Launch Fast, Learn Faster: Are you reading the early signals before your product launch falls behind?

Why accessing Early Innovation Performance matters for Brands and Retailers.

Across Europe, the innovation engine is running faster than ever. New products are launched every day, competition for physical and digital space is intensifying, and both brands and private labels are moving fast to capture increasingly fragmented consumer needs.

In 2025 alone, more than 3,500 new brands and sub‑brands were launched across the United Kingdom, Germany, France, Italy and Spain. Yet, only one third of them were able to reach 1% of households.

In a context where assortment is under pressure and activation windows are tightening, retailers must make harder decisions, faster — while manufacturers face a shrinking opportunity to prove that a new product truly resonates with consumers and deserves to stay. Still, areas of opportunity and growth remain amid this emotional battleground. In this analytical assessment of the state of consumers, we’ll help equip you to win with cautious yet hopeful consumers over the next 12 to 18 months—and beyond.

It is clear that accessing early performance matters more than ever.

The first months of a launch reveal whether a product is building the momentum, credibility, and category value it needs to grow — or whether it will quietly fade into the background.

This three‑part analysis explores the early‑stage indicators that matter most for FMCG product launches across five European markets:

- Consumer acceptance — are shoppers not only trying, but coming back?

- Consumer sentiment — what are early adopters really telling you?

- Incrementality — are you adding value, or cannibalising your own brand?

Powered by our integrated and robust NIQ Consumer Panel data*, this analysis provides category‑specific benchmarks to give manufacturers and retailers a practical, evidence‑based framework to quickly diagnose whether a launch is performing as expected and build the foundations for sustainable growth.

Chapter 1: Consumer Acceptance

Not all products scale at the same pace, and repeat curves can hide big differences.

By analysing the first months of 2025 launches, we identified clear, category‑specific trial and repeat benchmarks across the United Kingdom, Germany, France, Italy and Spain. These early indicators are critical to guide launch decisions and demonstrate credibility with retail partners.

Want to read more?

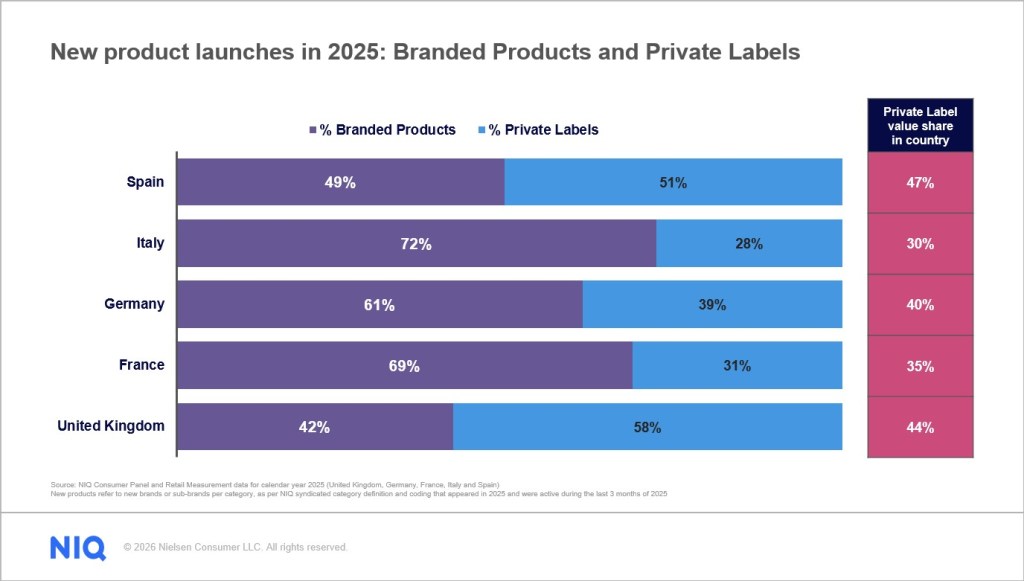

France

In France, Food dominates new product launches, with both Branded and Private Label activity heavily concentrated in Everyday and Confectionery & Snacks. However, the sheer volume of innovation in Ambient Food and Snacks makes it harder to drive both trial and repeat. While reaching 1% household penetration in the first year is achievable, only around 30% of launches get there. Perishable Food stands out, with 37% breaking through despite intense competition. Beyond trial, repeat is where categories truly diverge: Pet Food, Perishable Food and Beverages perform strongest, while Confectionery & Snacks struggle to convert experimentation into lasting loyalty.

While reaching 1% household penetration in the first year is achievable, only around 30% of launches get there.

The average new launch nearly reaches 1.5% household penetration in year one, and over half of launches surpass the 1% threshold.

Germany

In Germany, Food still dominates innovation, but priorities vary by brand type. Branded launches focus more on Confectionery & Snacks and Personal Care, while Private Labels concentrate on everyday Food, with Non‑Alcoholic Beverages emerging as a key battleground for both. Germany also shows stronger reach potential than other markets: the average new launch nearly reaches 1.5% household penetration in year one, and over half of launches surpass the 1% threshold. Home Care and Non‑Alcoholic Beverages scale fastest. Among successful launches, Non‑Alcoholic Beverages and Perishable Food build both trial and repeat most quickly, while Home Care enters households fast but develops repeat more slowly due to lower purchase frequency.

Italy

In Italy, Food remains the core of innovation, though focus shifts by brand type, with Branded Products also investing strongly in Health & Beauty. Achieving scale is possible, but performance varies by category. The average new launch slightly exceeds 1% household penetration in its first year, and around 30% of trialists repeat at least once. Nearly half of launches reach the 1% penetration threshold, with Home Care standing out as the most successful at scaling. Among launches that break through, Ambient Food, Perishable Food and Home Care drive faster trial, but repeat is more challenging in Ambient Food and Home Care, limiting longer‑term loyalty.

The average new launch slightly exceeds 1% household penetration in its first year, and around 30% of trialists repeat at least once.

The average new launch reaches around 1.5% household penetration in the first year, and two‑thirds of launches surpass the 1% threshold.

Spain

In Spain, new product launches show a balanced activation across categories, with clear winners emerging. Branded activity skews slightly toward Home Care and Confectionery & Snacks, while Private Label is more active in Health & Beauty. Spain stands out for its ability to scale: the average new launch reaches around 1.5% household penetration in the first year, and two‑thirds of launches surpass the 1% threshold, led by Confectionery & Snacks. Here, fast trial and strong repeat reinforce each other—Confectionery & Snacks is the only category over‑performing on both. In Non‑Food, Home Care delivers exceptionally rapid penetration while also retaining over 37% of trialists, highlighting strong early momentum and loyalty.

United Kingdom

In the UK, Food continues to dominate new product launches, but with a clear split between Branded and Private Label strategies. Branded launches skew toward indulgence and Personal Care, while PL activity concentrates on everyday meal and cooking categories. Scale remains the exception rather than the norm in a highly crowded market: only one in four launches reaches 1% household penetration. Less crowded categories such as Health & Beauty, Home Care and Paper Products show a more polarized pattern, with fewer launches but a higher likelihood of breaking through. While routine categories drive faster trial, they struggle to generate repeat, whereas less activated or more niche categories recruit more slowly but convert trial into loyalty more effectively.

Only one in four launches reaches 1% household penetration in the United Kingdom.

Want to read more?

Chapter 2: Consumer Sentiment

What happens after consumers try your innovation? And more importantly, why do they come back – or not?

In the first chapter of Launch Fast, Learn Faster, we explored how penetration and repeat rate signals whether a launch is gaining traction. However, this only tells what is happening, but not why. To truly understand a product trajectory, manufacturers need to know what consumers think, feel and expect after their first experience.

Drawing on 15 years of NielsenIQ New Product Alert data and more than 54,000 interviews with verified buyers across the United Kingdom, Germany, France, Italy and Spain, this Report uncovers the consumer sentiment factors that separate successful launches from the rest.

Key Takeways

From the drivers of trial and repeat purchase to the growing importance of satisfaction, value and meaningful differentiation, the findings reveal why some products convert curiosity into loyalty while others struggle to gain momentum.

- Only 1 in 3 launches reaches 1% household penetration, and only 17% combine strong trial and repeat purchase.

- Innovation attracts attention, but satisfaction drives growth. While 40% of consumers purchase a new product because they want to try something new, overall liking, quality and value for money are much stronger predictors of future repurchase than novelty alone.

- Generating trial is only half the battle. Although 76% of trialists claim they would buy a product again, actual repeat rates are typically much lower, highlighting the importance of benchmarking consumer sentiment against real-world behavior.

- Small shifts in consumer sentiment can signal major differences in performance. The strongest launches are more likely to meet or exceed expectations, resulting in significantly higher repeat purchase rates over time.

- The innovation bar continues to rise. European consumers increasingly seek products that feel genuinely new and different, yet fewer launches succeed in standing out, making meaningful differentiation more important than ever.

Download the Full Chapter 2 European Report to discover the consumer signals that can help you identify opportunities, address barriers to repeat purchase and maximize innovation success before it’s too late.

Not all innovations are the same.

Do you want to access the early performance of your innovations with confidence, or gain strategic insights to plan the next one?