenario: Soft landing

What to watch for

| Signals | Behavioral insights | Manufacturer actions | Retailer actions | How NIQ can help |

Consumer spending remains steady; sentiment on the rise. | Consumers are supported by a solid labor market and real wage growth, enabling stable (albeit intentional) spending. | Lean into value proposition and messaging, emphasizing features and benefits to drive brand loyalty | Strengthen symbiotic relationship between online and in-store, ensuring consistency of messaging; accessible product information/availability; and thoughtful recommendations, signage, and product filters | Brand & Media Consumer Behavior & Insights Market Measurement |

Inflation remains steady or declines, toward 2% target; gap between share of private label vs. branded products begins to shrink. | Increased price stability leads to stable demand and a returned focus on full value proposition (instead of price alone). | Rationalize SKUs that underperformed under pressure Reintroduce premium innovation for low-elasticity categories | Rebuild premium mix where loyalty remained Lean into curated discovery zones (seasonal, wellness, occasion-based) | Analytics & Activation Consumer Behavior & Insights Innovation Market Measurement |

Labor market holds steady, with unemployment below 5%; spending in “nice-to-have” categories on the rise. | Solid real income growth continues, supporting demand. | Invest in brand equity storytelling in direct-to-consumer and digital retail channels Test price lifts on loyalty-linked SKUs | Shift from deep discounts to personalized offers Use elasticity and promotional response data to refine promotion calendars | Analytics & Activation Brand & Media Consumer Behavior & Insights Market Measurement |

From enhancing brand perceptions to increasing market share and customer engagement, learn how NIQ is helping companies solve real-world challenges in unpredictable times.

Key takeaways:

Delaying key decisions or defaulting to the status quo in a rapidly shifting environment can lead to lost momentum, resources, and opportunities. Use data and thoughtful planning to direct your next move, keeping in mind lessons learned from economic shocks of the past.

Watching what matters

Today’s economic environment presents undeniable challenges for businesses. Shifting government policies and mixed economic indicators are forcing companies to rethink how they produce, move, and price their goods. But this looming uncertainty doesn’t automatically translate to a lack of consumer demand—especially for businesses that can adapt effectively.

Despite the noise, there are encouraging signals. Consumer behavior in times of stress tends to follow a predictable pattern: cutting back on discretionary spending while continuing to prioritize essentials. And at the time of this analysis (summer 2025), NIQ consumer data shows no widespread signs of consumer stress behavior emerging.

That said, this is not a moment for complacency. It’s a time for vigilance, preparation, and precision. As we learned in the aftermath of COVID-19, consumer sentiment and consumer behavior don’t always align. While consumers may express concern about inflation or economic uncertainty, their actual purchasing patterns often tell a different story. Overreacting to sentiment—rather than behavior—can lead to premature or excessive business responses.

“This is not a moment for complacency. It’s a time for vigilance, preparation, and precision.”

The key is to not overcomplicate the landscape. The question isn’t how consumers will respond to every possible scenario—it’s whether their behavior is exhibiting signs of stress or not.

To stay ahead, companies must monitor the right data. While key government indicators can shed light on what happened in the past and what to watch out for, they lack the immediacy and detail necessary to fully empower agile decision-making.

NIQ can help bridge the gap with real-time consumer intelligence, enabling businesses to detect early signals and pivot with confidence. With the right insights, businesses can move from reactive to resilient, prepared to not just weather change—but to lead through it.