A welcome from Julian Baldwin

Consumers are at a juncture. They’re still cautious about their spending amid lingering economic uncertainty, but they are spending on certain technology products. What they want is compelling value for their money.

So what is this value? When it comes to household appliances, our research shows that consumers are interested in durable products that make their lives easier. They’re looking for appliances that deliver increased convenience, multifunctionality, energy and water savings, and/or enhanced health and well-being benefits. They notice the value when these benefits are clear.

For the Household Appliances sector in 2026, there are strong opportunities for manufacturers and retailers to meet these consumer needs—even amid slow economies. They must get the feature sets and pricing right, especially as challenger brands drive assertive market expansion.

This report looks at the most lucrative home appliance market trends in 2026, analyzing where manufacturers and retailers should focus their product assortment, innovation, and marketing investments. Throughout, we draw from NIQ’s in-depth analysis of Consumer Technology and Durable Goods (T&D) sales data, as well as trends in consumer behavior and aspirations—revealing strategic, actionable insights.

We hope that these insights strongly enhance your view of the buyer journeys and sector purchasing behaviors that lie ahead.

President, Global Tech & Durables, NIQ

President, Tech & Durables, and Head of Global Commercial Negotiations

Julian Baldwin leads NIQ’s Global Tech & Durables business, managing the world’s most robust point of sale (POS) tracking network, and global, long-term panel studies. His team partners with clients to deliver the data-driven insights needed to help them understand their market, brand, and consumer better than ever. In addition, Julian leads NIQ’s Global Commercial organization, managing commercial negotiations and pricing for NIQ’s largest global clients.

Want to read later?

Chapter 1: 2025 full-year projection

Manufacturers and retailers are still facing headwinds with changes to US tariffs during 2025 disrupting planning, on top of still-fragile consumer confidence across many markets.

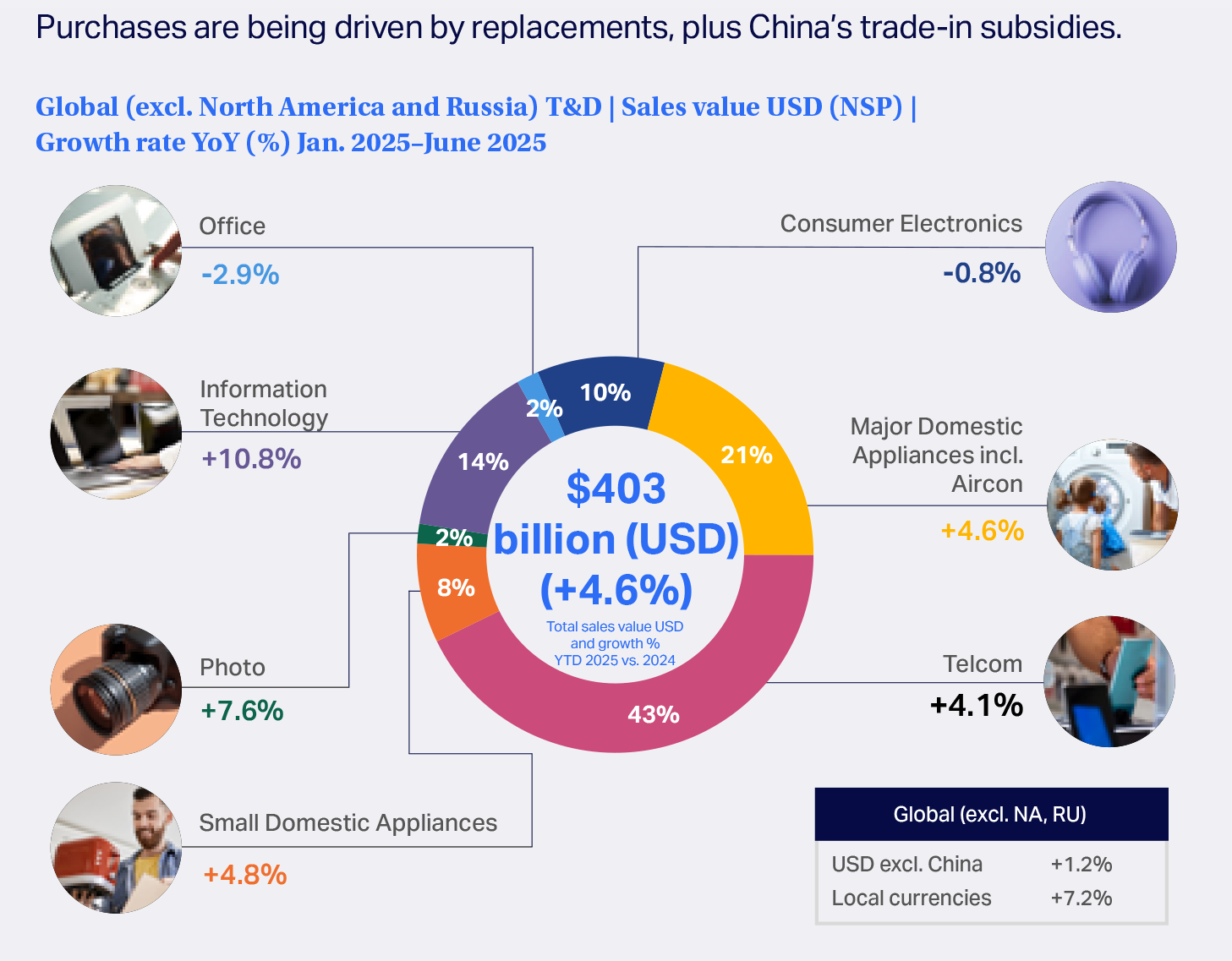

Nevertheless, in the first half of 2025 (H1 2025), sales of Consumer Technology and Durable Goods (T&D) grew 4.6% in value year over year. That increase—to $403 billion (US dollars)—was largely driven by activity in China due to retail “trade-in” policies that cut replacement costs for consumers in key product groups. With China removed from the analysis, global sales increased by a more gradual 1.2%.

Consumer Tech and Durables Goods global market returns to growth

Electronics includes Multifunctional Technical Devices, Small Domestic Appliances includes Personal Diagnostics)

Our analysis shows that global sales volume remains relatively flat so far (+1%), but sales value is up 5%. This shows a landscape where consumers aren’t buying more T&D goods than before, but they are spending more per item, where they see compelling offers.

This holds true for small domestic appliances (SDA); however, major domestic appliance (MDA) categories are the exception. Here, price pressure is still strong in many categories and markets (especially developed markets, like Europe). When it comes to MDA purchases, consumers are still focused on saving money and are leaning toward products that offer core features (e.g., energy efficiency, capacity, and convenience) at the most attractive price—even if it requires switching brands.

“Relevant features—from convenience to smart energy efficiency—and savvy pricing will be critical to sales growth in home appliances. It must be positioned so consumers can clearly see the benefit that a product’s features bring to their lives.”

—Frank Landeck, Global Tech & Durables Lead, NIQ Next

By the end of 2025, NIQ projects 2% year-over-year value growth for global Consumer Tech and Durable Goods (T&D) sales, driven by China, Emerging Asia, Eastern Europe, and the Middle East & Africa—and with household appliances playing a significant part in that growth.

Key takeaways

- Global sales of Consumer Tech and Durable Goods (T&D) grew 4.6% in H1 2025, year over year.

- For full-year 2025, NIQ predicts value growth of 2% globally, bolstered by replacements, China’s trade-in policies, some improvement in global macroeconomics, and demand in emerging markets and Eastern Europe.

- Price remains important but is not the only factor. Consumers are choosing products that present value for money—and manufacturers and retailers can capitalize on that.

Chapter 2: Macro forces shaping home appliances 2026

Six key macroeconomic and business-related forces will impact the household appliances sector in 2026:

- Chinese brand growth outside China

- Evolving US tariffs

- Chinese trade-in program

- Replacement cycles

- Gen X purchasing behavior

- Home country manufacturing

This chapter examines the scope and implications of each.

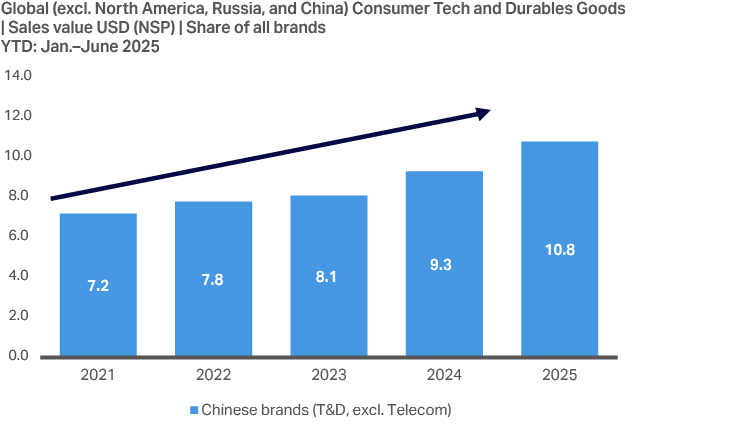

Force #1: Chinese brand growth outside China

China has been investing in establishing stronger distribution in markets such as Saudi Arabia, the United Arab Emirates (UAE), Southeast Asia, Latin America (LATAM), and Europe. A prime example is China’s investment in the Chancay port in Peru, opening a faster, cheaper trade route for Chinese goods to enter LATAM countries.

Their ability to present products with strong feature sets at attractive prices, and the fact that they lead the market in SDA innovation and R&D investments, means Chinese brands have increased their share of sales across consumer tech, including household appliances.

In 2026, this expansion will grow as Chinese brands look to replace revenue lost in the US market due to tariffs.

Chinese brands are steadily expanding their market share internationally

In the small home appliances sector, Chinese brands have been leading the market in terms of product innovation, and thereby commanding premium prices—especially in areas such as vacuum cleaners, electric fans, and air treatment.

Within major home appliances, Chinese brands have quietly been growing brand recognition in key markets via attractive pricing. Having used this approach to build overseas consumer trust in the quality of their products, Chinese brands are now expanding into more premium price ranges. Overall, Chinese MDA brands are outperforming others in terms of growth—especially in Central and Eastern Europe, LATAM, and Western Europe.

Chinese brands have quietly been growing brand recognition in key markets via attractive pricing.

Force #2: Evolving US tariffs

As retailers clear the stock that they brought in ahead of US tariffs coming into effect, we will start seeing the impact of those tariffs on manufacturers and retailers really taking hold.

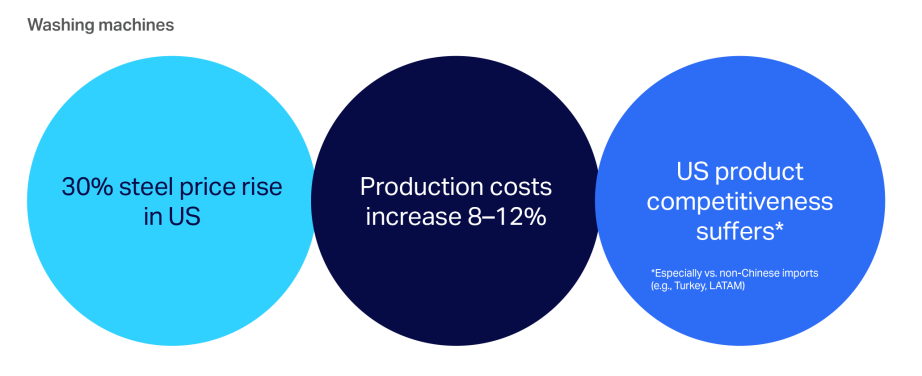

The major household appliances sector will feel the greatest impact due to the deepening of steel-related tariffs. Before June 23, 2025, US levies included a tariff of 50% on the import of raw steel. However, this had a negative impact on production costs for American-made MDA, such as washing machines, dishwashers, and ovens.

Impact of US steel tariff on US manufacturing

In late June 2025, the scope of the steel levies expanded to include a 50% tariff on the “steel equivalent” contained within imported appliances, including freezers, fridge-freezers, washing machines, dryers, dishwashers, and ovens.

In the remainder of 2025 and throughout 2026, these changes will provide a more level playing field for US manufacturing, eliminating disadvantages to US manufacturers versus MDA imports. However, as a result, US consumers will have to pay extra for these products—whether US made or imported—as happened when US steel tariffs were introduced in 2018. In a recent interview, the CEO of Michigan-based manufacturer Whirlpool estimated the new tariffs could increase the retail price of imported appliances by $50 to $70, potentially swaying consumer purchasing decisions.

Tariffs are especially challenging for brands that have a high proportion of US sales within their total revenues. These manufacturers and retailers are likely to rethink their supply chains, although these efforts can be complex, take a long time to set up, and be quickly negated by subsequent policy changes. Because the US market is too big for brands to simply deprioritize it, all major overseas brands will continue to sell in the US—despite the decreased demand that will likely result from rising prices. However, these brands will also look to expand their reach in other markets to offset the likely fall in US revenue. We will therefore see increased competition in markets such as Europe, Southeast Asia (SEA), and LATAM in 2026 and beyond.

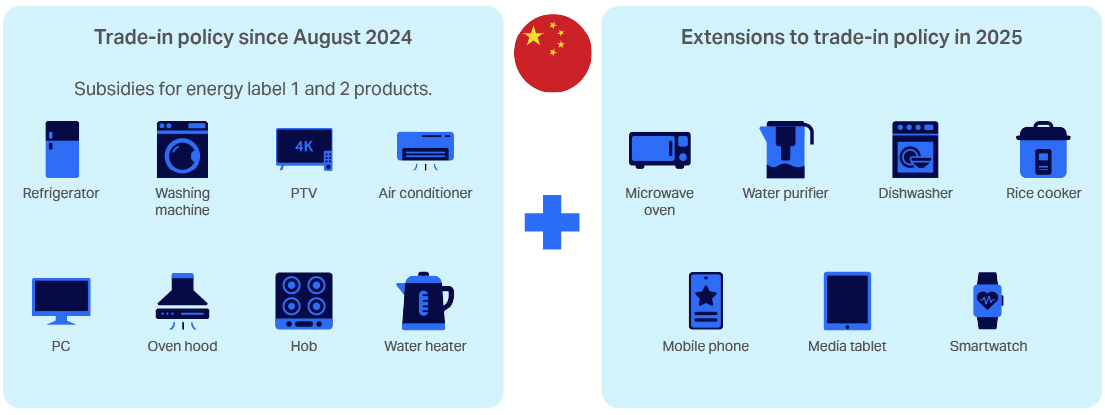

Force #3: Chinese trade-in program

China’s trade-in program for consumers’ household appliances is expected to have an ongoing impact in 2026.

China’s trade-in and subsidy policy: Categories included.

The subsidies boosted sales of key categories in China in H1 2025, but at a lower level than seen in H2 2024, when consumers first rushed to take advantage of the new offer. With the policy now expected to continue through the remainder of 2025, China’s consumers may not sense urgency. But there will likely be a purchasing spike in December 2025 as people rush to buy ahead of the speculated end date.

The end of this policy will have a substantial impact once it takes effect. If the policy concludes at the end of 2025, we believe sales of appliances within China will drop precipitously in 2026—with premium products being most affected. If the subsidies extend into 2026, we expect a very moderate sales impact since so many consumers have already replaced appliances that were most in need of an upgrade.

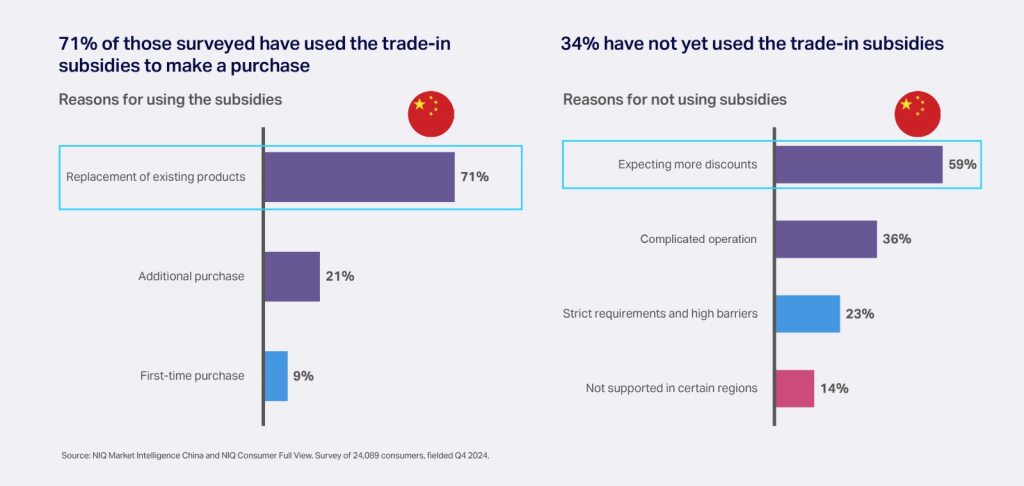

“Within China, awareness and take-up of the trade-in program is high, with the majority using it to replace existing products. However, one-third of those we surveyed have not yet made use of the program—either finding the process too complicated or hoping for greater discounts later in the year.”

—Nevin Francis, Senior Director, Global Strategic Insights, NIQ

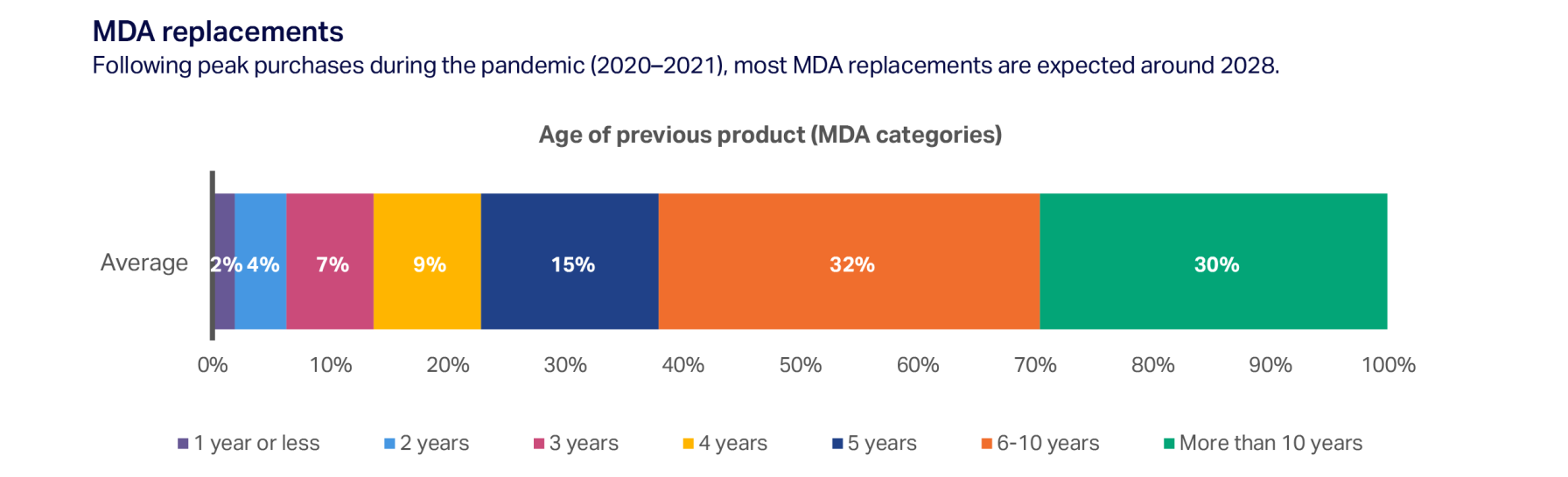

Force #4: Replacement cycles

In 2026, there will be a contrasting picture for replacement cycles between major and small home appliances.

For major domestic appliances, the average replacement cycle is eight to 12 years, so peak replacements (following pandemic-era purchase spikes) aren’t expected before 2028. MDA purchase activity in 2026 will instead be driven by people replacing faulty products and by first-time buyers.

“Consumers are holding onto major appliances longer—driven by cautious spending and a lack of compelling innovation. Sales for upgrades are down, while replacements for broken units are up. Manufacturers and retailers must adapt their strategies to counter this shift.”

—Frank Landeck, Global Tech & Durables Lead, NIQ Next

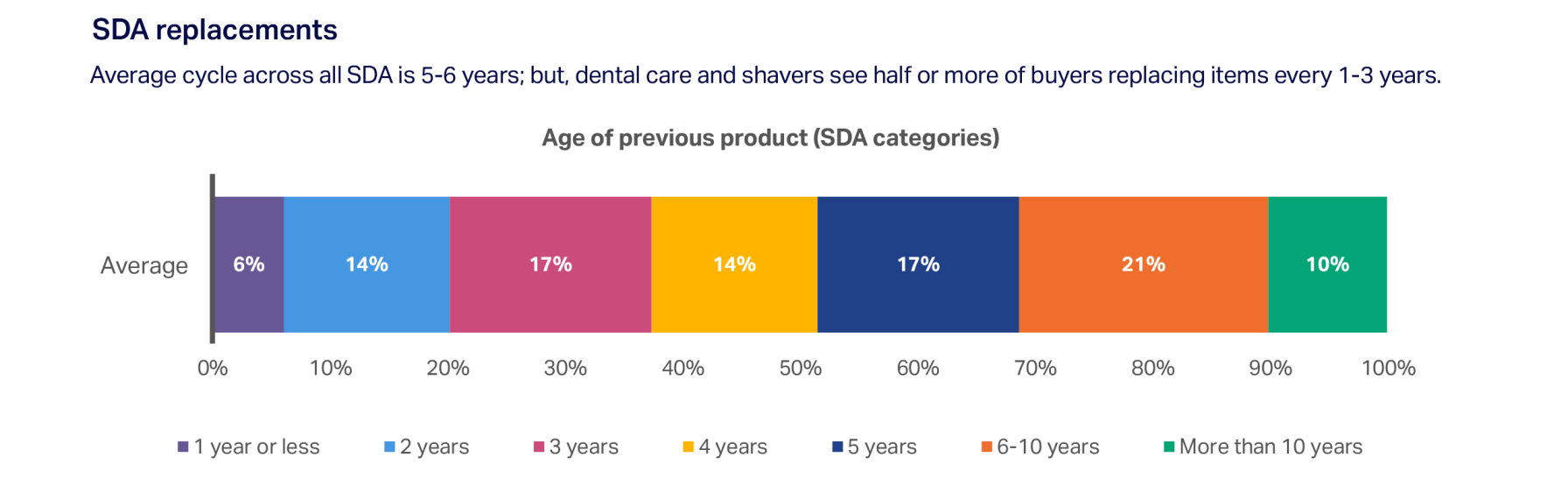

By contrast, replacement cycles are shorter (averaging five to six years) for small domestic appliances such as hair dryers/stylers, hot beverage makers, food preparation appliances, electric toothbrushes, and vacuum cleaners. Peak replacements of pandemic-era purchases are already kicking in. Demand has also been enhanced by the overall affordability of SDA products improving as recent innovations are commoditized. This is enabling more consumers to upgrade to more premium appliances—even before their current ones need replacing.

Force #5: Gen X purchasing behavior

Gen X (now ages 45–60) is the new highest-spending consumer segment, quietly driving trillions in consumer purchases. In 2025 alone, Gen X is set to spend $15.2 trillion globally on retail purchases—and, within a decade, their annual spending will reach $23 trillion.

Gen X is a prime audience for both major and small household appliances, with many members being time-pressed “caretaker consumers” who are responsible for—or heavily influencing—the home appliance purchases of aging parents and young-adult offspring, as well as their own household.

In terms of the appliances they buy, Gen Xers are more likely than others to place importance on products that are durable, high quality, and make their lives easier, as well as those offering energy savings. (NIQ’s Consumer Life 2025 survey reveals that 79% of Gen X consumers say they conserve energy at home all or most of the time.)

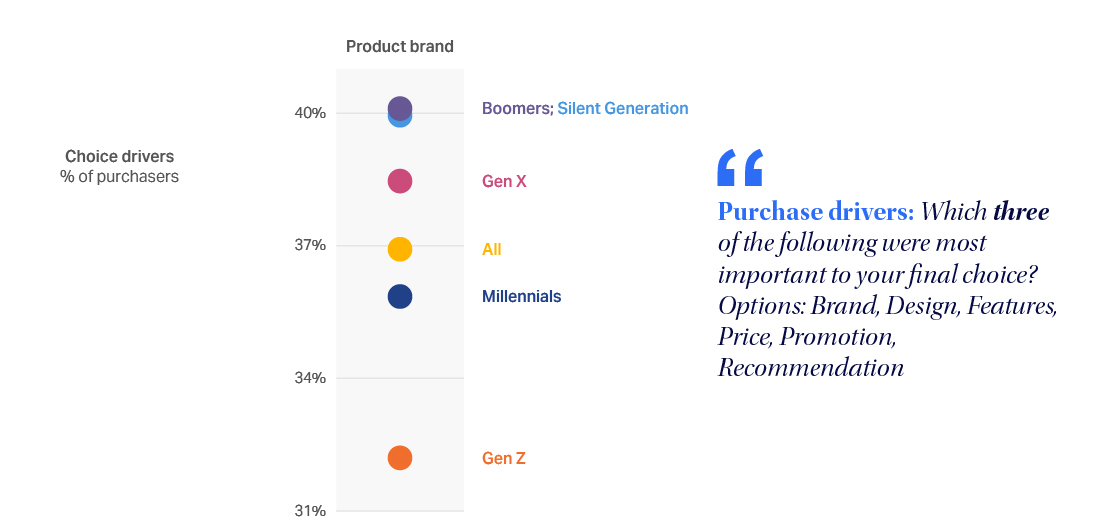

A key finding is that brand is more important with Gen Xers than it is with all younger generations—something that manufacturers should really focus on at a time when competition from new brand entrants is at an all-time high.

Manufacturers and retailers truly must have Gen X in mind when shaping their 2026 strategies, or they risk missing the mark with a highly profitable cohort.

25% of Gen X buyers in select markets spent over $650 on a washing machine, while only 17% of Gen Z did

Source: NIQ gfknewron Consumer: Austria, Belgium, Brazil, Chile, France, Germany, Great Britain, Italy, Japan, Netherlands, Poland, Spain, Türkiye, Washing machine sales, MAT Q125 (April 2024—March 2025)

Brand holds more influence on older generations in their MDA purchases; Gen Z is less brand-driven in their choices

Force #6: Home country manufacturing

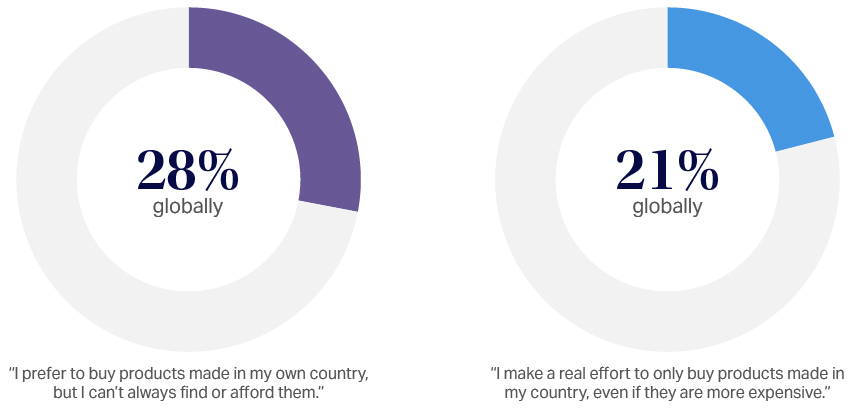

Consumers’ focus on the “made in” label is increasing, pointing to an emerging opportunity for home appliance manufacturers.

Globally, half of consumers state that they prefer to buy products made in their own country. However, a large percentage of those say they can’t always find or afford them, presenting an opportunity for brands. This opportunity is greatest in Western Europe and Developed Asia, where the number of consumers saying they prefer to buy products made in their own country (but can’t always find or afford them) jumps to nearly 40%, compared with the global average of 28%.

While this is currently more of a focus for groceries and fashion products, politicians and media in 2025 are increasingly highlighting the need to support domestic economies and jobs. Global home appliance brands that can market themselves as manufacturing items in the country of sale, while also offering good product features and price, can differentiate themselves in crowded landscapes in two ways—as supporting the local economy and as reducing delivery miles.

28% globally

“I prefer to buy products made in my own country, but I can’t always find or afford them.”

21% globally

“I make a real effort to only buy products made in my country, even if they are more expensive.”

Source: NIQ Consumer Life 2024, Global (18 core countries)

Key takeaways

- Domestically, China may see a significant sales drop for home appliances in 2026 unless trade-in subsidies are extended.

- Chinese manufacturers will continue to quickly enter global markets outside mainland China, capitalizing on the distribution they have built up over the past few years, as well as expanding into new and more premium sales channels.

- Globally, consumer replacement cycles won’t kick in until at least 2028 for most MDA. However, SDA sales will continue to experience an uplift, driven by commoditization of innovative features.

- Gen X has become a hugely valuable customer segment that’s willing to pay a premium for durability, quality, and convenience—and placing importance on brand.

Unlock premium chapters on Product innovation; Retail trends; Global takeaways; Regional outlooks: Enter your details to continue reading

Chapter 3: What will drive demand for home appliances in 2026?

Consumer perception of value

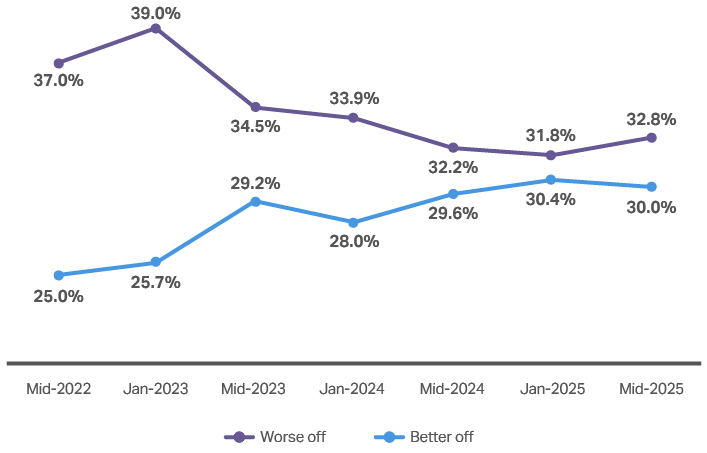

Consumers’ desire for value will be critical to how manufacturers and retailers grow their sales in 2026. Value perceptions are increasingly important, driven by consumers’ sentiment around their household finances remaining cautious. Globally, 32.8% felt worse off in their household finances in mid-2025 compared with a year prior—a percentage point increase from the start of the year—while 30% felt better off.

Note: In China, verbiage reflects change in “management of spending.”

1 Consumer Life 2025, Global

In this landscape, 60% of people consider value for money to be the most important factor a brand can offer.1 Price remains a priority in the purchase decision but, when it comes to getting value from a product, the top three most important factors are durability, high quality, and making life easier.

“Consumers, especially in the Western hemisphere, are increasingly looking at feature sets rather than brand within the Major Domestic Appliances sector. They want everything from energy efficiency and sustainability to convenience—presenting a clear opportunity for smart, AI-enabled, and multifunctional appliances.”

—Norbert Herzog, Head of Global Strategic Insights, NIQ

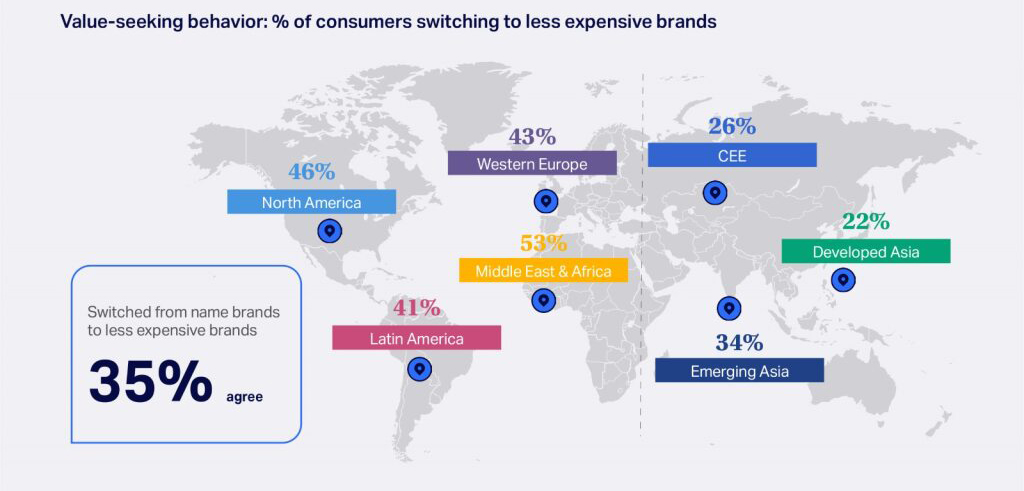

Being a trusted brand is still important, but consumer priorities are changing. Their growing prioritization of value over brand is enabling challenger brands to gain increased share in western markets through attractively priced products boasting strong functionality and feature sets. Over 40% of consumers in North America, LATAM, and Western Europe say they have switched to less expensive brands in the last year, rising to over 50% in the Middle East & Africa.

Product innovation

In 2026, manufacturers and retailers will need to satisfy consumer value demands with compelling, affordable innovation. For domestic appliances, the most notable developments will be around smart ecosystems, convenience, sustainability, and health and beauty.

Smart home ecosystems

While there’s enormous potential for AI functionality in domestic appliances, the concept remains a manufacturer push—rather than a consumer focus—at present.

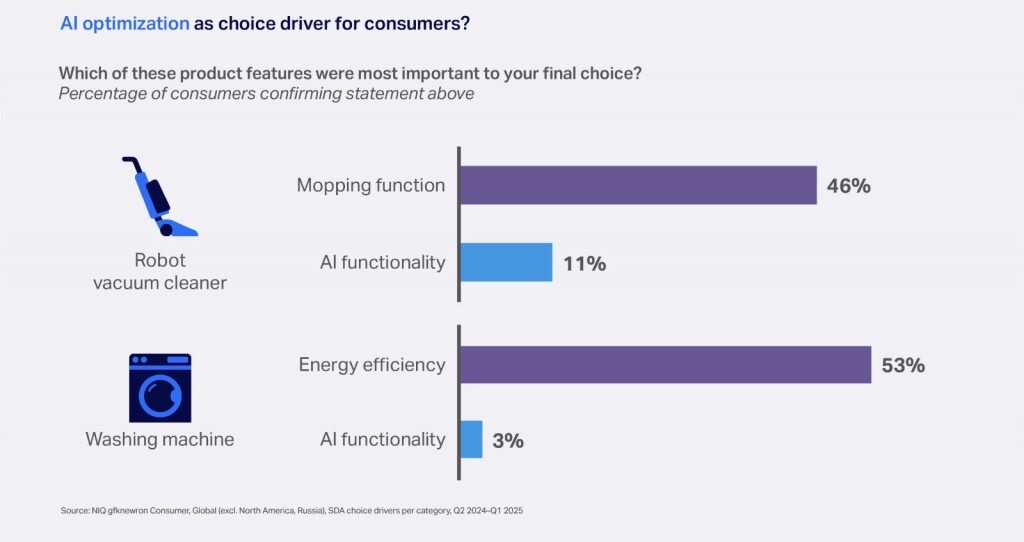

Even among robot vacuum buyers, only 12% say that AI functionality was important in their product choice, compared with 46% who bought it for the mopping function. With washing machines, AI functionality was a deciding factor for just 7% of buyers, while energy efficiency mattered to 53%.

However, if we consider how AI helps improve robot vacuum algorithms for navigation and mopping, or how it aids washing machine energy efficiency by means of pattern recognition and enabling sustainability dashboards, it becomes clear that AI is an enabler for what consumers consider to be their top purchase drivers.

We therefore expect consumer interest in certain smart products to increase strongly in the long term, as they better understand the very relevant benefits that AI functionality delivers.

Manufacturers must remember that consumers are motivated by convenience, performance, and energy savings, rather than by smart tech itself.

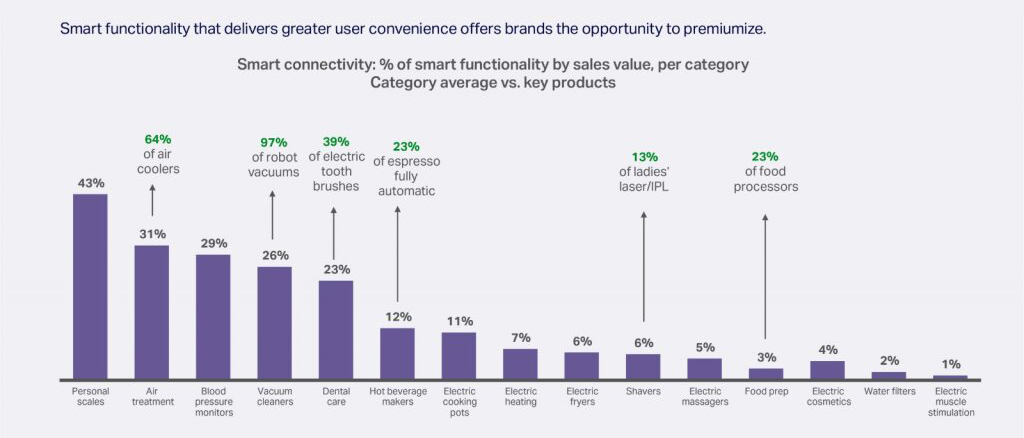

For small domestic appliances, AI-powered functionality will succeed wherever there is a compelling use case. These include:

- Robot vacuums that recognize different floor types and dirt, automatically switching between vacuum, mop, or steam clean, and having the ability to recognize different obstructions and move items out of their way

- Electric toothbrushes that monitor teeth and gum health and alert the user to developing mouth conditions

- Air conditioning units that balance whole-house efficiency by continuously learning the household’s room usage patterns

- Multifunctional food processors and cooking pots that recognize different food types and automatically trigger optimal settings that match individual users’ preferences

Smart connectivity growing in SDA categories where use cases are relevant

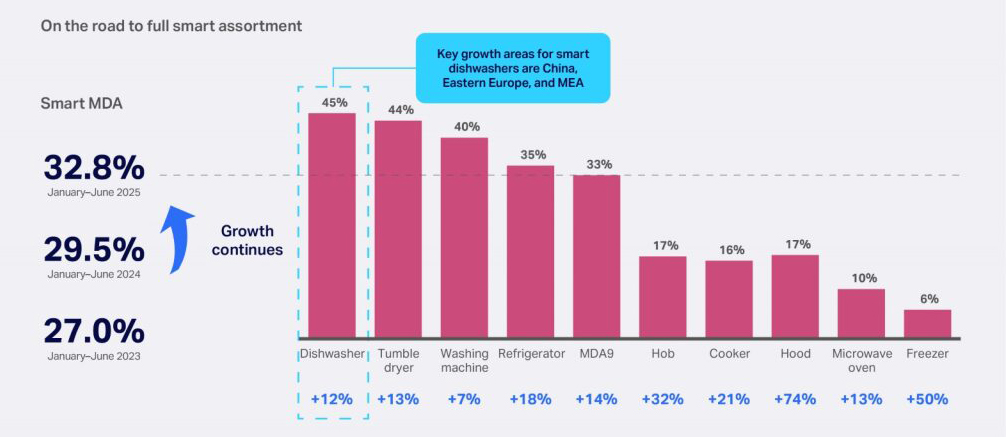

In major domestic appliances, AI functionality still lacks clear consumer pull. Even in dishwashers, where smart devices now account for 45% of sales value globally, consumers are often not choosing the machine for its AI capabilities. However, AI functionality is the enabler of many of the conveniences that are important to consumers, such as automatic selection of the optimal wash cycles or noise reduction.

For manufacturers and retailers to drive smart appliance sales, they must promote the benefits the AI capabilities deliver that resonate with that audience, rather than the technology itself. This means a focus around performance, making life easier, and energy/water/resource savings.

Smart appliances sales reach new record levels as key brands push new assortments

Within MDA, smart connectivity will deliver its maximum value when consumers install an ecosystem of appliances that work together. While this will take some years to achieve (due to long replacement cycles in MDA), we project that the strongest opportunity for AI innovation will be within the cooking space, where smart ecosystems can democratize culinary skills and present a personalized experience. Imagine the interplay of an AI refrigerator, oven, hob, and hood creating a smart kitchen that will tell you what recipes can be cooked from the ingredients available in the kitchen, talk you through the step-by-step preparation, and automatically set appliances to the optimal settings for that meal. Such a setup introduces radically new and relevant benefits into consumers’ lives.

“The biggest smart opportunity for MDA is in AI-assisted ovens, hobs, and hoods—democratizing the art of cooking and making it gratifying and personalized. Looking ahead, manufacturers will need to achieve proper interoperability to unleash the full potential of home ecosystems.”

—Norbert Herzog, Head of Global Strategic Insights, NIQ

People will increasingly buy based on product capabilities rather than form. Brand focus must be on multifunctional products that deliver convenience, performance, versatility, and space savings.

Convenience and performance

In both small and major household appliances, innovation in 2026 should focus on delivering convenience and performance—often via multifunctional appliances.

Convenience covers a range of areas:

- Saving space is a growing demand worldwide, but especially in countries such as Japan, China, and the major LATAM countries with high population density in urban areas, which often correlates to smaller living spaces.

- Innovation that drives resource conservation (e.g., energy/water efficiency, auto-dosing to reduce detergent use) remains in high demand, delivering money savings in the long term, as well as meeting people’s desire to be increasingly eco-friendly.

- Multifunctionality brings added value by delivering versatility, as well as space and money savings from one product doing more. Manufacturers can therefore charge a premium for the added value these products deliver.

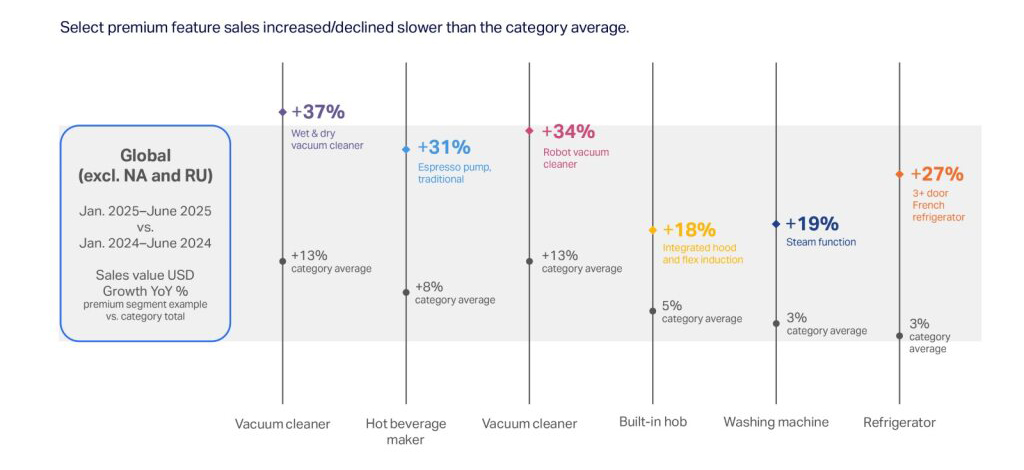

Demand for convenience and higher performance will continue in 2026 and beyond. We expect products offering these benefits to continue to outperform their category, as we are already seeing with wet and dry vacuum cleaners, robot vacuum cleaners, pump espresso makers, built-in hobs with integrated hoods and flex induction, washing machines with steam cleaning functions, and three-door (or more) French refrigerators that offer more capacity and flexibility.

“Value” justifies high growth for innovative segments

Manufacturers and retailers will need to focus on multifunctional products that deliver convenience, performance, versatility, and space savings. Where convenience goes hand in hand with eco-friendly benefits (e.g., no-pod coffee makers that are both sustainable and more convenient for the user), this presents a very strong consumer offer.

“Hybrid and multifunctional products are surging in popularity. For the consumer, this reduces the need for multiple products. For the manufacturer, it provides a rationale to charge premium pricing for the added value of versatility.”

—Nevin Francis, Senior Director, Global Strategic Insights, NIQ

Sustainability and circularity

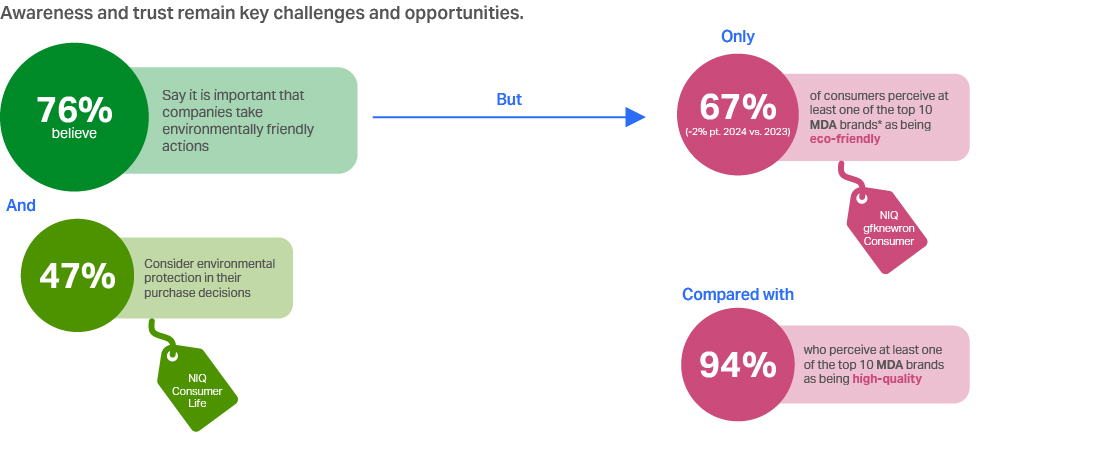

As of this year, 45% of consumers say they consider environmental protection when making their purchases. What’s more, increasing numbers of consumers now fall into the NIQ consumer segment “Green inDeed”—shoppers who are most active in turning their environmental aspirations into action.

In 2024, 21% of global consumers were “Green inDeed”—up seven percentage points from 2022. The “Jaded” cohort—those skeptical about sustainability and climate change—stood at just 13% of global consumers.

Rise in “Green inDeed” consumers: Most active in environmental action as well as aspiration

Manufacturers must focus on demonstrable sustainability—from sourcing and packaging to energy efficiency and repairability.

That said, sustainability isn’t always the leading influence on consumers at the actual point of purchase. Other factors can overtake it—including price, performance, features, and availability. Brands must balance high performance with well-evidenced sustainability to successfully reach the maximum number of consumers. This may mean offering best-in-class energy efficiency and durability and/or repairability, alongside high-end dashboards that track daily use and make eco-saving recommendations.

Energy efficiency is a stronger purchase motivator in major than small home appliances, as more than 90% of lifetime energy consumption of MDA products happens during usage, rather than production. In 2026, energy efficiency will continue to be the leading purchase driver for MDA shoppers, combining the personal benefit of saving money on electricity with acting sustainably.

Repairability and circularity are also becoming more important, bringing both sustainability and money-saving benefits to consumers. The expectation is that France’s mandatory “repairability index” will soon be adopted across the EU, augmenting the European Parliament’s existing Right to Repair directive.

When it comes to refurbished domestic appliances, the market will take some years to gain traction: Products will need to be designed for circularity first, increasing their durability and repairability to extend their usable lifetimes, and then the opportunity for refurb will become a real opening.

For small household appliances, the eco focus will continue to be on recycled or recyclable materials and packaging, as well as reducing consumption waste—such as soda makers with refillable cylinders or no-pod coffee makers.

Sustainability is a much weaker buying criterion for SDA than MDA

But it is steadily growing in various forms across various SDA categories.

Although T&D manufacturers are investing in eco factors, there’s a disconnect between those efforts and how consumers perceive these brands. When presented with a list of the top 10 MDA brands in their country, one-third of consumers felt that none of them is known as being eco-friendly. Compare that with the 94% who felt that at least one of the brands was known for being high quality, and it’s clear that T&D manufacturers have a long way to go to build up recognition of their brand’s eco credentials.

Consumers expect companies to take environmentally friendly action, but most MDA brands are not yet recognized as being eco-friendly

To differentiate themselves, manufacturers must focus on promoting demonstrable sustainability across the full life cycle of their products—from sourcing of raw materials and construction to packaging and delivery and the product’s energy efficiency, durability, repairability, and recyclability. This is particularly important in mature markets where competition is high, and where a significant percentage of key consumer segments have the disposable income to make premium purchases that support their values around sustainability.

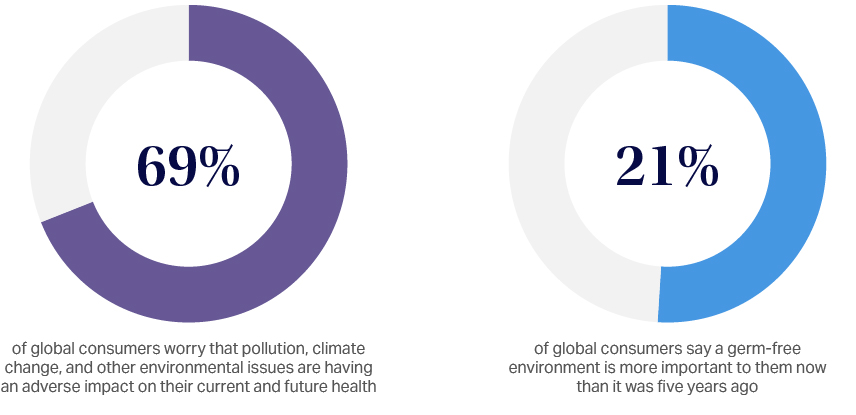

Health, hygiene, and climate change

Health, hygiene, and climate change will continue to be important purchase drivers for consumers next year, including in markets with weaker discretionary spending.

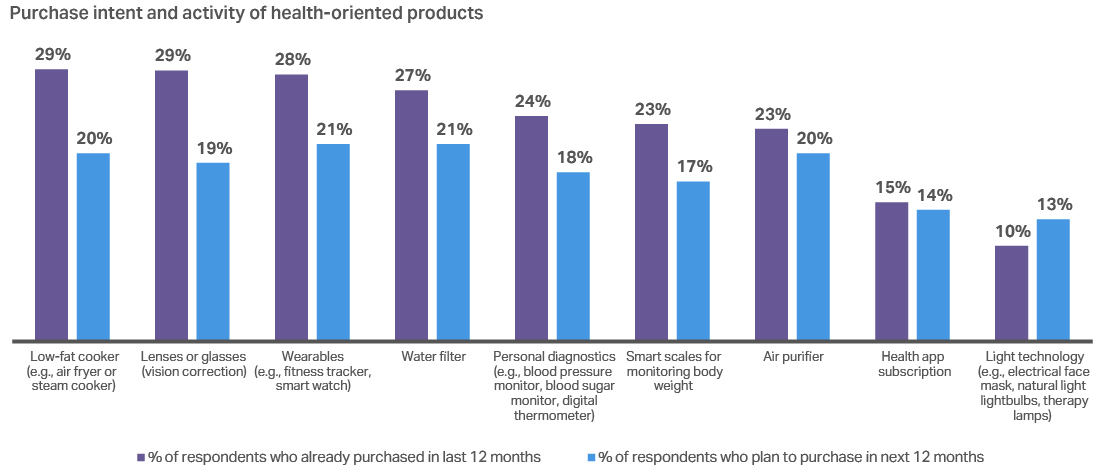

Consumers are increasingly informed on health issues—both physical and mental—and are increasingly focusing on making changes now to ensure a healthier future. With many health tech products becoming more affordable, demand is accelerating for items from air fryers and water and air purifiers to vacuum cleaners and washing machines with steam cleaning functions.

Consumers plan to buy more health tech

NIQ’s 2025 Global Health & Wellness survey revealed that 74% of people say they would prefer tech appliances that offer health and wellness features (such as washing machines with steam functions, and more effective air purification and water filtration) over ones that do not, and that healthier cooking is the leading motivator for 44% of people looking to buy health-focused appliances.

Marketing clarity and tailored messaging will be key to success here, to cut through the inundation of competing messages from brands across social networks and traditional media channels.

“Steam functions in major appliances are increasingly offering clear health benefits in products such as washing machines and cooking appliances—simultaneously providing better hygiene and healthier living.”

—Norbert Herzog, Head of Global Strategic Insights, NIQ

Alongside consumers’ increased focus on health, climate change is also driving demand for specific products such as electric fans, water filters, air conditioners, soda makers, and frozen dessert makers—and we expect this trend to continue in 2026.

Beauty and well-being

Global sales of beauty appliances are growing—but not as fast as health or hygiene appliances. As a category, beauty appliances are heavily impacted by wealth, age, and region, prompting the need for a highly tailored strategy from manufacturers and retailers alike.

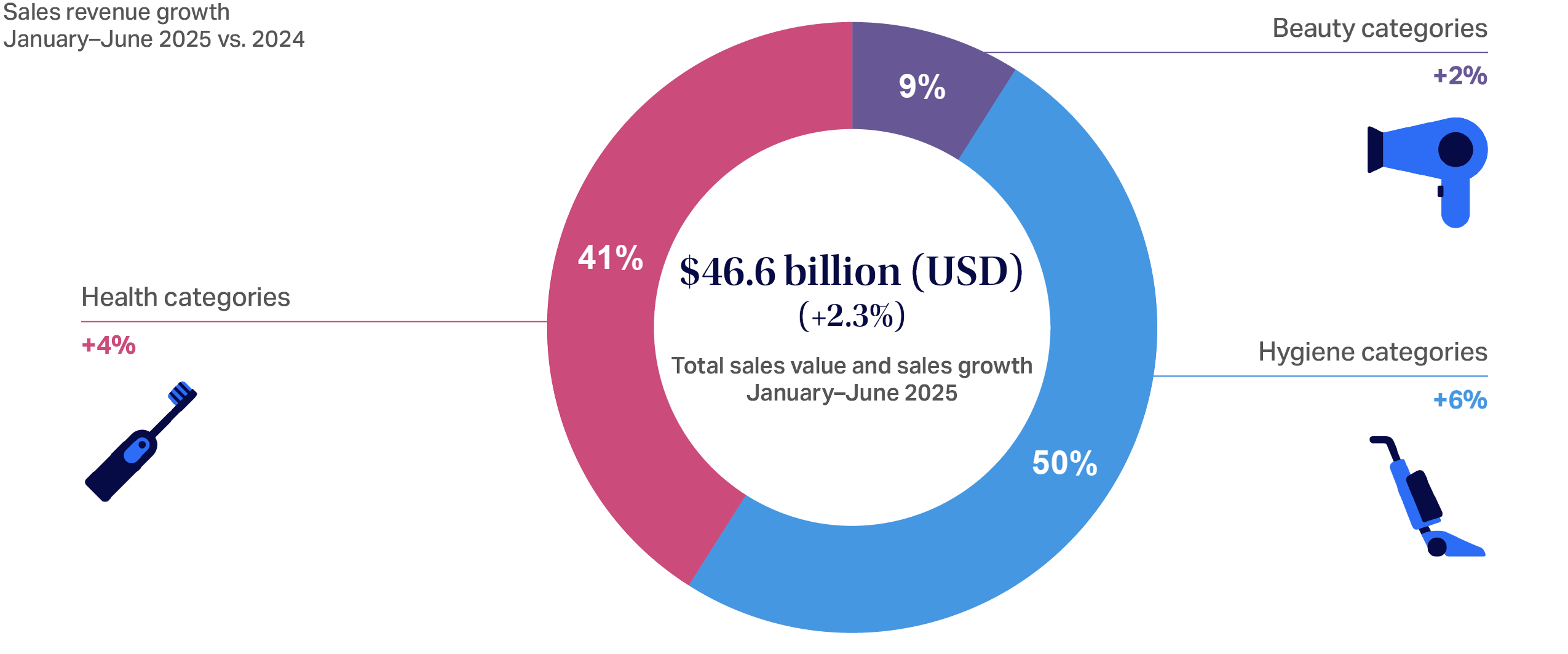

Health, Hygiene, and Beauty categories in Consumer Tech and Durable Goods

Hygiene outpaces total T&D in value growth, growing faster than Health and Beauty.

Beauty includes Hair dryers, Hair stylers, Hair clippers, Shavers, Shaver accessories, Electric male system razor, Electric muscle stimulation, Electric massagers, Electric cosmetics, Electric blankets

Health includes Air treatment, Water filters, Liquidizers (food prep), Electric juicers/presses, Hot air fryers, Electric cooking pots with steam, Mini ovens with steam, Hypoglycemic rice cookers, Food steamers, Light therapy, Baby food cookers, Blood pressure monitors, Digital thermometers, Kitchen scales, Personal scales, Nebulizer

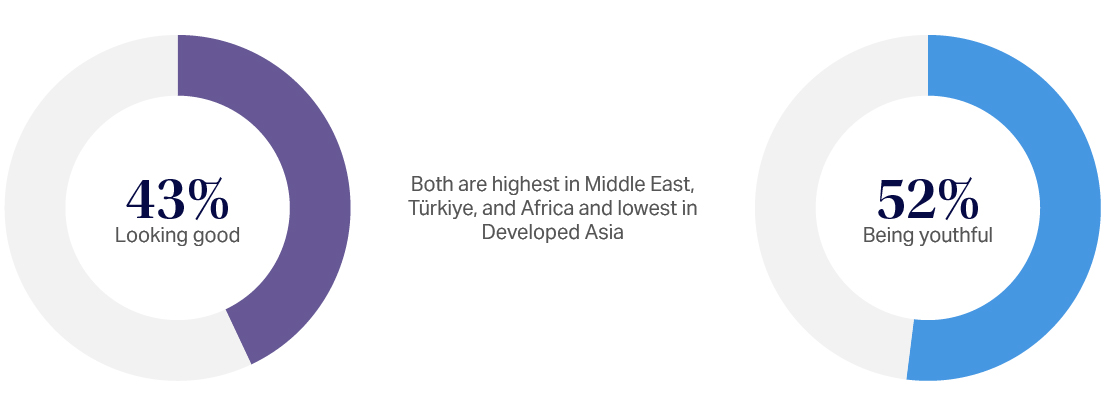

Although 43% of consumers globally say that looking good is important to them and gives them meaning, it’s the higher-income consumers who contribute disproportionately (compared with the size of their segment vs. the total population) to sales of electrical beauty and well-being products.

“Important principle that gives meaning to my life”:

“Beauty appliances are an aspirational category, with ‘looking good’ being an important life value for many consumers. However, purchases in this area trail behind health and hygiene in terms of value growth. Manufacturers need to focus on developing multifunctional, affordable beauty appliances that help consumers both look and feel good. This will be a win-win for both brands and consumers.”

—Nevin Francis, Senior Director, Global Strategic Insights, NIQ

In 2026, we expect to see continued growth in the sales value of beauty appliances across Eastern Europe and the Middle East & Africa (EEMEA). However, they’re likely to decline in Asia Pacific due to the highly successful electric cosmetics and electric stimulation devices facing market saturation and, second, due to increasing regulation classifying some of these electric beauty products as medical devices, which limits their sale over the counter.

Design, functionality, and ease of use will remain important choice drivers overall, while significant buyer groups include Millennials (now ages 29–44) and Gen Z (now ages 13–28), who currently dominate hair dryer and styler purchases.2

To succeed next year, the beauty and well-being appliance industry should focus on innovation that captures specific consumer segments’ aspirations about looking good and feeling good about their body and mind.

2 NIQ gfknewron Consumer

Key takeaways

- For success in 2026, manufacturers and retailers of home appliances must match consumers’ evolving expectations around affordable value and focus on products that deliver quality, convenience, and multifunctionality while being energy-efficient and space-saving.

- Features and functionality will be a bigger driver for consumer choice than brand loyalty. Brands need a strong focus on balancing affordability with new convenience and performance features.

- The key drivers for consumers remain convenience, multifunctionality, performance, health and well-being, beauty, and sustainability. To unlock stronger sales potential, manufacturers and retailers must shift focus from the product form factor to these underlying purchase motivations.

Chapter 4: How home appliances retailers should prepare for 2026

With retailers wary of passing on rising costs to consumers, they need highly targeted strategies to ensure profit growth in 2026.

This will mean focusing on the specific consumer segments who are ready to spend on premium durability, quality, and convenience features. These include Gen X consumers who are at the peak of their spending powers, as well as the 45% of global consumers (especially in the Middle East & Africa, Emerging Asia, and LATAM) who say it’s important to pamper themselves regularly.

“Retailers are seeing more intentional consumers, who remain cautious but are willing to purchase above their original budget when the right value equation is present.”

—Michael McLaughlin, Global Head, Tech & Durables Retail, NIQ

Retailers need to reach those shoppers who are ready to spend a bit more to get greater value, including Gen X “caretaker consumers.”

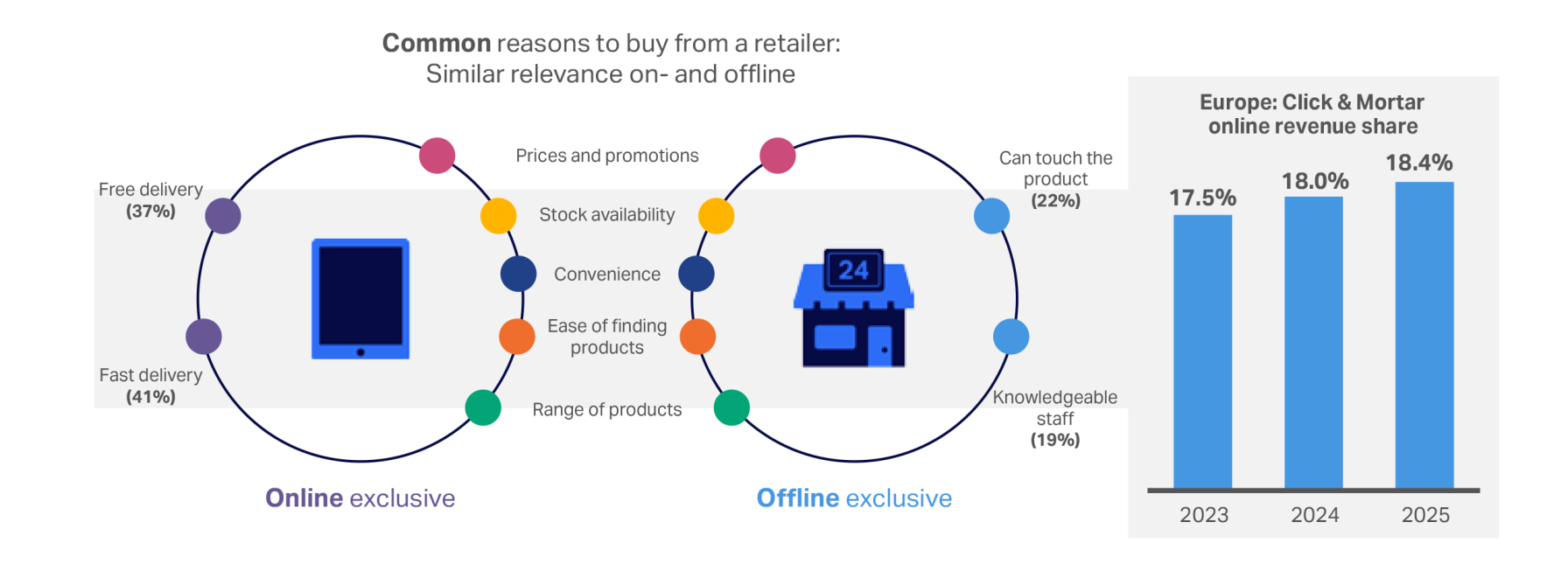

A critical part of retailers’ strategy must be maximizing their omnichannel potential. Consumers today are motivated by moments and experiences, with a high focus on personalization and convenience. They move freely across the full mix of channels to solve their product research and buying needs—and will respond to retailers who present cross-platform consistency featuring truly personalized touchpoints.

Consumers don’t think in channels, but in moments and experiences

Digital habits shape physical expectations; channel choice is contextual.

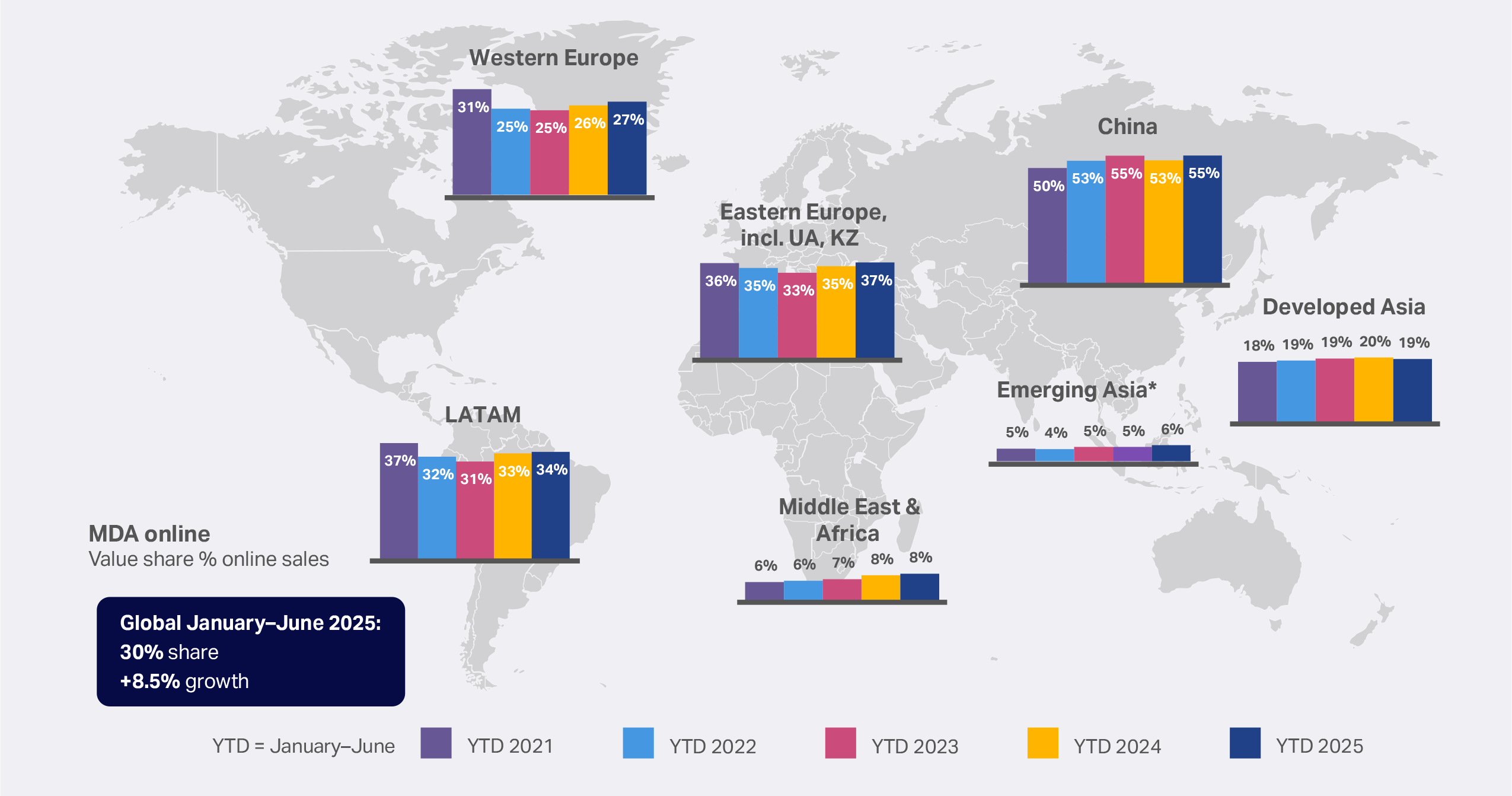

For small domestic appliances, online will continue to grow as a critical purchase channel that already accounts for over half of global purchases—and nearly all purchases in China. For major domestic appliances, online is also expected to grow from the 30% of total global sales it already handles (50% in China). This will be driven by consumers continuing to research MDA products both online and in-store but increasingly selecting the convenience of online for the actual purchase.

SDA online share has always been higher than for Consumer Tech and Durable Goods overall

It continues to grow—and it’s hitting almost 50% in some regions.

MDA e-commerce improves over 2025

Online share of total sales grows again in select regions.

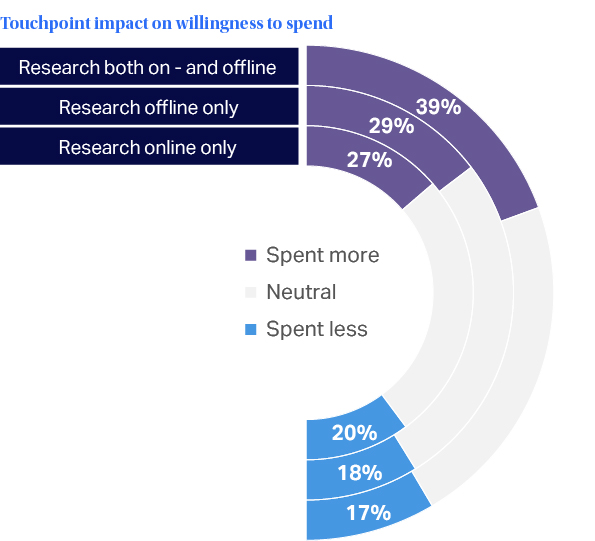

Physical stores will remain important in helping to unlock incremental spend in 2026. NIQ analysis shows that consumers who research a product both online and offline are more likely to spend more than intended when they come to purchase—regardless of what channel that final purchase is made on.

Omnichannel isn’t just about meeting expectations

It’s also about unlocking incremental consumer spend—regardless of whether the final purchase is made on- or offline

Social commerce also plays a growing role in the buying journey. This channel presents emerging opportunities for household appliances that have strong visual appeal either in their design or operation—such as beauty tech, shavers, coffee machines, or frozen dessert makers.

Retailers must also take a strategic focus on the opportunity presented by online marketplaces, which are acquiring an increasing share of consumers’ online spending and allow retailers to offer A-to-Z assortments of products without having to hold or ship all associated inventory themselves.

“Retailers must have a connected omnichannel experience for all points of the consumer journey. Pure online continues to dominate, but social commerce, marketplaces, and in-store experiences are a critical factor in both research and buying.”

—Michael McLaughlin, Global Head, Tech & Durables Retail, NIQ

Consumers’ preferred payment models are also continuing to evolve. In MDA and higher-priced SDA, flexible installment or “buy now, pay later” terms will prove ever more popular next year— especially in Eastern Europe and LATAM. Subscription and rental models are also on the rise, allowing the smartest retailers to communicate with their consumers just ahead of their renewal needs.

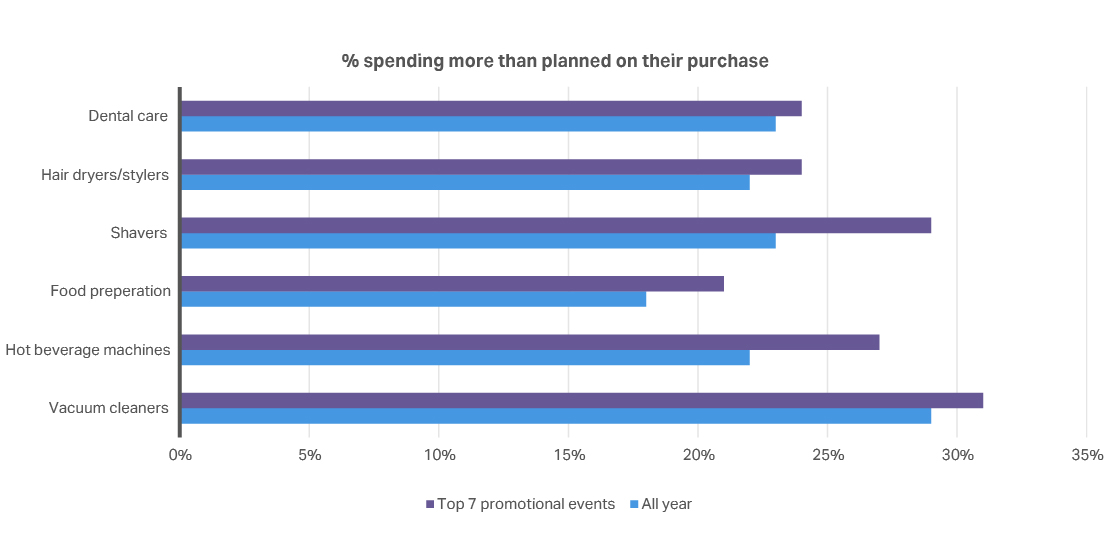

Finally, consumers are continuing to time their planned purchases for major annual promotional events. But they aren’t necessarily buying cheaper products. Often, they’re looking to increase the value they get for their money by buying premium products at a discount. In fact, during these events, consumers are more likely than usual to spend more than they intended—especially on vacuum cleaners, shavers, and hot beverage machines. Retailers must be able to present highly relevant, personalized offers during these major promotional events to stand out from the noise.

Consumers spending more than planned at promotional events—maximizing value by buying premium products at discoun

Key takeaways

- In 2026, retailers will be able to capture significant premium spending by focusing on specific consumer segments, such as Gen X, who are ready to spend on products that offer durability, quality, and convenience.

- Retailers must also aim to consolidate all their channels into a service ecosystem experience: a single front- and back-end system that delivers a high focus on personalized touchpoints and cross-platform consistency.

- Price competition will heighten with Chinese brands offering strong features at competitive prices. Finding the optimal price point and assortment range to balance volume sales and premium profitability will be critical.

- Promotions will continue to account for a growing percentage of total sales, so retailers must have a balanced strategy to maximize the opportunities of events such as Black Friday and Cyber Monday.

Chapter 5: Global key takeaways for home appliances industry in 2026

For manufacturers

- Focus form and features around new lifestyles: With growing competition from challenger brands, manufacturer success hinges on balancing affordability and product value—innovating in areas such as space-constrained living, multifunctionality, and AI-enhanced—for greater performance, convenience, and ease of use.

- Consider circular design and modularity: This helps meet consumers’ sustainability expectations, providing a key point of differentiation in a crowded marketplace.

- Design products to be ecosystem-centric: Consider areas where seamless collaboration across devices and categories can meet consumer expectations for smart, connected living.

For retailers

- Showcase ecosystem experiences: Create in-store and online environments that demonstrate how smart devices work together, helping consumers visualize real-life use cases and encouraging multi-product purchases.

- Speak the language of Gen X: Manufacturers and retailers should aim to reach Gen X, now a key demographic, with product communication that highlights the performance and convenience of these products.

- Build your omnichannel ecosystem: Consumers want experiences, everywhere. Brands and retailers must ensure that they present cross-platform consistency for consumers, featuring truly personalized touchpoints.

For both

- Tailor for powerful regional growth: There are pockets of strong sales growth in key regions worldwide, as we reveal in our next chapter.

Over 20,000 manufacturing and retail businesses use NIQ’s Full View of the consumer for an all-around understanding of shopper intentions and purchases across 100+ countries. Our intuitive, on-demand insights—from sales through 1.5M stores and 82,000 online merchants globally—provide actionable knowledge for confident, effective growth decisions.

Chapter 6: Regional outlook: Home appliance projections for full-year 2025 and 2026

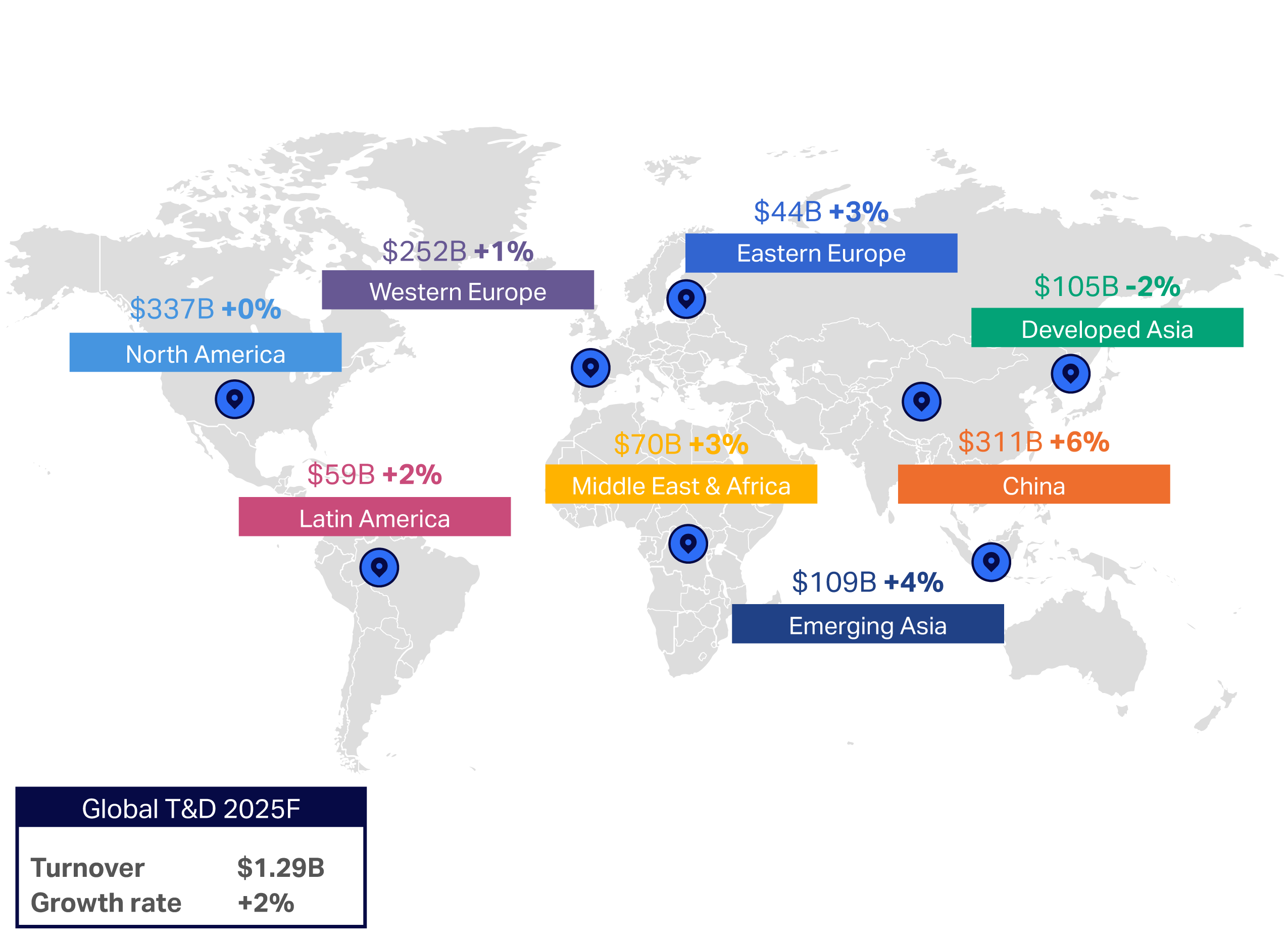

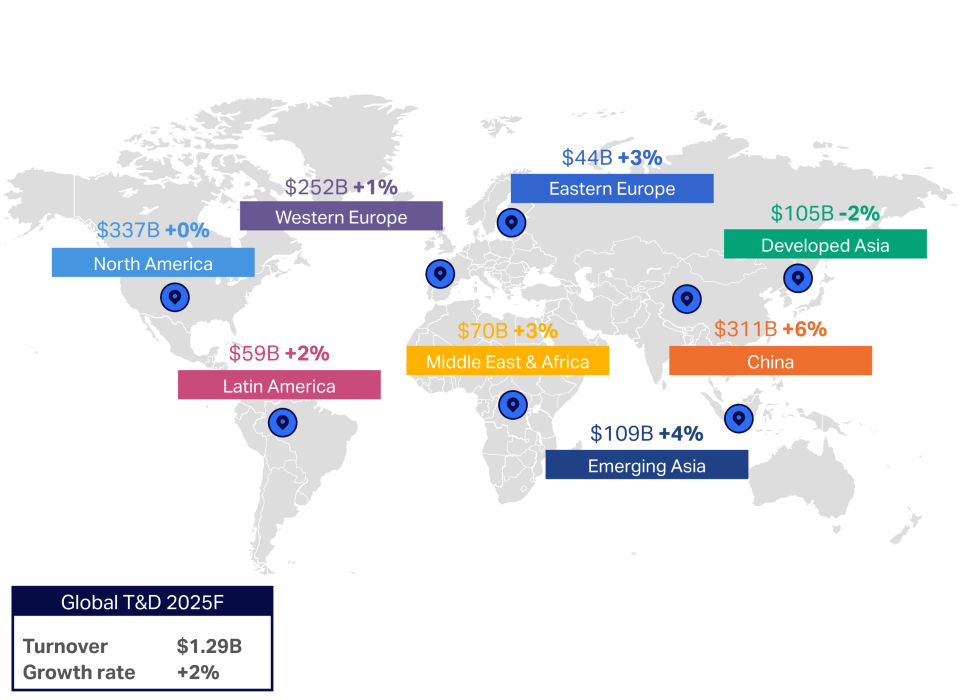

For full-year 2025, we expect the strongest total Consumer Tech and Durable Goods (T&D) sales value growth in China (bolstered by its trade-in policy), followed by Emerging Asia, Eastern Europe, and the Middle East & Africa (MEA).

Consumer Tech and Durable Goods sales: 2025 full-year forecast

Global (excl. Russia)

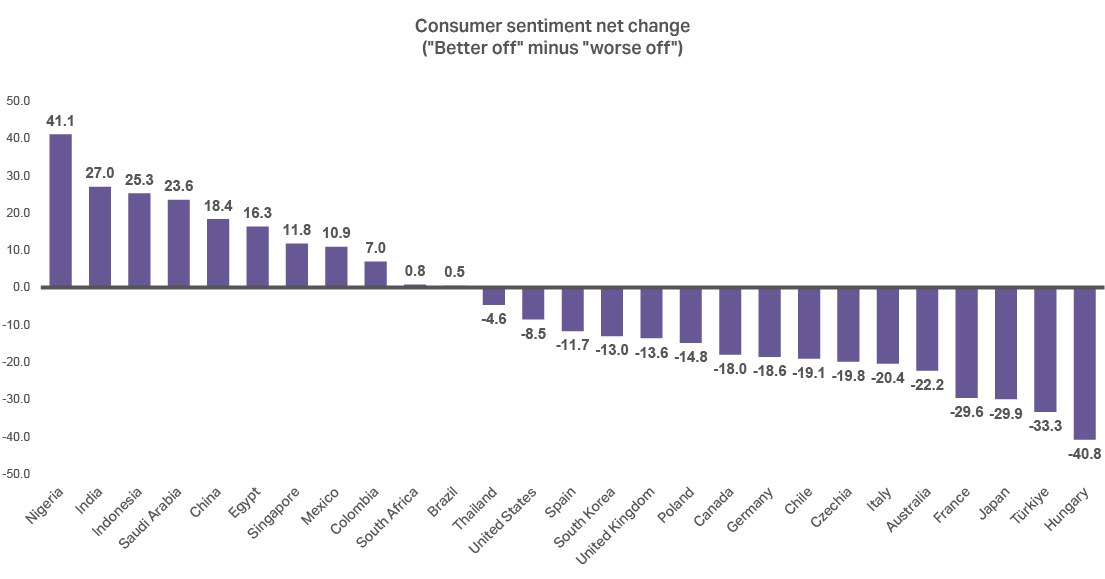

Data from NIQ’s 2025 Consumer Outlook survey shows key countries within Emerging Asia and MEA currently have the highest percentage of households who feel better off financially than they did a year ago, while households in countries in North America and Europe are more likely to feel worse off.

Consumer optimism around financial situation varies widely by region and country

2025 total T&D full-year projection (value growth):

- China: +6%

- Emerging Asia (without China): +4%

- Developed Asia: -2%

2026 home appliance projections (value growth):

- MDA

- China: +4% to 7%

- APAC (without China): -2% to +1%

- SDA

- China: +3% to 6%

- APAC (without China): +1% to 3%

Asia Pacific (APAC)

APAC overview

Price will remain pivotal in China, where 70% of consumers have used the trade-in subsidy to replace items, and in India, where consumers generally prefer to replace items only when they’re broken (aka, unserviceable).

However, even a small increase in spending appetite among middle-income households across these countries’ enormous populations can boost premium sales significantly. Notably, in India, which was recently hit by 50% US tariffs, the government is reforming the income tax and the Goods and Services Tax (GST) to bolster its population’s spending capacity.

Value will be key in the developed economies of Australia, Japan, Singapore, and South Korea—particularly regarding premium purchases with strong and demonstrable benefits for consumers.

Price-sensitive developing markets such as Indonesia, the Philippines, Thailand, and Vietnam also present significant new MDA and SDA sales growth opportunities, particularly for affordable multifunctional products.

APAC key takeaways for 2026

- In major household appliance sales, manufacturers and retailers should prioritize smart energy efficiency and compact forms while capturing growth in air conditioning and AI-enabled washers and dryers.

- MDA should also focus on trade-in and flexible ownership payment models to encourage price-sensitive consumers to replace or upgrade. EMI payment facilities or BNPL (buy now pay later) are key in India and Southeast Asia.

- In small household appliances, product innovation should focus on convenience, hygiene, health, and living with the effects of climate change (e.g., air coolers, water purifiers, electric fans, steam cleaning).

- Channel choices will be critical. Sales performance will benefit from the right balance of in-store experiences, effective online sales and discovery, and savvy use of social commerce.

- “Quick commerce” (ultra-fast delivery) will become another competitive battleground for retailers and brands in India—particularly in major cities where consumers will have increased spending capacity from the new reduced income tax and GST rate reductions.

For our full APAC 2026 outlook, check out our Home Appliances Outlook 2026: Regional Insights Companion.

Eastern Europe, Middle East & Africa (EEMEA)

2025 total T&D full-year projection (value growth):

- Eastern Europe: +3%

- Middle East & Africa: +3%

2026 home appliance projections (value growth):

- MDA: +4%

- SDA: +6%

EEMEA overview

For full-year 2025, we forecast low- to mid-single-digit growth across both MDA and SDA. We expect only around 3% growth for MDA sales, with competition from Chinese brands pushing down price points and a peak replacement cycle not fully expected until 2028. In SDA, we expect approximately 6% growth, driven by premium purchases such as vacuums and hot beverage makers, with replacement cycles for SDA kicking in during 2026.

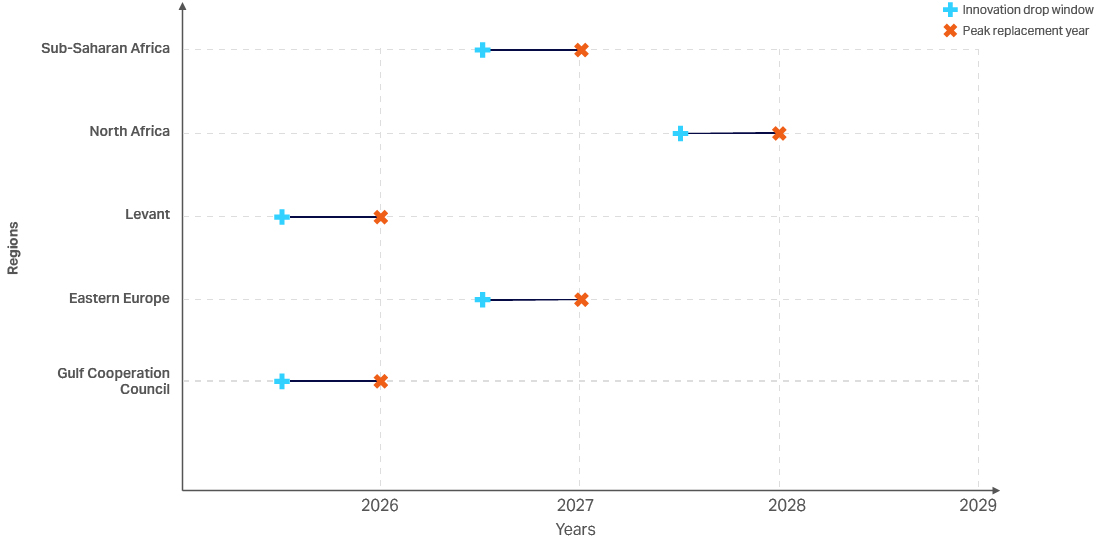

While SDA replacement cycles are far shorter than for MDA, if we look at all home appliances combined, we expect 2026 to mark the start of peak replacement cycles for Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates; 2027 onwards for Sub-Saharan Africa and Eastern Europe; and 2028 onwards for North Africa. However, compelling innovation in performance and/or features could encourage consumers to buy premium products earlier (see below). In Eastern Europe, we expect regional brands to gain share.

EEMEA: Replacement cycle peaks vs. innovation drop windows, MDA and SDA combined

Eastern Europe outlook

Price sensitivity should ease by 2027, as consumer confidence rises. Until then, a focus on affordability and compelling performance value will remain imperative.

In major home appliances, we expect strengthening uptake of built-in appliances due to the numbers of new property developments. Products with lower current penetration, such as dishwashers, tumble dryers with heat pumps, and slimline dishwashers (in smaller properties) will gain share.

In small home appliances, we expect particularly robust growth in Poland, Romania, and Ukraine, driven by increasing disposable income across income groups and by the commoditization of products featuring recent innovations.

Middle East & Africa (MEA) outlook

Prices will continue to fall due to increased brand competition and the ongoing rise of pure-play online and marketplaces—as well as strong mass merchant discount events.

In major home appliances, amid high temperatures, climate-related product sales will grow—particularly for mid-range air conditioners and those usable during power cuts in Africa, as well as higher-range items in the Middle East. Chinese-brand fridges, including those that are solar compatible, will gain popularity, and water heaters and efficient LPG canister cooking will rise across Sub-Saharan and Central Africa. Local and Chinese low-priced washing machines and twin tubs are growing, while wealthier segments will buy high-capacity washer-dryers.

In small home appliances, wide-voltage items will grow rapidly in Sub-Saharan Africa and the Levant, given their capacity to operate across a range of voltage standards. By contrast, premium products—including robotic vacuums, multi-basket air fryers, high-end or multifunctional food preparation appliances, and frozen dessert makers that are useful when hosting events tied to religious festivals—will be increasingly popular in larger Middle Eastern homes.

EEMEA key takeaways for 2026

- In major domestic appliance sales, manufacturers and retailers should focus on built-in, slimline products in Eastern Europe, while cooling will grow across the Middle East & Africa.

- Small domestic appliances will see significant growth in Eastern Europe and the Middle East, while sales of wide-voltage items are expected to grow in Africa and the Levant.

- Across the region, manufacturers and retailers must sharpen their assortment and price point strategies on a country-by-country basis to reach lower- and middle-income households and to encourage wealthier homeowners to buy too.

- Innovative purchase models and smart omnichannel strategies will also be essential to support customers in appliance discovery and purchasing.

For our full EEMEA 2026 outlook, check out our Home Appliances Outlook 2026: Regional Insights Companion.

Latin America (LATAM)

LATAM overview

Established markets, including Brazil, Chile, and Mexico, are seeing moderate value growth, as units increase but average prices fall with the arrival of Chinese brands. Value for money, even in the premium segment, remains important, so brands and retailers need to push innovation.

Meanwhile, in Argentina, where triple-digit inflation has hurt the market, conditions are stabilizing, and consumers are gradually buying more appliances. From a recent low baseline, therefore, we expect strong growth in this market.

2025 total T&D full-year projection (value growth)

- Latin America: +2%

2026 home appliance projections (value growth):

- MDA: +3% to 5%

- SDA: +4% to 6%

LATAM key takeaways for 2026:

- In major household appliance sales, brands and retailers will focus on tumble dryers and freezers as growth segments, alongside smart cooling.

- In small household appliances, we expect innovative premiumization in products such as vacuum cleaners and food preparation appliances to be important.

- With the port in Chancay (Peru) serving to expand Chinese imports, all established manufacturers within LATAM will increasingly need to offer affordable premium items to remain competitive.

- It will be critical, too, for retailers to upgrade their online offerings by improving product assortments and consumer experiences across research, buying, and delivery to strengthen trust.

For our full LATAM 2026 outlook, check out our Home Appliances Outlook 2026: Regional Insights Companion.

North America

North America overview

In North America in 2026, we expect moderate growth in major and small appliance sales value, following a flat 2025.

Major home appliance sales value will be supported by sustained demand driven by replacement cycles, potential interest rate cuts starting in late 2025, and exchange rates, which continue to provide an upward push on US dollar numbers. In volume and value terms, expiring federal tax credits for individuals installing more environmentally friendly air conditioning and refrigeration will put downward pressure on sales, and we expect minimal growth in 2026.

In small home appliances, we expect slower but steady growth. As inflation eases, sales will likely rebound. In addition, changing lifestyles and smaller living spaces, as well as the popularity of premium appliances, will continue to drive growth.

2025 total T&D full-year projection (value growth):

- North America +0% (flat)

2026 home appliance projections (value growth):

- MDA: +0.4%

- SDA: +1%

North America key takeaways for 2026:

- In major home appliance sales, manufacturers and retailers should aim to capitalize on specific incoming replacement cycles on dishwashers, refrigerators, and air conditioners.

- The industry should appeal to consumer trends by doubling down on smart innovation, such as around AI-driven energy savings and eco-friendly materials.

- In small home appliances, health, hygiene, and convenience will be the strongest drivers on which the industry should aim to capitalize.

- Product promotions should be timed around the big annual promotional events—and harness social commerce—to capture value-conscious buyers looking to make the most of their spending by buying premium products at a discount.

For our full North America 2026 outlook, check out our Home Appliances Outlook 2026: Regional Insights Companion.

Western Europe

Western Europe overview

Macroeconomic disruption in Western Europe continues to challenge manufacturers and retailers. There are widespread expectations, too, that Chinese brands will continue to increase their impact within key markets with high-functionality appliances at competitive prices, taking additional MDA and SDA market share from established brands.

Price will drive consumer choice in many markets, while brand, reliability, and performance are important to specific segments of product buyers.

Growth in online sales will continue to dominate small home appliance sales, with social commerce presenting opportunities for products with obvious visual appeal or that lend themselves to influencer reviews, such as beauty appliances and frozen dessert makers.

2025 total T&D full-year projection (value growth):

- Western Europe: +1%

2026 home appliance projections (value growth):

- MDA: +1.5%

- SDA: +5% to 7%

Western Europe key takeaways for 2026:

- In major domestic appliance sales, the market will only grow slightly, driven mainly by replacements of broken appliances and by first-time buyer sales.

- Small domestic appliance sales will grow much more strongly, bolstered by replacement cycles and consumers upgrading to get higher convenience, performance, or health features.

- With more brand competition, small appliance innovation must focus on design and timely convenience-based features, while large appliance innovation should focus on clear premium propositions around resources savings (e.g., energy, water) and convenience (e.g., timesaving, self-cleaning, frost-free).

- Retailers will continue to face stiff competition and must augment how they explain compelling product benefits and create attractive, personalized service ecosystems that unify the online and offline experience for shoppers.

For our full Western Europe 2026 outlook, check out our Home Appliances Outlook 2026: Regional Insights Companion.

Want to go deeper?

Discover the NIQ solutions driving this report

Grow your business and market share with a complete view of performance across categories, channels, and global markets.

Understand consumers and shoppers through purchases, clicks, and trends—and the motivations behind them.

Understand all aspects of people’s lives: Not just the what, but the why, the why now, and the what to do next.

The vast majority (91%) of consumers buy products both in-store and online. Most companies struggle to fully measure this omnichannel sales landscape—until now.

Home Appliances Outlook 2026: Asia Pacific

Home Appliances Outlook 2026: Eastern Europe, Middle East & Africa

Home Appliances Outlook 2026: Latin America

Home Appliances Outlook 2026: North America

Home Appliances Outlook 2026: Western Europe

Contact our experts to discuss how to maximize your opportunities in 2026

Global experts

Amanda Martin

Global Thought Leadership & Content, T&D

Norbert Herzog

Head of Global Strategic Insights

Nevin Francis

Senior Director, Global Strategic Insights

NIQ Next

Frank Landeck

Global T&D Lead, NIQ Next

Global T&D Retail

Michael McLaughlin

Global Head, T&D Retail

Regional experts

Mukund Tripathi

Customer Success Leader, T&D, Southeast Asia, North Asia, and Pacific (SEANAP) and India

Navneet Chawnani

Regional Consulting Lead, EEMEA

Nicolet Pienaar

Customer Success Senior Manager, MEA

Enrique Espinosa de los Monteros

Regional Director, T&D, LATAM

Steffen Schenk

Managing Director, T&D, North America

Paul Mitchell

Regional Consulting Lead, Western Europe

Thilo Heyder

Regional Director, SDA, Western Europe

Rachel Gilbey

Senior Regional Insights Manager, MDA, Western Europe

Markus Wagenhäuser

Customer Success Director, MDA, Western Europe

Forward-Looking Statements Disclaimer

This report may contain forward-looking statements regarding anticipated consumer behaviors, market trends, and industry developments. These statements reflect current expectations and projections based on available data, historical patterns, and various assumptions. Words such as “expects,” “anticipates,” “projects,” “believes,” “forecasts,” and similar expressions are intended to identify such forward-looking statements. These statements are not guarantees of future outcomes and are subject to inherent uncertainties, including changes in consumer preferences, economic conditions, technological advancements, and competitive dynamics. Actual results may differ materially from those expressed or implied in these statements. While we strive to base our insights on reliable data and sound methodologies, we undertake no obligation to update any forward-looking statements to reflect future events or circumstances, except to the extent required by applicable law.