Oil prices rarely show up as a line item on a store shelf, but for consumer-packaged goods, they quietly shape nearly every economic decision behind that price tag. From raw materials and packaging to transportation, manufacturing energy, and supply chain resilience, oil is embedded across the CPG value chain.

At a moment when consumers remain acutely price sensitive after several years of inflation, renewed pressure from higher oil prices represents more than another cost variable. It is a risk factor that can quickly alter demand, mix, and brand loyalty. According to NielsenIQ, the consumer appetite for absorbing additional price increases remains limited, leaving manufacturers and retailers with little room to maneuver without consequences for volume and share. [1,2]

Recent volatility in energy markets has pushed crude prices back into a range that historically coincides with renewed inflationary pressure across food, household, and personal care categories. History also shows that when oil price increases persist rather than reverse quickly, they tend to move alongside food prices and broader consumer inflation, reinforcing cost throughout the system rather than dissipating it. [3,4]

For CPG leaders, oil prices are not a background macro indicator. Instead, they are a practical input shaping daily commercial decisions.

The CPG Cost Stack Is More Oil‑Exposed Than It Looks

Oil’s influence on CPG economics operates through three interconnected channels that often activate simultaneously.

Transportation & fuel

First is transportation and fuel

Diesel, bunker fuel, and freight costs track crude prices closely and represent up to 40 percent of total transportation expenses across trucking, maritime shipping, and intermodal logistics. As oil prices rise, carriers typically pass those increases through via fuel surcharges, contract escalators, or higher spot rates. [6,7]

Comodities & packaging

Second are upstream commodities and packaging

Many agricultural inputs are energy intensive to produce and move. Plastic packaging materials such as polyethylene, polypropylene, and PET are petrochemical derivatives whose pricing follows crude oil with a short lag. Even non plastic materials like glass and aluminum are affected because of the energy required to produce them. [9,10,14]

Manufacturing & utilities

Third is manufacturing and utilities

Electricity, heat, and industrial fuels represent meaningful portions of cost of goods sold, particularly in categories requiring refrigeration, sterilization, or continuous production.

The risk is not any one input rising in isolation. NIQ analysis consistently shows that cost pressure becomes most disruptive when these forces compound at once, compressing margins faster than pricing can adjust. [5,6]

Transportation Is the Fastest Transmission Mechanism

Transportation is typically where oil pressure shows up first and most visibly. Higher inbound freight costs for ingredients and packaging quickly flow into higher outbound distribution costs to retailers. Volatility also complicates budgeting and forecasting, as transportation costs become harder to lock in with confidence.

NIQ data indicates this pressure is especially acute in low margin, high velocity categories such as food, beverages, and household essentials. Pricing power is limited, while consumer trade down risk is high. [1]

Oil volatility also increases supply chain fragility. Research shows that sustained energy shocks tend to lengthen lead times, accelerate nearshoring or regionalization, and reduce reliance on distant suppliers. These decisions may improve resilience, but they often bring higher structural costs that do not quickly unwind when oil prices ease. [5,8]

If energy costs decide your growth strategy, let’s chat.

Schedule time with an NIQ industry expert

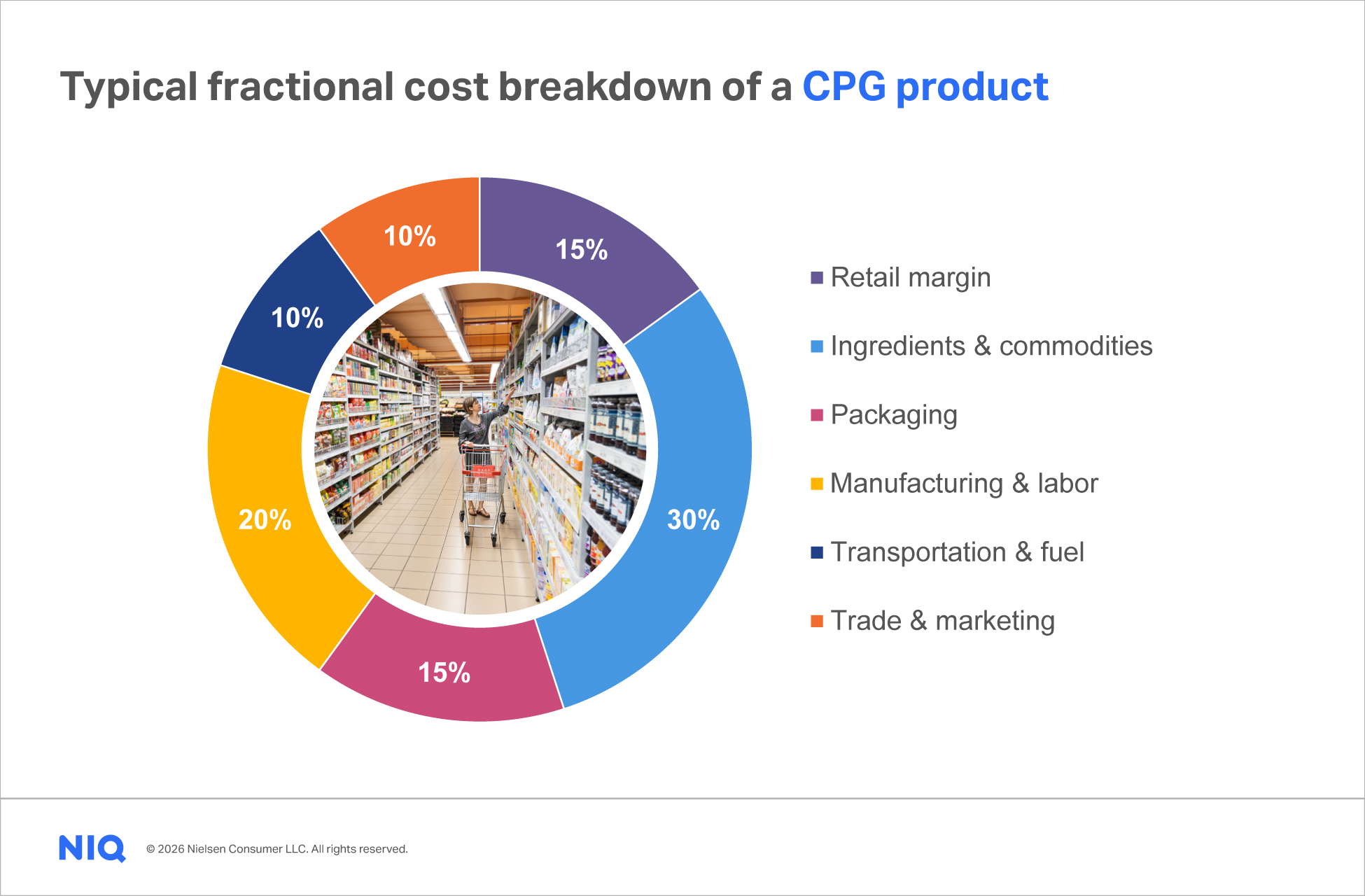

Where Oil Pressure Concentrates Inside the CPG Dollar

While every category is different, a typical CPG product allocates most of its dollars across ingredients, packaging, manufacturing, and transportation. Together, these cost components represent roughly three-quarters of the total cost and are all meaningfully exposed to oil-linked increases.

Transportation and fuel face a direct pass-through from higher diesel prices. Packaging absorbs higher resin, energy, and logistics costs. Ingredients and commodities reflect energy-intensive agriculture and processing.

Manufacturing and utilities rise with electricity and fuel costs.

Retail margins and trade spend are less directly tied to oil, but they often become pressure valves when price elasticity limits shelf price increases.

Category Implications Are Uneven. And It Matters

NIQ data shows that while higher oil prices affect all CPG, the timing and magnitude vary by category.

Food and beverage (F&B)

Food and beverage

Food and beverages feel pressure earliest. Fresh, refrigerated, and frozen foods depend heavily on diesel powered transportation and cold chain logistics. Packaged beverages are doubly exposed, as PET packaging often represents one of the largest single cost components while distribution is freight intensive. Historically, oil price spikes align with faster inflation in these categories relative to shelf stable groceries. [3,12,14]

Household and cleaning products

Household and cleaning products

Household and cleaning products face exposure through both formulation and packaging. Many detergents rely on petrochemical based surfactants and fragrances, while heavy plastic packaging tracks resin markets closely. Even paper products, though fiber based, are energy intensive to produce and ship. Consumer response in these categories is typically swift, with shoppers extending usage cycles and prioritizing promotions or larger formats. [2,10,11,13]

Health, beauty, and personal care

Health, beauty, and personal care

Health, beauty, and personal care often encounter oil pressure in less visible but concentrated ways. High specification packaging, decorative components, and specialty formulations inflate together. Smaller, higher value items are also disproportionately affected by logistics costs. NIQ data suggests shoppers respond by delaying purchases or trading across brands and price tiers when inflation reemerges. [1,14]

Pet food and pet care

Pet

Pet food and pet care remain structurally resilient, but not immune. Energy intensive processing, metal packaging, and long-distance shipping all increase exposure. Pet parents tend to remain loyal to trusted brands but often adjust pack sizes or rely more heavily on promotions as prices rise. [2]

Shelf-stable snacks

Shelf stable snacks and packaged foods

Snacks and packaged foods typically feel oil pressure later, but margin compression often builds internally before fully surfacing at retail. Flexible packaging is almost entirely plastic based, and widespread, high frequency distribution amplifies exposure to fuel surcharges. [5]

06

NONE

NONE

Oil Prices Shape Consumer Behavior, Not Just Costs

Higher oil prices do more than raise costs. They reshape how consumers shop.

NIQ data consistently shows that when inflation resurfaces, shoppers shift more quickly toward private label, value channels, smaller pack sizes, and promotional dependence. These shifts change category dynamics and brand elasticity, often long before manufacturers fully adjust list prices. [1,2]

Manufacturers are forced into difficult tradeoffs. Absorbing costs compresses margins. Passing them through risks volume declines. Reformulating products, resizing packages, or rebalancing assortments introduces operational complexity. Supply chain redesigns aimed at resilience may stabilize service, but often at a higher long term cost base.

NIQ’s Perspective: Duration Matters More Than the Headline Price

From an NIQ perspective, the critical question is not whether oil prices spike, but how long elevated volatility persists. Short lived increases are often managed within existing systems. Sustained pressure, however, rewrites contracts, resets expectations, and embeds itself into consumer behavior.

With consumers still highly price conscious, future cost recovery is unlikely to be evenly distributed. Brands with strong value perception, disciplined pricing strategy, and granular visibility into cost drivers will navigate more effectively than those relying on blunt price increases.

As energy markets once again move to the center of the inflation conversation, CPG leaders will need deeper scenario modeling, sharper consumer insight, and more precise price pack architecture to protect growth. Oil prices may be set in global markets, but their consequences are decided every day on the shelf.

Talk to an NIQ expert about what oil prices mean for your category

Book a call with an industry expert